At 4:15 PM on June 8, 2026, a ladle explosion at the SMS-1 steelmaking shop of Visakhapatnam Steel Plant (VSP) — operated by Rashtriya Ispat Nigam Limited (RINL) — unleashed molten metal at over 1,500°C onto the working platform below Caster-2. According to a preliminary report by India's Chief Inspector of Factories, the cause was a sudden release of gas entrapped within the liquid steel, which ruptured the ladle seal before the sliding gate was opened, triggering a catastrophic spill. The resulting fireball reached the shop ceiling and ignited the overhead cranes. As of the early hours of June 10, 2026, eight workers are confirmed dead — five regular employees and three contract workers — and six others remain in critical care with severe burns. Former Chief Minister Jaganmohan Reddy publicly accused years of mass workforce reductions of systematically dismantling the plant's safety framework.

I. Incident Reconstruction & Government Response

1.1 How the Accident Unfolded

The continuous caster (Caster-2) in SMS-1 is the central link in VSP's steelmaking chain. Liquid crude steel flows from the ladle through the tundish into the casting machine, where it solidifies into billets for downstream rolling. Under normal procedure, a ladle carrying approximately 300 tonnes of liquid steel is rotated and centered above the tundish, after which the sliding gate is manually opened to begin pouring. At this critical juncture, accumulated gas pressure breached the ladle's bottom seal before the gate was opened, triggering a catastrophic molten steel overflow.

The liquid metal surged out at a rate of hundreds of litres per second, instantly engulfing workers operating equipment on the platform below. As the incident coincided with a shift changeover, the platform was relatively crowded, compounding the casualty toll.

1.2 Government Compensation & Relief Measures

In the wake of the accident, India's central and state governments moved swiftly:

- Prime Minister Modi disbursed funds from the Prime Minister's National Relief Fund: INR 200,000 (~USD 2,400) per fatality; INR 50,000 (~USD 600) per critically injured worker.

- Steel Minister Kumaraswamy announced dedicated compensation: INR 2.5 million (~USD 30,000) per fatality; INR 1 million (~USD 12,000) per injured worker.

- Ancillary welfare guarantees: bereaved families may continue residing in plant housing until statutory retirement age; children are entitled to free education; eligible family members may receive permanent plant employment.

- The Ministry of Steel constituted a 3-member independent expert panel, led by the director of SAIL's Bokaro Steel Plant, to investigate mechanical failures and management lapses.

II. Company Profile: RINL and Visakhapatnam Steel Plant

2.1 Corporate Overview

RINL (Rashtriya Ispat Nigam Limited) is a 100% Government of India-owned enterprise under the Ministry of Steel. Its sole production asset, Visakhapatnam Steel Plant (VSP), is India's only coastal integrated steel plant and one of the country's largest state-owned steel facilities. VSP operates on the blast furnace–basic oxygen furnace (BF-BOF) integrated route with a rated capacity of 7.3 million tonnes of liquid steel per annum. The plant spans over 33,000 acres and holds a captive deep-water port (AGPL), enabling direct sea delivery of iron ore, coking coal, and other raw materials — a meaningful cost advantage. Its product mix focuses on long products: TMT rebar, wire rod coils (WRC), structural sections (angles, channels, beams), and billets, widely deployed in India's infrastructure, metro rail, and defence projects.

