Tính đến ngày 24 tháng 3, giá chào bán titanium dioxide anatase là 12.600-13.200 nhân dân tệ/tấn, giá bình quân 12.900 nhân dân tệ/tấn, đi ngang so với ngày trước đó; titanium dioxide rutile được chào ở mức 13.800-14.500 nhân dân tệ/tấn, giá bình quân 14.150 nhân dân tệ/tấn, tăng 150 nhân dân tệ so với ngày trước đó; titanium dioxide quy trình chloride được chào ở mức 14.600-17.200 nhân dân tệ/tấn, giá bình quân 15.900 nhân dân tệ/tấn, tăng 300 nhân dân tệ so với ngày trước đó.

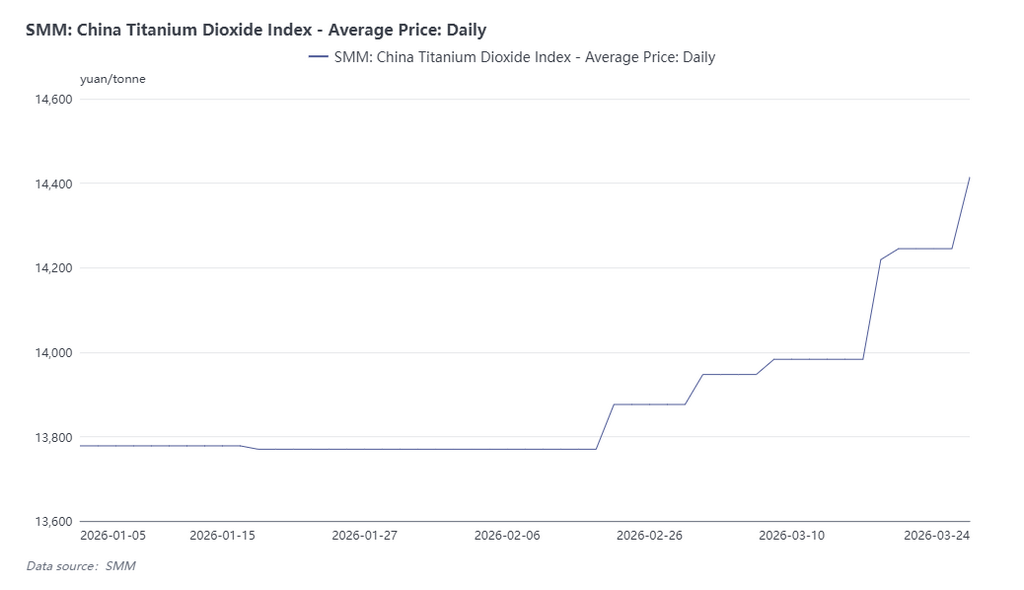

Chỉ số titanium dioxide SMM Trung Quốc đạt 14.414 nhân dân tệ/tấn, tăng 169 nhân dân tệ/tấn so với ngày trước đó và tăng 4,6% so với đầu năm 2026.

Kể từ tháng 3, các doanh nghiệp titanium dioxide đã liên tiếp phát đi hai đợt thông báo tăng giá. Bắt đầu từ ngày 16 tháng 3, nhiều doanh nghiệp chủ lực lần lượt công bố thông báo điều chỉnh giá lần hai trong tháng, đồng loạt nâng giá bán tất cả các cấp sản phẩm, trong đó giá cơ sở cho thị trường nội địa tăng 500 nhân dân tệ/tấn và giá xuất khẩu tăng 100 USD/tấn. Sau đó, báo giá đơn hàng tại nhà máy nhìn chung được nâng theo các thông báo, một số doanh nghiệp đã tạm ngừng nhận đơn hàng mới, và tồn kho thị trường vẫn ở mức thấp.

