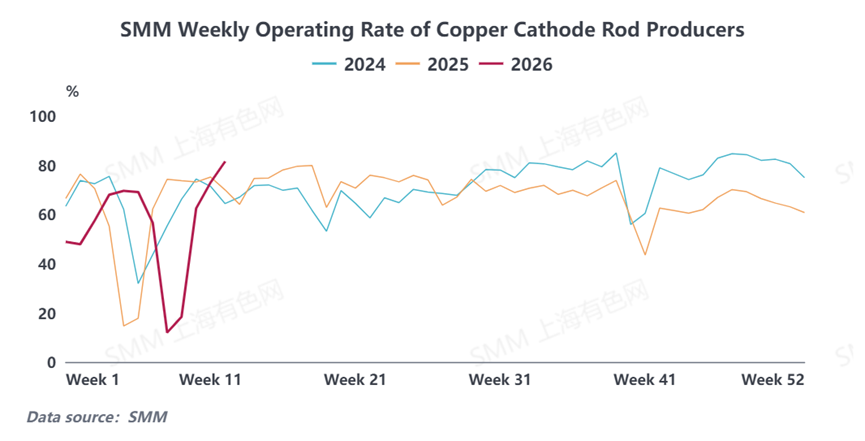

The operating rate of major copper cathode rod enterprises in China stood at 81.51% last week (March 13–March 19), marking the fourth consecutive week of improvement since the Chinese New Year, with industry sentiment continuing to recover.

The strong rebound in the operating rate in this round was mainly driven by two factors: first, the relatively weak operating rates of secondary copper rod enterprises, coupled with the price difference between copper cathode and copper scrap remaining at a relatively low level, significantly weakened the substitution effect between copper cathode and copper scrap, leaving more market room for copper cathode rod; second, improving orders for downstream wire and cable and enamelled wire boosted a faster drawdown in enterprises' finished product inventories. As copper prices broke above low-level support, downstream procurement sentiment continued to heat up, and new orders for copper cathode rod enterprises showed a pattern of concentrated volume release. Most enterprises reported that their production pace could no longer keep up with shipment progress, and some had already begun to proactively control the pace of taking orders to ensure contract fulfillment.

From the downstream industry perspective, wire and cable as well as enamelled wire enterprises also benefited from the pullback in copper prices, with operating rates steadily rebounding, further boosting demand for copper rod.

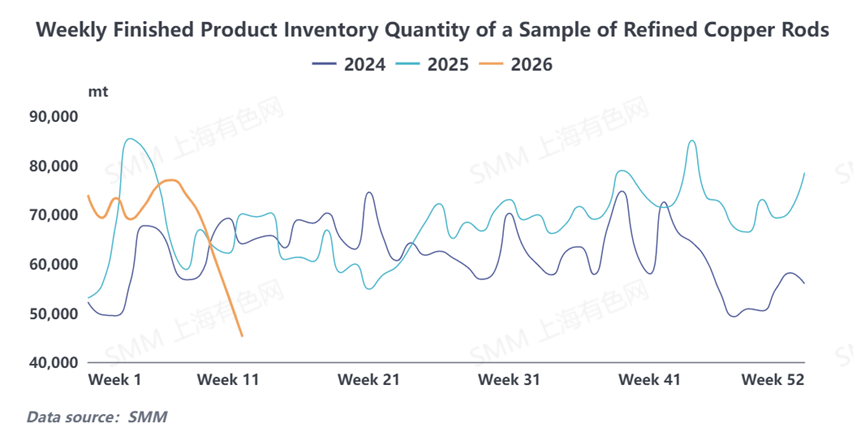

Inventory side, although the pullback in copper prices boosted enterprises' willingness to restock, constrained by limited room for capacity release, enterprises did not excessively stockpile on dips and mostly maintained normal production raw material reserves. Meanwhile, due to continued downstream pick-up of goods, enterprises' capacity was unable to fully match order demand, accelerating the drawdown of finished product inventories.

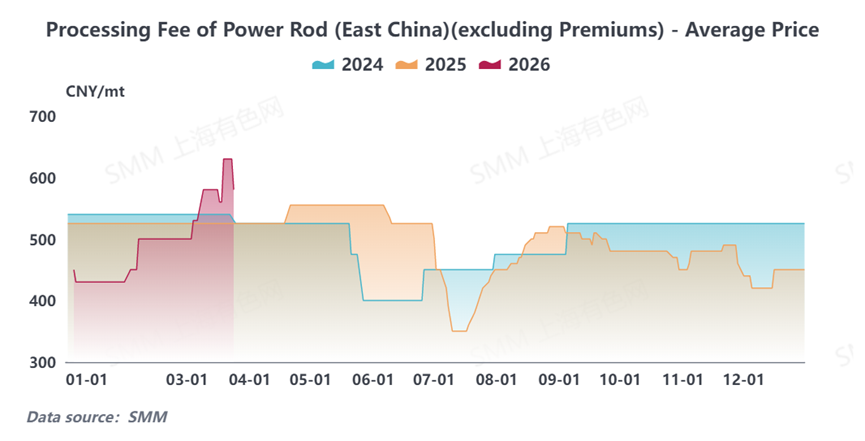

Enterprises Raise Processing Fees and Increase Margin Requirements to Control Risks

After copper prices pulled back sharply, downstream purchase willingness increased significantly, and order concentration rose markedly. To reasonably control the pace of taking orders, some enterprises urgently raised processing fees. At the same time, affected by the increased uncertainty in the pace of cargo pick-up caused by concentrated downstream order placement, as well as the continued decline in copper prices, enterprises became more concerned about the default risk of earlier high-priced orders, and some enterprises simultaneously increased margin ratios to strengthen risk control.

Looking ahead, with copper prices rising at present, downstream procurement sentiment has clearly weakened. To ensure stable deliveries, copper cathode rod enterprises are expected to maintain relatively high operating loads. Although rigid demand is gradually being fully released, against the backdrop of low finished product inventories, enterprises will still maintain high operating rates to replenish inventory. Accordingly, SMM expects the operating rate of China's copper cathode rod enterprises to fluctuate at highs in March.