Thị trường kỳ hạn: Qua đêm, đồng LME mở cửa ở mức 9.608,0 USD/tấn. Giá dao động trong phiên đầu, đạt mức cao nhất là 9.622,0 USD/tấn trong phiên dao động, trước khi giảm xuống mức thấp nhất là 9.557,0 USD/tấn. Sau đó, giá dao động và đóng cửa ở mức 9.567,0 USD/tấn, tăng 0,01%. Khối lượng giao dịch là 13.343 lô và lượng hợp đồng mở là 295.433 lô. Qua đêm, hợp đồng đồng SHFE 2507 mở cửa ở mức 78.080 nhân dân tệ/tấn. Giá dao động trong phiên đầu, đạt mức cao nhất là 78.100 nhân dân tệ/tấn trong phiên, trước khi dao động giảm xuống mức thấp nhất là 77.750 nhân dân tệ/tấn. Cuối cùng, hợp đồng đóng cửa ở mức 77.850 nhân dân tệ/tấn, giảm 0,18%. Khối lượng giao dịch là 30.719 lô và lượng hợp đồng mở là 171.728 lô.

[Tóm tắt cuộc họp buổi sáng SMM về đồng] Tin tức: (1) Vào ngày 28 tháng 5 (thứ Tư), nhà sản xuất kim loại Kazakhstan KAZ Minerals cho biết trong một thông cáo rằng sản lượng đồng của công ty trong quý I năm nay là 90.400 tấn, giảm 4,1% so với cùng kỳ năm ngoái. Công ty cho rằng sự sụt giảm sản lượng đồng trong quý I là do hàm lượng quặng thấp hơn, nhưng sản lượng đồng trong quý I vẫn cao hơn một chút so với mức 92.900 tấn trong quý IV năm 2024.

