In recent years, Indonesia's energy transition has shown clear signs of acceleration. As the government sets more ambitious renewable energy targets, and as mining decarbonisation, island-based power system upgrades, floating PV project development and local manufacturing build-out continue to advance, the long-term growth potential of Indonesia's solar PV, energy storage and microgrid markets is opening up further.

During the recent Indonesia Critical Minerals Conference (ICM) and its Coal and Energy Transition Forum, SMM exchanged views with local PV companies, energy storage and energy system solution providers, mining-related companies, industry associations, and representatives from Indonesia's state-owned power utility PLN. Based on these discussions, SMM understands that Indonesia's energy transition is not being driven solely by PV installation targets. Instead, it is gradually moving from policy planning toward concrete application scenarios. Mining energy transition, weak-grid and off-grid scenarios, floating PV, local module manufacturing, energy storage systems, and demand for green electricity and carbon management are becoming the main themes in Indonesia's renewable energy market.

Clear policy targets, but short-term implementation remains constrained by grid conditions and project mechanisms

From a policy perspective, the Indonesian government is increasing its support for renewable energy. Whether viewed through long-term PV installation targets or PLN-related power development plans, Indonesia is seeking to improve its energy structure through solar, hydropower, geothermal, wind power and energy storage, while gradually reducing its dependence on traditional fossil fuels.

However, based on actual market feedback, Indonesia's energy transition is still at the stage of 'clear targets, cautious implementation.' Indonesia is a typical archipelagic country. Its main grid mainly covers Java and Bali, while many other islands still rely more heavily on microgrids, captive power systems or diesel generators. Connecting remote islands or mining areas fully to the main grid would involve high construction costs and significant transmission and distribution losses. As a result, grid conditions have become one of the core practical constraints affecting the implementation of renewable energy projects in Indonesia.

At the same time, project approval, land coordination, financing conditions, PPA mechanisms, local content requirements and the execution pace of PLN projects also affect the actual progress of PV and energy storage projects. Some companies believe that Indonesia's medium- to long-term market potential is clear, but the market is unlikely to see a simple and rapid increase in installations in the short term. Project implementation still requires coordination among policy, grid infrastructure, financing and end-user demand.

Mining energy transition is becoming the most certain incremental demand scenario

Compared with ordinary ground-mounted PV projects, mining and industrial power consumption scenarios are becoming a more commercially logical direction in Indonesia's energy transition. Indonesia has abundant nickel, copper, bauxite, silica and other mineral resources. Mining and smelting projects are often located in Sulawesi, Kalimantan and other areas where grid infrastructure is relatively weak. Some mining areas have long relied on coal power, diesel power or captive power plants, resulting in high electricity costs, while also facing traditional energy price volatility and carbon emission pressure.

Based on corporate discussions, the energy transition in mining is no longer only an environmental requirement. It is also closely linked to energy security, cost control, export competitiveness and downstream customer access. For nickel, copper and other critical metals companies, product carbon footprint, ESG requirements, battery passport requirements and potential carbon costs may all become important constraints when exporting to Europe, Japan, South Korea and other markets. If mining companies can increase their share of green electricity consumption, they will be able to reduce unit product carbon emissions and improve their competitiveness in the international supply chain.

Against this backdrop, combined solutions involving solar PV, wind power, energy storage, diesel backup and microgrid control systems are becoming an important path for mining energy transition. In weak-grid or off-grid areas, wind-solar-storage systems can not only reduce the overall levelised cost of electricity, but also improve power supply stability and reduce mining companies' reliance on diesel and external grids.

Microgrids and energy storage are key supports for Indonesia's renewable energy development

The challenge of Indonesia's energy transition is not simply 'how much PV capacity to build,' but how to ensure that renewable energy can operate stably under complex grid conditions. Due to dispersed islands, complex load structures and insufficient grid strength in some regions, relying solely on PV modules cannot solve all problems. Energy storage systems, PCS, EMS, inverters, transformers and intelligent dispatching capabilities will be critical to whether a project can operate stably.

SMM believes that Indonesia has significant renewable energy development potential, but its grid structure is relatively complex. Many projects cannot be solved by installing a single type of equipment alone. Instead, they require comprehensive consideration of system matching, grid stability, long-term operation and maintenance, and local delivery capability. For weak-grid, microgrid and floating PV projects, integrated system solutions can help reduce compatibility issues among different equipment, while improving system stability and service response efficiency.