2.2 Product Mix and Market Position

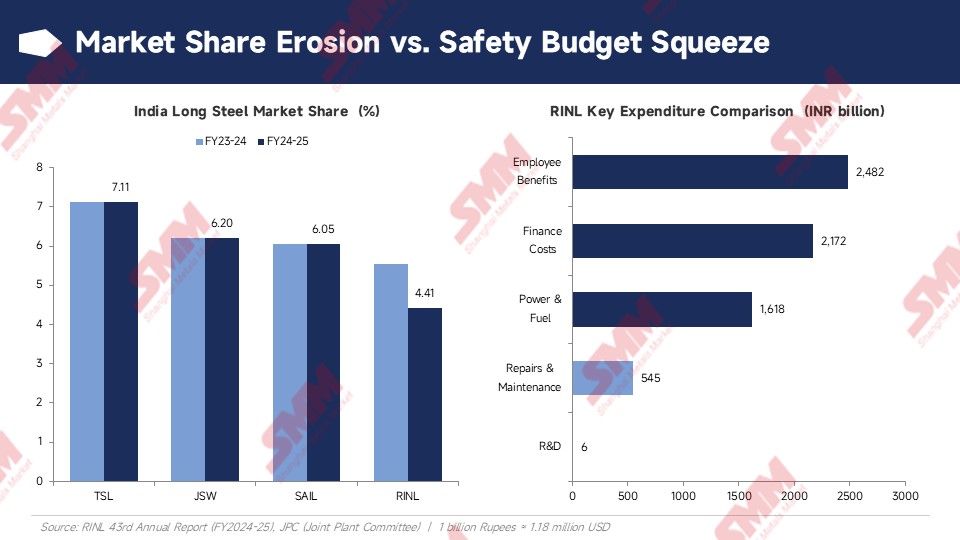

According to RINL's 43rd Annual Report (FY2024-25): RINL's share of India's long steel market (bars and structurals) fell from 5.55% in FY2023-24 to 4.41% in FY2024-25, ranking fourth nationwide — trailing Tata Steel (TSL, 7.11%), JSW Steel (6.20%), and SAIL (6.05%).