Logic cốt lõi đằng sau đợt tăng giá titanium dioxide: cộng hưởng giữa áp lực chi phí và cú sốc địa chính trị

Logic cốt lõi của đợt tăng giá trên diện rộng là ngành titanium dioxide đã chịu thua lỗ phổ biến trong năm 2025 do biên lợi nhuận bị thu hẹp bởi chi phí. Đối với titanium dioxide quy trình sulphate, áp lực chi phí cốt lõi đến từ axit sulfuric, với khoảng 2,5-3 tấn axit sulfuric được tiêu thụ để sản xuất 1 tấn titanium dioxide, cho thấy nhu cầu rất lớn. Tính đến ngày 20 tháng 3, chỉ số axit luyện kim SMM Trung Quốc đạt 1.079,5 nhân dân tệ/tấn, tăng 19,49% so với đầu năm.

Việc xung đột địa chính trị tại Trung Đông leo thang gần đây đã làm gián đoạn nghiêm trọng chuỗi cung ứng năng lượng và hóa chất toàn cầu. Trung Đông chiếm 40% sản lượng lưu huỳnh toàn cầu và 50% khối lượng thương mại đường biển, trong khi gián đoạn vận chuyển tại eo biển Hormuz đã dẫn đến tình trạng thiếu hụt nguồn cung lưu huỳnh nghiêm trọng trên toàn cầu. Trung Quốc phụ thuộc vào nhập khẩu đối với hơn 50% nguồn cung lưu huỳnh, trong đó khoảng 56% đến từ Trung Đông. Giá lưu huỳnh tăng vọt đã đẩy một số nhà sản xuất axit sulfuric sử dụng lưu huỳnh vào tình trạng thua lỗ, trong khi giá quặng pyrit cũng tăng theo, tiếp tục củng cố hỗ trợ về chi phí.

Từ tháng 3, các nhà máy axit tại nhiều khu vực lần lượt dừng hoạt động để bảo trì, khiến mức tải vận hành của ngành giảm rõ rệt. Trong khi đó, tháng 3 và tháng 4 là giai đoạn then chốt chuẩn bị phân bón cho vụ cày cấy vụ xuân, làm nhu cầu axit sulfuric tăng mạnh. Nhìn chung, sau tháng 3, giá axit sulfuric vẫn có khả năng tăng nhiều hơn giảm.

Đối với các doanh nghiệp titan dioxit theo cả quy trình clorua và quy trình sunfat, khí tự nhiên cũng là một khoản chi phí chủ chốt. Để sản xuất 1 tấn titan dioxit cần khoảng 400-500 m³ khí tự nhiên. Xung đột địa chính trị làm gia tăng bất ổn về nguồn cung năng lượng, đẩy giá khí tự nhiên lên cao và tiếp tục làm tăng áp lực chi phí cho doanh nghiệp. Đồng thời, do ảnh hưởng của xung đột, cước vận tải biển quốc tế tiếp tục tăng, chi phí vận chuyển xuất khẩu cũng leo thang tương ứng, tạo áp lực kép lên hoạt động ngoại thương titan dioxit.

Xuất khẩu titan dioxit khởi đầu thuận lợi, tồn kho thấp hỗ trợ đà tăng giá trong tháng 3