At the same time, SMM learned from corporate discussions that Indonesia's mining energy systems are expected to gradually shift from single-equipment procurement toward integrated solutions combining 'wind-solar-storage + AI + carbon management.' Especially given the intermittency of wind and solar generation, AI capabilities can be applied to weather forecasting, generation-side dispatching, demand-side matching and system operation optimisation, thereby improving the economics and stability of new power systems.

Therefore, future competition in Indonesia's renewable energy market may no longer focus only on the price of individual products such as modules, inverters or storage batteries. Instead, competition is likely to shift toward system integration capability, weak-grid adaptability, long-term O&M capability and local delivery capacity.

Floating PV is expected to become a distinctive application scenario in Indonesia

In addition to mining energy transition, floating PV is another important direction worth monitoring in the Indonesian market. Indonesia has numerous islands, relatively abundant reservoir and water resources, and some regions also face land constraints, giving floating PV a strong application foundation. In recent years, the implementation of large-scale floating PV projects such as Cirata has provided a demonstration effect for similar projects in Indonesia.

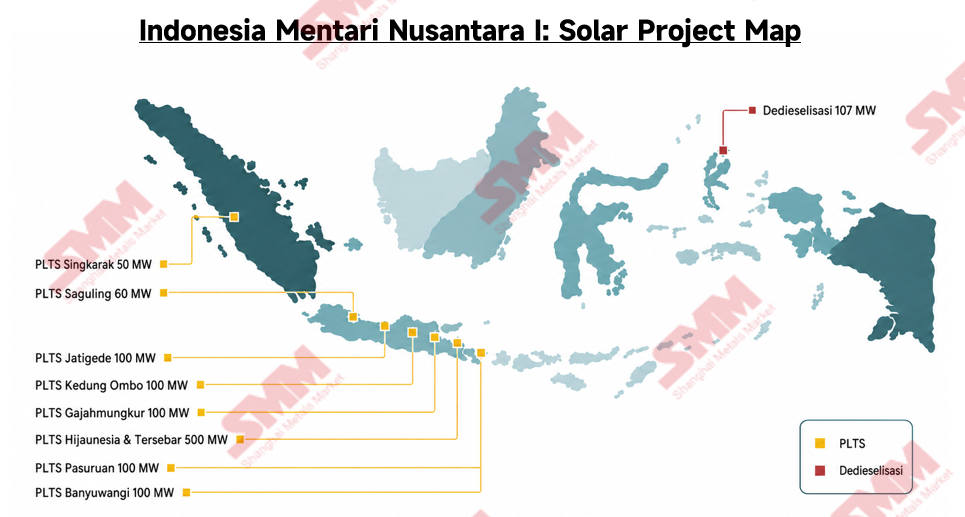

According to SMM, several floating PV projects are still being advanced in Indonesia in 2026, including the Karangkates floating project, with a scale of approximately 130MWdc, and the Saguling floating project, with a scale of approximately 92MWdc. These projects involve TKDN 4.0 waivers, reflecting the need for Indonesia's floating PV market to balance policy requirements with project execution efficiency amid local supply capacity, project timelines and module technology selection.

From the perspective of project demand, large-scale floating PV projects have relatively high requirements for system solutions. They need to take into account module efficiency, inverter selection, cable costs, floating systems, O&M convenience and long-term stability. Compared with ordinary ground-mounted projects, floating PV places higher requirements on power generation per unit area, equipment reliability and system integration capability. Therefore, high-efficiency modules, central inverters, energy storage and intelligent O&M solutions are expected to see more application opportunities in such projects.

Overall, floating PV is expected to become one of the more representative application scenarios in Indonesia's renewable energy market. On the one hand, it can help ease land constraints for certain projects. On the other hand, it can also support the application of high-efficiency modules and system-based solutions in the Indonesian market. However, future project scale-up will still depend on local content policy implementation, project approval, grid connection conditions and financing arrangements.

TKDN local content requirements support domestic manufacturing, but cost premiums remain significant

Another major theme in Indonesia's energy transition is local manufacturing. As TKDN local content requirements continue to advance, demand for locally manufactured modules from Indonesian government and PLN-related projects is increasing. Local module manufacturers have certain market opportunities in government projects and projects with mandatory local content requirements.

According to SMM, some Indonesian government and PLN-related projects are expected to gradually enter the execution stage in 2026, with approximately 1.2GW of project demand closely related to TKDN 4.0 local content requirements. As these projects require modules that meet TKDN requirements, demand for localised modules is still mainly driven by government projects, PLN projects and mandatory local content application scenarios.