III. Financial Autopsy: How the Balance Sheet Foretold Disaster

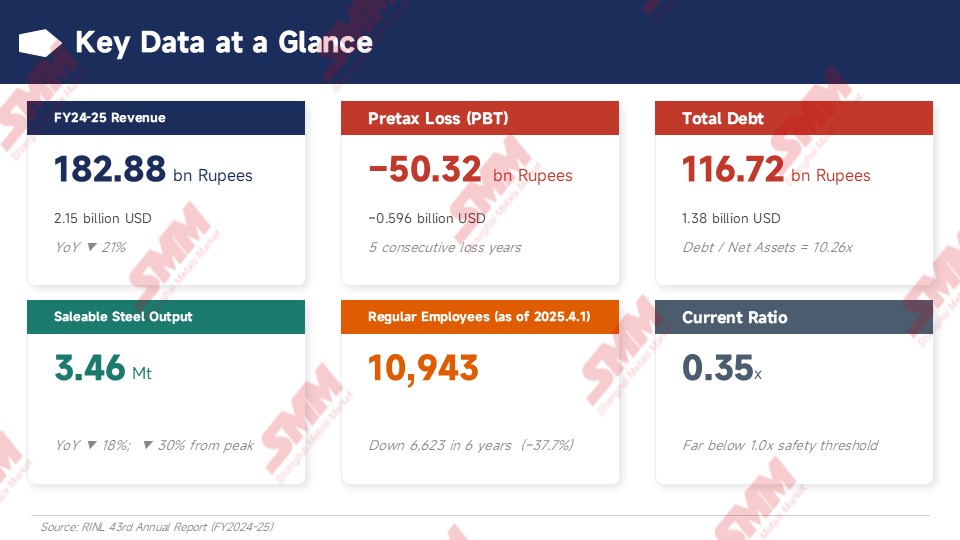

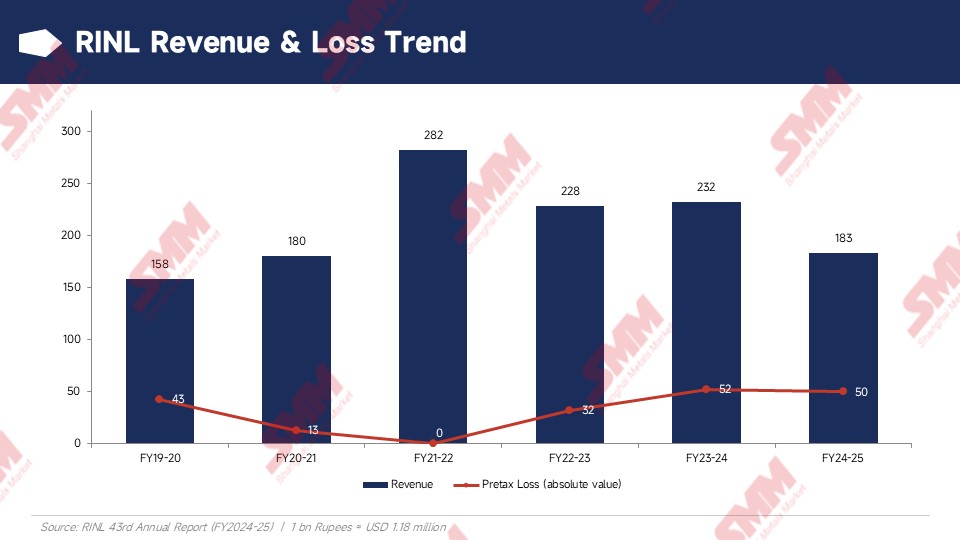

Tracing RINL's recent financials, the warning signs were unmistakable. In FY2021-22, VSP reached its historic production and revenue peak, with revenue climbing to USD 3.3 billion. What followed was a sharp reversal: weighed down by falling global steel prices, surging raw material costs, and an escalating debt burden, revenue declined for three consecutive years, reaching USD 2.15 billion in FY2024-25 — a year-on-year collapse of 21%.

More critically, RINL has reported losses for five consecutive fiscal years. The FY2024-25 pretax loss (PBT) reached USD 0.596 billion, with a net after-tax loss of USD 0.164 billion — the apparent narrowing owed not to operational improvement, but to a government equity injection of USD 0.86 billion. EBITDA remained negative; operating cash flows could not cover any capital expenditure.

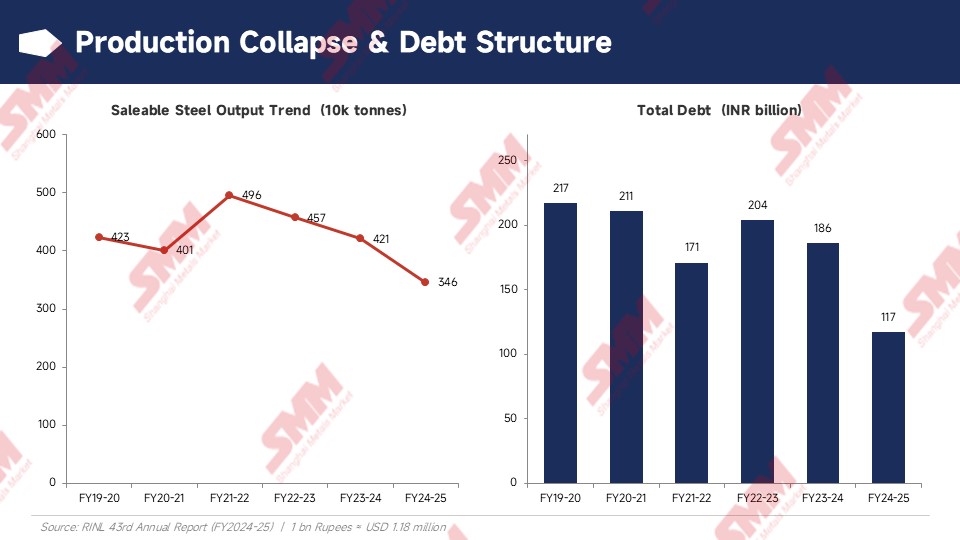

The production-side collapse was equally alarming. Between May and September 2024, with working capital exhausted and raw material supply disrupted, the company was forced to idle two of its three blast furnaces, leaving the plant running on a single furnace at its lowest point. FY2024-25 saleable steel output was just 3.46 million tonnes — a decline of over 30% from the FY2021-22 peak of 4.96 million tonnes. The third blast furnace was not relit until June 27, 2025.

On the debt side, following the government's USD 1.35 billion integrated recovery package, total liabilities declined from their peak, but the remaining USD 1.38 billion in outstanding debt still produces a debt-to-net-assets leverage ratio of 10.26x. Annual interest charges alone run to USD 0.257 billion — well beyond the company's actual earnings capacity.

