SMM March 2 News:

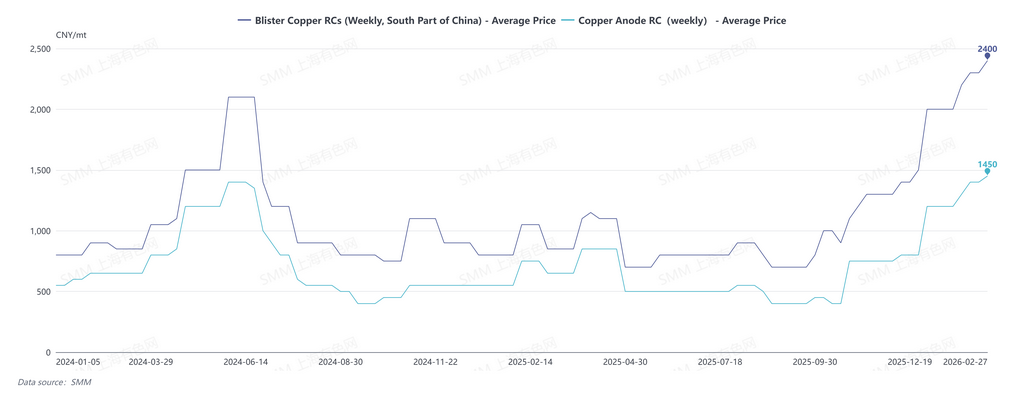

SMM's February 2026 blister copper RCs in sourth China were quoted at 2,200-2,500 yuan/mt, with an average of 2,350 yuan/mt, up 300 yuan/mt MoM; blister copper RCs in north China were quoted at 1,700-2,000 yuan/mt, with an average of 1,850 yuan/mt, up 650 yuan/mt MoM; blister copper RCs, cif China were quoted at $90-100/mt, with an average of $95/mt, unchanged from the previous month.

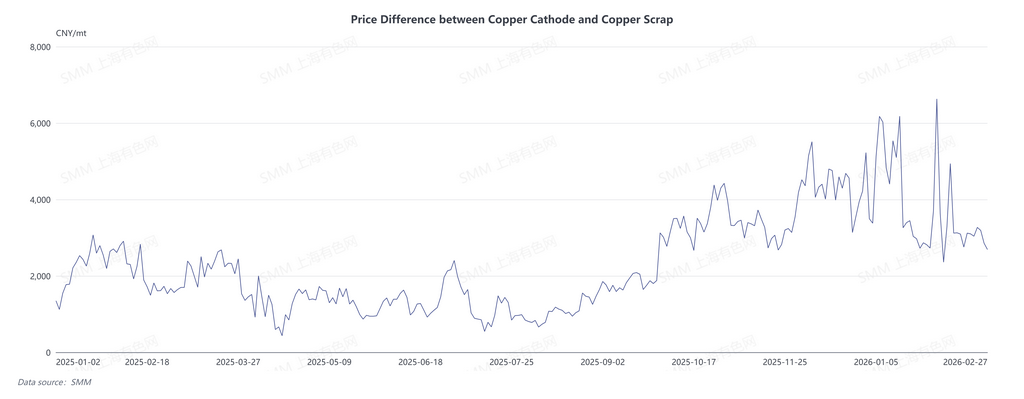

Due to continuous flow of secondary copper into smelting, the blister copper market in February 2026 remained oversupplied. China's spot blister copper RCs stayed above 2,000 yuan/mt. On the demand side, although February spanned the long Chinese New Year holiday, smelters had already completed pre-holiday stockpiling due to high cold material inventory since January. In terms of supply, as the center of copper prices rose in January, the price difference between primary metal and scrap widened, suppressing downstream consumption in the processing sector, leading to a continuous inflow of copper scrap into smelting. With smelters stopping purchases before the holiday and scrap-derived copper anode producers entering the holiday, most enterprises halted production for about half a month.

On February 27, SMM's weekly blister copper RCs in south Chinawere quoted at 2,200-2,600 yuan/mt, with an average of 2,400 yuan/mt; copper anode RCs in China were quoted at 1,400-1,500 yuan/mt, with an average of 1,450 yuan/mt, both setting new highs for processing fees after 2024.

SMM expects the loose market for copper anodes to continue throughout Q1 2026. From the supply perspective, ore-derived copper anode producers have no maintenance plans in March, keeping supply stable. Scrap-derived copper anode producers resumed production gradually after the holiday, and according to SMM, many enterprises maintained high levels of raw material inventory due to continuous imports of copper scrap during the holiday. This will ensure normal production in March, while financial pressure may increase willingness to sell. Additionally, if copper prices fluctuate at highs, slow recovery in processing demand will support the continued flow of secondary copper into smelting.

From the demand perspective, ample supply since 2026 has kept overall cold material inventory levels at smelters high, limiting market demand in March. Under the supply-demand mismatch, there is still room for China's spot blister copper and anode processing fees to rise in March. Meanwhile, with abundant domestic supply and more attractive RCs, enterprises show low interest in imported materials.

SMM analysis suggests that the turning point for China's blister copper and anode RCs may appear in April. If copper prices lack upward momentum, the price spread between primary and scrap will narrow, and under high RCs, secondary copper will shift back from smelting to processing, reducing market supply. As Q2 enters the concentrated maintenance period for China's smelters, increased cold material stockpiling needs will help rebalance the supply and demand in the anode copper market.

![BC copper the most-traded contract closed up 1% Geopolitical risks boost copper prices [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/AhHUS20251217171713.jpg)