Source: SMM

However, from a pricing perspective, local TKDN modules are priced significantly higher than Chinese imported modules. According to SMM research, TKDN module prices for projects above 10MW are approximately 14.5 US cents/W, while prices for small-scale projects may reach around 16 US cents/W. Modules with around 40% TKDN content are typically priced around 20%-30% higher than Chinese imported modules. This premium mainly stems from local manufacturing costs, insufficient supply chain support, differences in technology efficiency and policy-based pricing mechanisms.

SMM believes that Indonesian local modules do not fully compete directly with Chinese imported modules. Instead, they are mainly used in government projects, PLN projects and application scenarios with strict local content requirements. In the future, Indonesia's module market may gradually form two pricing systems: one market-based pricing system centred on imported high-efficiency modules, and another local project pricing system centred on TKDN modules. For price index development and market research, distinguishing between local TKDN module prices, imported module prices and the premium between the two will become increasingly important.

Are Indonesia's TKDN restrictions a benefit or a burden?

Another major theme in Indonesia's energy transition is local manufacturing. As TKDN local content requirements continue to advance, demand for locally manufactured modules from Indonesian government and PLN-related projects is increasing. Local module manufacturers have certain market opportunities in government projects and projects with mandatory local content requirements.

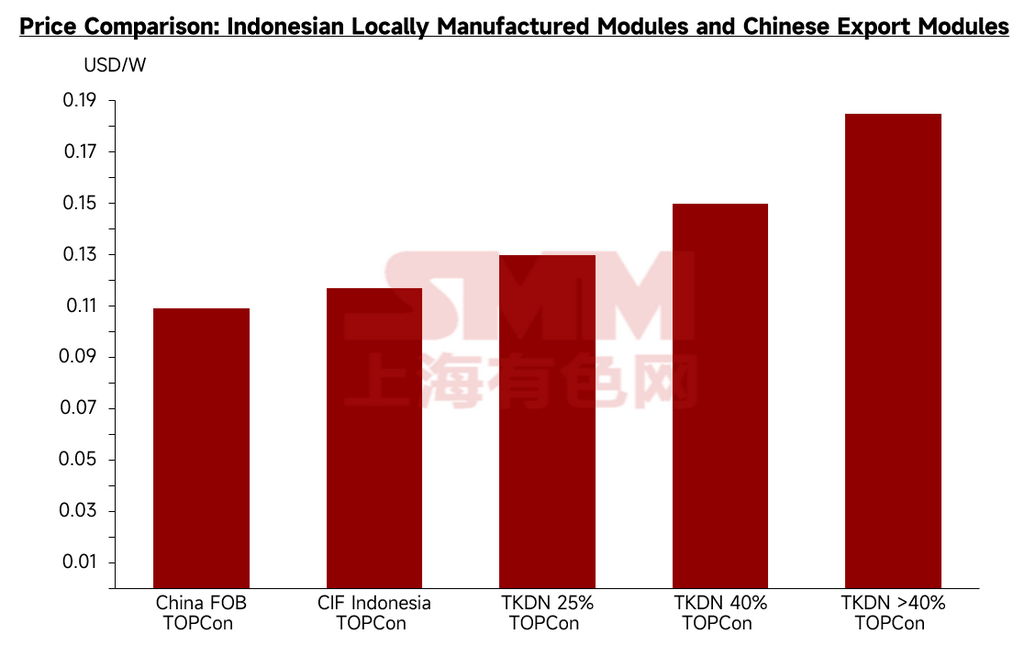

According to SMM, the current FOB price of Chinese TOPCon modules is around USD0.110/W, while the CIF Indonesia price for Chinese TOPCon modules is approximately USD0.114-0.120/W. In comparison, prices for Indonesian local TKDN modules are significantly higher overall. TKDN 25% TOPCon modules are priced at around USD0.130/W, TKDN 40% TOPCon modules at around USD0.150/W, and TOPCon modules with TKDN content above 40% may reach approximately USD0.185/W.

In terms of price differences, TKDN 25% modules carry a relatively limited premium of around 5% over Chinese CIF Indonesia modules. However, as local content requirements increase, the cost premium expands significantly. TKDN 40% modules are priced around 21% higher than Chinese CIF Indonesia modules, while modules with TKDN content above 40% are around 49% higher. This difference mainly stems from local manufacturing costs, insufficient supply chain support, limited production scale, differences in technology efficiency and policy-based pricing mechanisms.