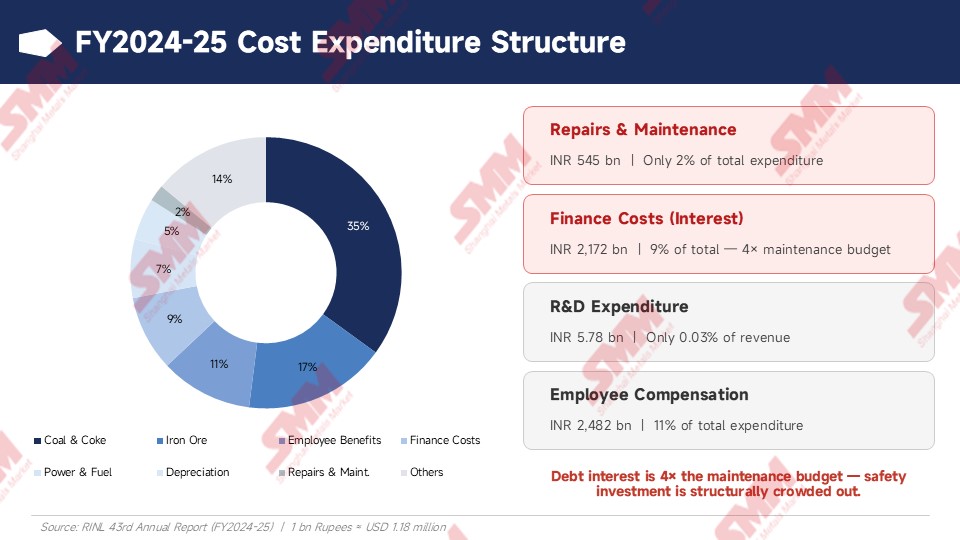

A breakdown of the cost structure reveals the systematic crowding-out of safety spending. In FY2024-25, repairs and maintenance expenditure stood at just USD 0.064 billion — less than 2% of total costs — while debt finance charges (interest) consumed USD 0.257 billion, exactly four times the maintenance budget. R&D spend was USD 0.0007 billion, representing 0.03% of revenue. IoT-based ladle monitoring, automated sliding-gate diagnostics, and other modern safety systems were effectively non-existent.

IV. Workforce Reduction & Technological Stagnation: How Misaligned "Cost-Cutting" Dismantled the Safety Moat

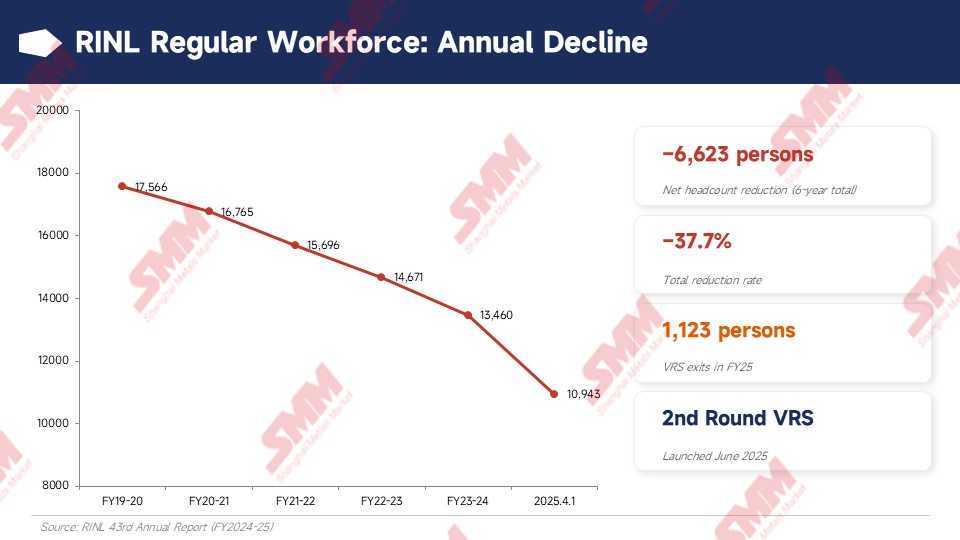

Headcount data tell a stark story. As of April 1, 2025, RINL's regular employee count had fallen to just 10,943 — down from 17,566 in FY2019-20, a net reduction of 6,623 workers (−37.7%) over six years. Within FY2024-25 alone, 1,123 employees left under the Voluntary Retirement Scheme (VRS), saving an estimated USD 0.024 billion per year in wage costs. More alarmingly, the annual report explicitly notes that a second round of VRS invitations was issued on June 14, 2025 — the redundancy programme is ongoing.