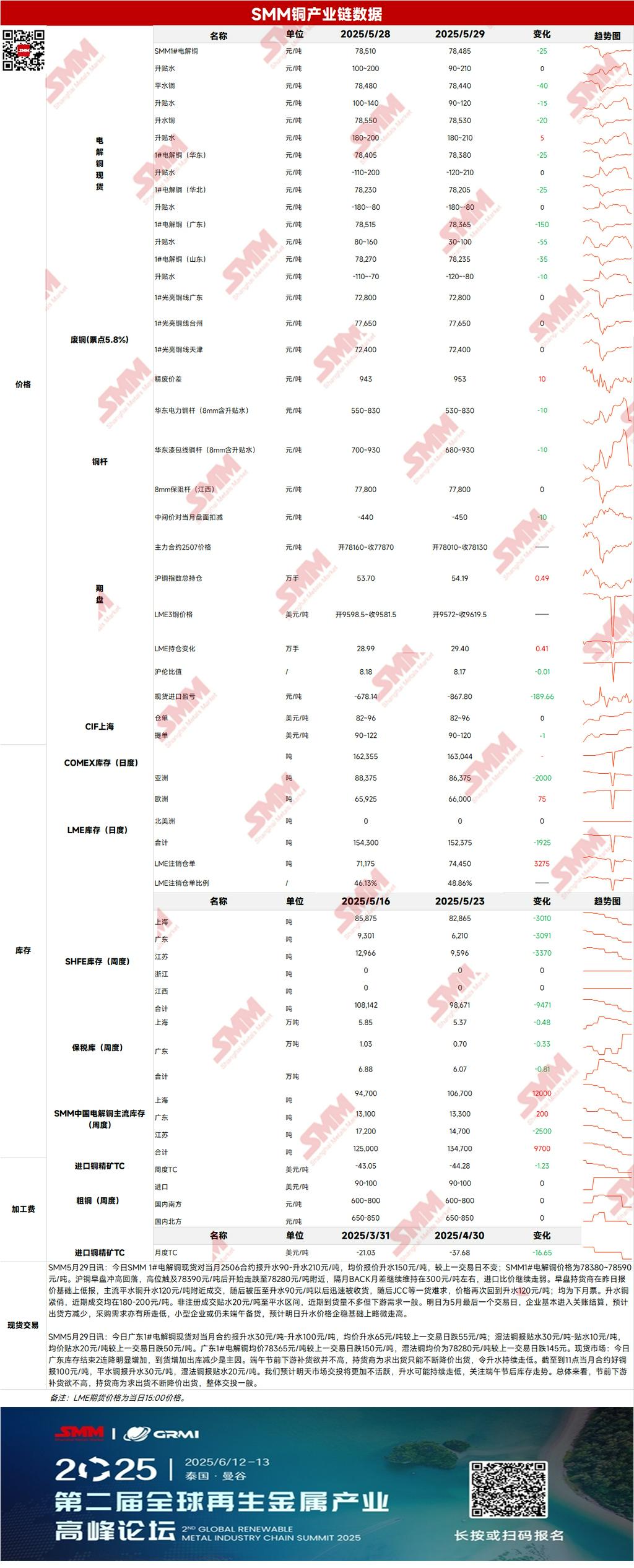

Giao dịch kỳ hạn: (1) Thượng Hải: Vào ngày 29 tháng 5, giá đồng cathode SMM loại 1 giao ngay được báo giá ở mức chênh lệch 90-210 nhân dân tệ/tấn so với hợp đồng kỳ hạn 2506 tháng giao ngay, với mức chênh lệch trung bình là 150 nhân dân tệ/tấn, không đổi so với ngày giao dịch trước đó. Giá đồng cathode SMM loại 1 là 78.380-78.590 nhân dân tệ/tấn. Đồng SHFE tăng mạnh ban đầu và sau đó giảm trong phiên sáng, đạt mức cao nhất là 78.390 nhân dân tệ/tấn trước khi giảm xuống khoảng 78.280 nhân dân tệ/tấn. Chênh lệch giá giữa hợp đồng tháng giao ngay và hợp đồng tháng tiếp theo tiếp tục dao động quanh mức 300 nhân dân tệ/tấn và tỷ lệ giá SHFE/LME tiếp tục suy yếu. Ngày mai là ngày giao dịch cuối cùng của tháng 5 và các công ty thường bắt đầu quá trình đóng sổ sách và thanh toán giao dịch. Dự kiến số lượng nhà cung cấp sẽ giảm và nhu cầu mua hàng cũng sẽ giảm một chút. Các doanh nghiệp nhỏ vẫn có thể tích trữ hàng hóa cho Lễ hội Đua thuyền Rồng. Dự kiến giá chênh lệch sẽ ổn định và tăng nhẹ vào ngày mai.

(2) Quảng Đông: Vào ngày 29 tháng 5, giá đồng cathode SMM loại 1 Quảng Đông giao ngay được báo giá ở mức chênh lệch 30-100 nhân dân tệ/tấn so với hợp đồng tháng giao ngay, với mức chênh lệch trung bình là 65 nhân dân tệ/tấn, giảm 55 nhân dân tệ/tấn so với ngày giao dịch trước đó. Đồng khai thác-ngâm tẩm (SX-EW) được báo giá ở mức chiết khấu 30-10 nhân dân tệ/tấn, với mức chiết khấu trung bình là 20 nhân dân tệ/tấn, giảm 50 nhân dân tệ/tấn so với ngày giao dịch trước đó. Giá trung bình của đồng cathode SMM loại 1 Quảng Đông là 78.365 nhân dân tệ/tấn, giảm 150 nhân dân tệ/tấn so với ngày giao dịch trước đó và giá trung bình của đồng SX-EW là 78.280 nhân dân tệ/tấn, giảm 145 nhân dân tệ/tấn so với ngày giao dịch trước đó. Nhìn chung, sự nhiệt tình mua hàng của hạ nguồn trước kỳ nghỉ là thấp. Các nhà cung cấp liên tục giảm giá để tạo điều kiện bán hàng và hoạt động giao dịch tổng thể là vừa phải.

(3) Đồng nhập khẩu: Vào ngày 29 tháng 5, giá chứng quyền là 82-96 USD/tấn, với QP là tháng 6, và giá trung bình không thay đổi so với ngày giao dịch trước đó. Giá vận đơn là 90-120 USD/tấn, với QP là tháng 6, và giá trung bình giảm 1 USD/tấn so với ngày giao dịch trước đó. Giá đồng EQ (CIF vận đơn) là 60-74 USD/tấn, với QP là tháng 6, và giá trung bình giảm 3 USD/tấn so với ngày giao dịch trước đó. Báo giá dựa trên các lô hàng dự kiến đến vào đầu tháng 6. Nhìn chung, giao dịch thị trường suy yếu. Tồn kho trong khu vực ngoại quan tiếp tục giảm trong tuần này, nhưng tốc độ giảm chậm lại một chút. Dự kiến vẫn còn dư địa giảm giá phí bảo hiểm đối với đồng nhập khẩu, nhưng nguồn cung sẽ vẫn khan hiếm trong tháng 5-6, tạo ra hỗ trợ mạnh mẽ ở mức đáy.