Source: SMM

In the short term, TKDN requirements can help improve the utilisation rate of local module capacity in Indonesia, support the formation of a more complete local manufacturing ecosystem across cells, modules, glass, aluminium frames and other auxiliary materials, and help reshape Indonesia's PV manufacturing chain and local employment system.

However, from the perspective of project economics, TKDN restrictions also create a cost-benefit challenge for Indonesia's future PV development. On the one hand, local content requirements can strengthen Indonesia's PV supply chain autonomy, enhance domestic manufacturing capability and provide local industrial support for government and PLN projects. On the other hand, higher TKDN module prices will increase initial project investment costs and may affect PPA prices, investment payback periods and developer enthusiasm for certain projects.

SMM believes that Indonesian local modules do not fully compete directly with Chinese imported modules. Instead, they are mainly used in government projects, PLN projects and application scenarios with strict local content requirements. In the future, Indonesia's module market may gradually form two pricing systems: one market-based pricing system centred on imported high-efficiency modules, and another local project pricing system centred on TKDN modules. For Indonesia's energy transition, TKDN policy can support the restructuring of the local manufacturing chain. However, if the cost premium remains high for an extended period, it may also constrain the pace of PV project deployment. Therefore, how to strike a balance between the benefits of local manufacturing and project development costs will become a key issue for the future development of Indonesia's PV market.

Mining decarbonisation will drive rising demand for 'green electricity + carbon management'

Within the critical metals supply chain, the significance of energy transition is expanding from 'reducing electricity costs' to 'reducing carbon footprint.' In particular, during the development of nickel, copper, silica and other mineral resources, end customers may increasingly focus on the power source, carbon emission intensity and traceability of raw material production.

Envision Energy noted in discussions that its strengths lie not only in providing green power systems, but also in carbon management capabilities. Through an IoT-based carbon management system, companies can calculate end-to-end carbon emissions across mining, smelting and production processes, and further allocate emissions to the carbon footprint of each unit of product. Compared with traditional static calculations using Excel, real-time tracking systems can better support companies in connecting with certification bodies, shortening certification cycles and reducing certification costs.

For Indonesian mining companies, low-carbon capability may in the future affect not only production costs, but also the ability of products to enter international markets. As downstream battery, automotive and metals-consuming companies raise their requirements for low-carbon raw materials, Indonesian mining companies' demand for green electricity, energy storage, carbon management and verifiable green power is expected to continue rising.

SMM View: Indonesia's energy transition will move from 'installation targets' toward 'system solutions'

Overall, Indonesia's energy transition is gradually moving from policy-target-driven development toward concrete application scenarios across mining, islands, floating PV and industrial parks. In the short term, Indonesia's PV market still faces constraints related to grid connection, project financing, PPA mechanisms, local content requirements and project execution pace, and actual installation growth will take time to materialise. However, in the medium to long term, Indonesia's unique archipelagic structure, abundant mineral resources, high-cost captive power scenarios and downstream low-carbon supply chain requirements will continue to create demand for PV, energy storage, microgrids and carbon management systems.

In the future, the core competitiveness of Indonesia's renewable energy market may no longer be limited to single-module pricing, but may shift toward more comprehensive system capabilities. For renewable energy companies, those that can provide integrated solutions suited to weak grids, off-grid systems, floating PV and mining load characteristics are more likely to secure long-term market share in Indonesia's energy transition.

For SMM, future research on the Indonesian market will also need to extend beyond traditional module pricing to TKDN module premiums, local manufacturing costs, floating PV project progress, mining green power demand, energy storage system costs, microgrid configuration, low-carbon mineral export requirements, and upstream raw material pricing systems such as silica and quartz sand. As Indonesia's energy transition enters a more practical project implementation phase, price transparency, cost assessment and data services will become increasingly important.

Written by: Ryan Tey Tze Yang | SMM PV Analyst

![[Solar: HVR Solar to build 1.2GW TOPCon cell factory in India]](https://imgqn.smm.cn/usercenter/DCwfK20251217171737.jpg)

![[Solar: European Energy commissions 148MW solar park in Latvia]](https://imgqn.smm.cn/usercenter/LMmrH20251217171737.jpg)

![[Solar: FRV secures 2.3GW of grid capacity in Germany]](https://imgqn.smm.cn/usercenter/Jzkij20251217171737.jpg)