The reduction in regular headcount ran in parallel with the mass dismissal of contract workers. Former Andhra Pradesh Chief Minister Jaganmohan Reddy alleged after the accident that approximately 6,500 contract workers had been dismissed over the past two years, alongside 3,000 VRS exits and 1,500 age-based retirements. These numbers paint a deeply troubling picture: behind the annual savings of hundreds of millions of dollars in wage costs lies a rapid erosion of institutional knowledge in a 1,500°C operating environment, and an exponential rise in operational risk as undertrained contract workers take over high-hazard roles.

RINL's annual report discloses a labour productivity figure of 496 tonnes of crude steel per employee per year. Placed on the global steelmaking timeline, this figure is severely lagging. By contrast, China's leading steel groups (such as Baowu's smart manufacturing hubs) and modern mills in Japan and South Korea — leveraging AI vision recognition, comprehensive IoT sensors, and automated ladle tracking systems — have already pushed total-factor labour productivity to 1,000–1,500 tonnes of crude steel per employee per year, achieving genuine dark-factory, operator-free high-hazard furnace operations.

VSP's critical failure was not the headcount reduction per se, but its systemic misalignment. Management unilaterally eliminated thousands of experienced furnace operators — workers carrying irreplaceable muscle memory for front-of-furnace emergency response — without any accompanying capital expenditure on automation, and without deploying a single intelligent temperature-monitoring or ladle breakout detection system. Filling labour-intensive, high-hazard positions with cheap outsourced workers is not 'quality-efficiency improvement' in an industrial upgrade — it is a predatory cost reduction that cannibalises the safety floor.

V. Market Impact and Trade Flow Transmission

5.1 Immediate Capacity Shock and Regional Supply-Demand Rebalancing

From a supply-demand balancing perspective, the shutdown of SMS-1 and the plant-wide safety review will tear a significant gap in the supply side for South India. With a rated capacity of 7.3 million tonnes of crude steel per annum, and factoring in VSP's typical blast furnace and converter utilisation cycles, the incident is estimated to remove 150,000–200,000 tonnes per month of long products and semi-finished goods from the regional supply base.

This sudden regional supply deficit will generate clear and immediate trade-flow transmission effects: independent rolling mills in the surrounding region that have lost their stable domestic feedstock supply will be forced into panic buying on the seaborne market. This will not only temporarily freeze India's ability to export semi-finished products, but will directly translate into incremental import inquiries for billets from neighbouring countries — particularly Southeast Asia and the Middle East — providing a liquidity floor under Asian seaborne semi-product pricing in Q3 2026.

5.2 Import-Export Inversion and Resource Inflows

Since 2024, India has formally become a net steel importer, with the annual trade deficit surpassing 2.3 million tonnes. The VSP shutdown will further tighten India's exportable surplus, while forcing domestic mills to step up procurement of scrap and low-cost billets from the Far East — particularly Russia — thus providing a degree of support to Asian raw material pricing.

On the international price front, India's HRC export offers in the first week of June 2026 were holding in the range of USD 555–560 per tonne FOB, carrying limited competitiveness in global steel markets. The import-export inversion is unlikely to reverse in the near term.

5.3 Billet Trade Flow Restructuring: India's Exit and the Strategic Window for Chinese Exports

At the micro level of cross-border tender flows, VSP's sudden shutdown is landing a precise blow on the existing pricing equilibrium in the Middle East semi-finished market. In recent weeks, RINL had been an active participant in overseas billet tenders, with batches of low-price Indian material flowing seaborne into Saudi Arabia and other Middle Eastern markets. Under the prevailing procurement logic of Middle Eastern buyers — who strongly favour the lowest-cost competitive tender — India has traditionally served as a powerful downward price anchor in the region.

