》View SMM Aluminum Product Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Metal Spot Prices

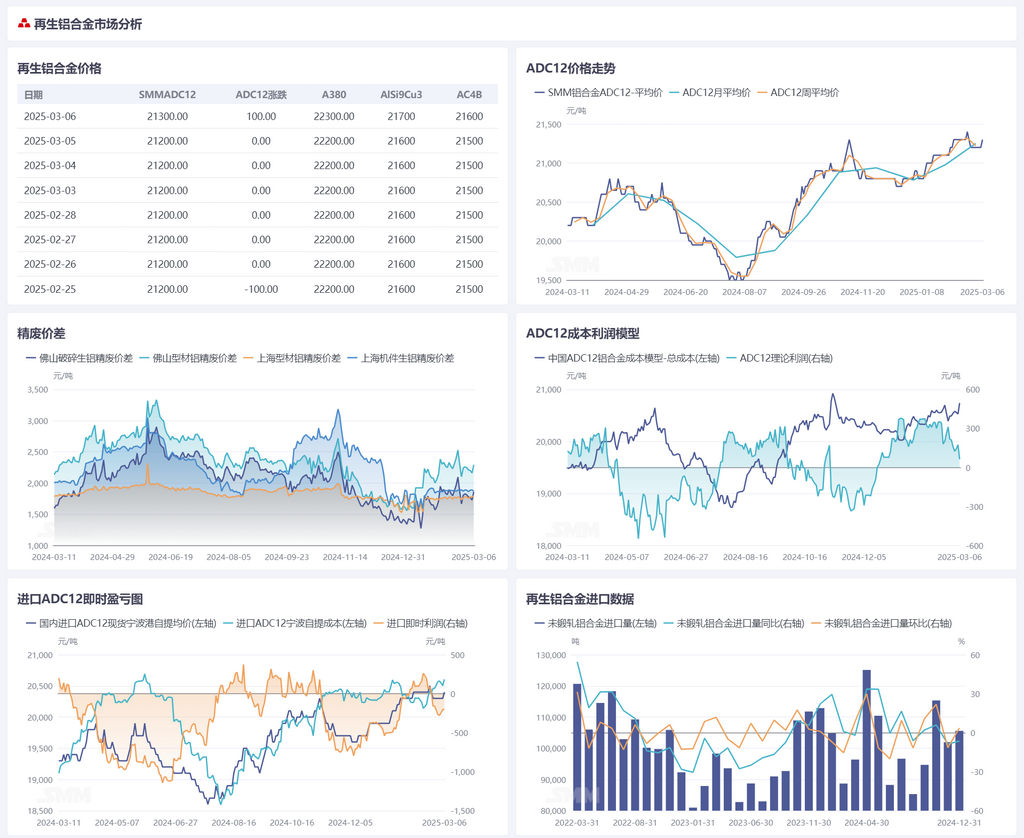

Secondary Aluminum Raw Materials:

This week, both upstream and downstream aluminum scrap markets were in a recovery phase, but primary aluminum and aluminum scrap prices continued to fluctuate at highs, with the market maintaining purchasing as needed. In terms of aluminum scrap supply, the operating rate of aluminum processing enterprises showed a rebound due to post-holiday production resumption and the approaching peak season of "Golden March and Silver April," leading to a slight increase in new scrap supply. For overseas aluminum scrap supply, the pattern of LME outperforms SHFE for primary aluminum prices remained unchanged, and overseas aluminum scrap prices stayed relatively high. Although overseas shipments recovered after the holiday, the price spread is unlikely to see a significant increase in the short term. As of Thursday this week, SMM A00 spot price was 20,800 yuan/mt, up 250 yuan/mt WoW; Shanghai aluminum tense scrap price was 18,662 yuan/mt, down 163 yuan/mt WoW; the price difference between Shanghai aluminum tense scrap and A00 aluminum narrowed by 21 yuan/mt WoW to 1,867 yuan/mt; the price difference between Foshan aluminum extrusion scrap and A00 aluminum widened by 33 yuan/mt WoW to 2,291 yuan/mt. In the short term, the domestic aluminum scrap market supply and demand are both in recovery. Recently, primary aluminum prices have fluctuated upward, with aluminum scrap prices adjusting accordingly. Considering the upcoming "Golden March and Silver April," downstream demand may improve, and aluminum scrap prices are expected to fluctuate at highs.

Secondary Aluminum Alloy:

This week, the secondary aluminum market overall showed a trend of stabilizing first and then rising. As of March 6, SMM ADC12 price increased by 100 yuan/mt WoW to 21,300 yuan/mt. On the cost side, aluminum prices fluctuated at highs at the beginning of the week, with ADC12 prices remaining stable. By Thursday, SHFE aluminum surged strongly, driving aluminum scrap prices to follow actively. The procurement costs of raw materials for secondary aluminum enterprises rose significantly. Under cost pressure, many enterprises raised their quotations, but due to limited demand-side acceptance, the actual transaction price increase was smaller than the cost rise, narrowing the theoretical profit margin for the industry. On the demand side, entering March, the market did not show a significant rebound. Orders from downstream die-casting enterprises lacked growth, and consumption recovery in end-use sectors fell short of expectations. Some enterprises reported a YoY decline in current order volumes, which limited the upward momentum of ADC12 prices and highlighted the suppressive effect of demand on prices. On the supply side, most enterprises maintained normal production rhythms, with overall industry supply relatively stable. On the import side, overseas ADC12 prices rose to a high range of $2,480-2,520/mt, with immediate import losses widening to around 200 yuan/mt, keeping the import window closed. Overall, ADC12 prices in the short term are likely to continue the tug-of-war between cost support and demand suppression. If consumption recovery remains weak, the upside room for prices may be limited.