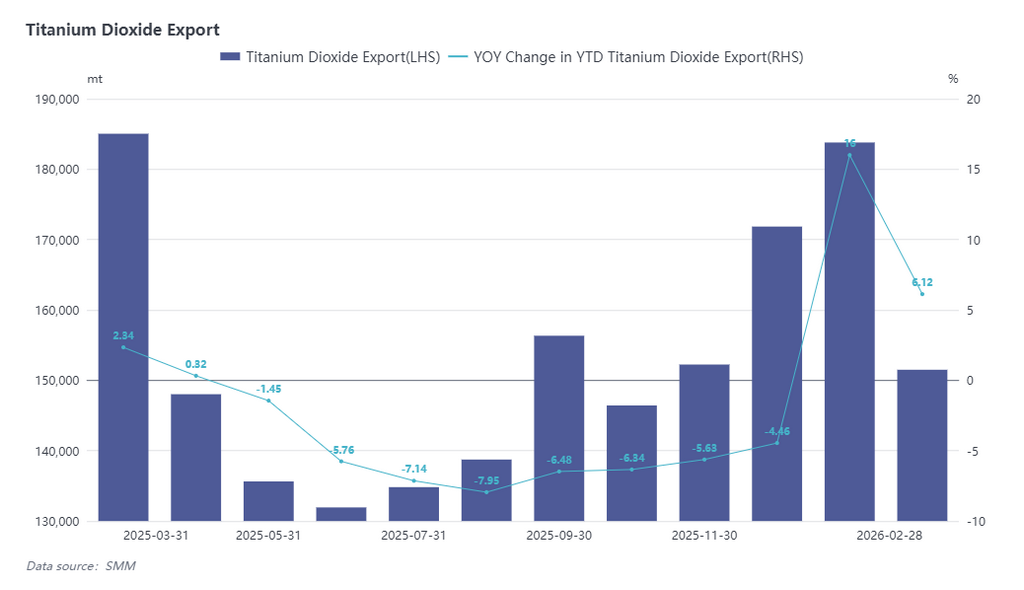

Theo số liệu hải quan mới nhất, xuất khẩu titan dioxit của Trung Quốc đạt 183.800 tấn trong tháng 1/2026, tăng 12,88% so với cùng kỳ năm trước và tăng 12,88% so với tháng trước, lên mức cao gần đây. Xuất khẩu trong tháng 2 đạt 151.500 tấn, và lũy kế xuất khẩu trong 2 tháng đầu năm tăng 6,12% so với cùng kỳ năm trước. Nhìn chung, xuất khẩu titan dioxit đã khởi đầu tốt trong năm 2026, kéo tồn kho doanh nghiệp giảm 7,2% trước Tết Nguyên đán và duy trì mặt bằng tồn kho chung ở mức thấp.

Về phía sản xuất, từ nửa cuối năm 2025, các doanh nghiệp titan dioxit đã bước vào giai đoạn thu hẹp quy mô và cắt giảm sản lượng. Sản lượng tháng 2 đạt 310.000 tấn, giảm 5,78% so với tháng trước, với tỷ lệ vận hành của ngành chỉ ở mức 70%. Sau khi hoạt động trở lại trong tháng 3, nhu cầu bổ sung hàng tồn theo nhu cầu cứng trên thị trường nội địa bắt đầu xuất hiện, cùng với việc giao hàng tập trung cho các đơn hàng tồn đọng trước đó của ngoại thương, nên tồn kho toàn thị trường vẫn duy trì ở mức tương đối thấp. Được hỗ trợ bởi mặt bằng chi phí tiếp tục vững, giá titan dioxit trong tháng 3 duy trì xu hướng tăng.

Nhìn về phía trước, các nhà sản xuất hiện có mong muốn tăng giá rất mạnh, nhưng sau mùa cao điểm nhu cầu truyền thống trong tháng 3, việc giá có thể tiếp tục tăng hay không vẫn còn chưa chắc chắn. Các yếu tố địa chính trị tiếp tục gây gián đoạn năng lực vận tải biển và giá dầu trên các tuyến Trung Đông và châu Âu, gây áp lực lên chi phí xuất khẩu. Xét về các yếu tố cơ bản cung - cầu, thị trường titanium dioxide vẫn cho thấy tình trạng dư cung, chưa có cải thiện rõ rệt về nhu cầu thực tế, thậm chí còn xuất hiện dấu hiệu suy yếu nhẹ. Tình trạng dư thừa công suất ở phía cung vẫn cần thời gian để được hấp thụ và loại bỏ dần. Về chi phí, giá axit sulfuric được dự báo sẽ tiếp tục hỗ trợ giá titanium dioxide, nhưng xu hướng giá tiếp theo vẫn sẽ phụ thuộc vào mức độ chấp nhận thực tế của thị trường hạ nguồn đối với các thư thông báo tăng giá.