With SMS-1 now fully sealed, the physical interruption of liquid crude steel output means RINL's capacity to export semi-finished products has been effectively frozen. This supply vacuum will trigger a clear substitution effect:

- Removal of Indian low-price disruption: The Middle East market will temporarily lose a key pricing floor anchor. Buyers' strategy of leveraging cheap Indian supply to extract concessions from other suppliers will lose its leverage.

- Confirmed upside for Chinese exports: For Chinese billet resources facing compressed domestic demand and seeking export channels, this opens an exceptional strategic window. Chinese billet exports currently carry strong underlying competitiveness. In the absence of Indian material competing head-to-head at the low end, Chinese billet exports to Saudi Arabia and the broader Middle East are well-positioned not only to fill the supply gap but to achieve a dual improvement in both volume and price through Q3 2026.

5.4 EU Trade Barriers and CBAM Pressure: A Compound Squeeze

On the macro trade policy front, the EU's revised steel safeguard measures are set to take effect on July 1, 2026, while the CBAM (Carbon Border Adjustment Mechanism) transitional reporting requirements are already imposing real carbon cost traceability obligations on BF-BOF integrated mills. Against a backdrop of still-high domestic downstream operating rates (pre-monsoon construction sprint), the combination of domestic and external pressures means Indian steelmakers cannot effectively pass carbon costs onto European buyers in the near term. Domestically, the compliance and safety audit costs triggered by the accident are set to rise exponentially.

VI. Privatisation at Risk: Deep Systemic Implications

RINL is currently at the epicentre of the Indian central government's privatisation agenda. The eruption of this catastrophe may prove to be a historic inflection point that derails — or fundamentally resets — RINL's privatisation trajectory. On one hand, the accident has exposed deep-seated equipment deterioration and management dysfunction, forcing any prospective private acquirer to substantially revise upward their estimates of safety remediation costs. On the other hand, labour unions and political opposition forces will leverage this tragedy to mount vigorous resistance against any privatisation model predicated on the logic of 'cutting labour costs to make the asset saleable.'

Looking back historically, this is far from VSP's first serious safety incident: in December 2020, a molten steel overflow in the same steelmaking shop injured four workers severely; in 2016, an explosion at the plant's oxygen facility killed 16; in 2012, an explosion during commissioning of the new steelmaking shop killed 19 — one of the worst accidents in India's steel industry history. This sequence of tragedies demonstrates that years of chronic under-investment in maintenance, compounded by successive rounds of workforce reduction, have elevated the safety risk to a systemic level that cannot be remedied through localised fixes.

Conclusion: When the P&L Outweighs Liquid Steel

The root cause of this catastrophe is not a single operational error. It is the ultimate reckoning of a state-owned steel enterprise that spent years trading its safety floor for accounting survival. Debt interest costs four times the maintenance budget. Headcount down by more than one-third in six years. High-hazard positions filled by cheap contract workers. Together, these figures form the coldest possible footnote to 1,500°C of spilled molten steel.

SMM recommends that industry participants track three critical signal lines closely:

- Vessel call data at Indian customs ports next week, and spot TMT rebar transaction anomalies in the southern region;

- Any suspension or resumption of RINL's privatisation negotiations;

- The scope and timetable of the industry-wide high-hazard equipment safety audit to be jointly launched by India's Ministry of Labour and Ministry of Steel.

The regional capacity cycle may be approaching a long-cycle inflection point — transitioning from 'excess expansion' to 'recession-mode fault frequency.' SMM will continue to track developments on this subject and provide timely updates to supply-demand and price forecasts.

![[National Railway's Coal Shipments Reach 870 Million mt, January-May]](https://imgqn.smm.cn/usercenter/FFFrV20251217171719.jpg)

![[US Steel Imports Up 5.9% MoM to 1.874 Million Short Tons in April]](https://imgqn.smm.cn/usercenter/UrrTG20251217171717.jpg)

![[Where Did the 2 Trillion Yuan in Household Deposits Go?]](https://imgqn.smm.cn/usercenter/tgoYV20251217171715.jpg)