(4) Đồng phế liệu: Vào ngày 29 tháng 5, giá nguyên liệu đồng phế liệu không thay đổi so với tháng trước. Giá đồng trần sáng bóng ở Quảng Đông là 72.700-72.900 nhân dân tệ/tấn, không thay đổi so với ngày giao dịch trước đó. Chênh lệch giá giữa đồng tinh luyện và đồng phế liệu là 953 nhân dân tệ/tấn, tăng 10 nhân dân tệ/tấn so với tháng trước. Chênh lệch giá giữa thanh đồng tinh luyện và thanh đồng phế liệu là 1.130 nhân dân tệ/tấn. Theo khảo sát của SMM, các doanh nghiệp sản xuất thanh đồng phế liệu có ý định dự trữ nguyên liệu thấp trước kỳ nghỉ. Do đơn đặt hàng trong tay không đủ, nguồn cung nguyên liệu đồng phế liệu trên thị trường ở mức vừa phải. Tồn kho nguyên liệu thông thường của các doanh nghiệp sản xuất thanh đồng phế liệu có thể đảm bảo sản xuất bình thường trong kỳ nghỉ, vì vậy họ không vội vàng mua quá nhiều nguyên liệu đồng phế liệu.

(5) Tồn kho: Vào ngày 29 tháng 5, tồn kho đồng tinh luyện LME giảm 1.925 tấn xuống còn 152.375 tấn. Cùng ngày, tồn kho chứng quyền SHFE giảm 2.696 tấn xuống còn 32.165 tấn.

Giá: Trên mặt trận vĩ mô, sau khi Tòa án Thương mại Quốc tế Mỹ tạm dừng chính sách thuế quan "Ngày Giải phóng", Tòa án Phúc thẩm Mỹ cho phép chính sách thuế quan của Trump tiếp tục có hiệu lực tạm thời. Các quan chức dưới thời Trump bày tỏ sự tự tin mạnh mẽ về việc thắng kiện và tin rằng ngay cả khi họ thua, họ cũng có thể tìm ra các cách thức thay thế để áp đặt thuế quan. Trong khi đó, các cuộc đàm phán thuế quan sẽ tiếp tục, với ba thỏa thuận dự kiến trong vài tuần tới. Bộ trưởng Tài chính Mỹ: Thái độ của các đối tác thương mại không có thay đổi nào trong 48 giờ qua. Với triển vọng thương mại không chắc chắn, giá đồng dao động ở mức cao. Trên mặt trận cơ bản, vào ngày giao dịch cuối cùng của tháng 5, tổng lượng dự trữ trước kỳ nghỉ thấp. Dự kiến cả cung và cầu sẽ yếu vào ngày hôm nay. Tính đến thứ Năm, ngày 29 tháng 5, tồn kho đồng SMM ở các khu vực chính trên toàn Trung Quốc giảm 1.000 tấn so với thứ Hai xuống còn 138.700 tấn, tiếp tục cho thấy xu hướng giảm tồn kho. Ở các khu vực tiêu thụ chính, Thượng Hải, Quảng Đông và Giang Tô đều cho thấy xu hướng giảm tồn kho, trong đó Thượng Hải có mức giảm tồn kho lớn nhất là 1.100 tấn. Nhìn chung, với triển vọng thương mại không chắc chắn nhưng các quan chức dưới thời Trump lạc quan, dự kiến giá đồng sẽ dao động ở mức cao vào ngày hôm nay, với áp lực tăng nhẹ ở mặt trên.

[Thông tin được cung cấp chỉ để tham khảo. Bài viết này không cấu thành lời khuyên trực tiếp cho các quyết định nghiên cứu đầu tư. Khách hàng nên đưa ra quyết định thận trọng và không nên dựa vào thông tin này như một sự thay thế cho phán đoán độc lập. Bất kỳ quyết định nào được khách hàng đưa ra đều không liên quan đến SMM.]

![Đồng BC giảm mạnh sau đợt tăng nhanh, chênh lệch nghịch đảo thu hẹp dưới áp lực địa chính trị và dữ liệu [Bình luận đồng BC của SMM]](https://imgqn.smm.cn/usercenter/KytYP20251217171712.jpg)