I. Why Has Aluminum Prices Kept Falling?

1. Reversal of Trading Expectations: From "General Supply Shortage" to "Structural Supply Shortage"

The fundamental driver behind the current aluminum price decline is a systemic shift in market pricing, moving from expectations of a general supply shortage to a structural supply shortage. Previously, market sentiment centered on supply disruptions stemming from Middle East conflicts. More than 2 million metric tons of aluminum capacity in Bahrain, the United Arab Emirates and Qatar were shut down, coupled with blockages in the Strait of Hormuz, leading the market to anticipate a severe global aluminum deficit.

However, on the physical market side, actual conditions have not validated the notion of a widespread shortage. Overseas available stocks have been continuously replenished by Chinese aluminum exports. Meanwhile, high aluminum prices have curbed operating rates among overseas fabricators, and pre-conflict inventories have also eased tightness. Initially, supply concerns were mainly reflected in the strong backwardation (cash premium) of LME aluminum ingots, which failed to drive a substantial rally in outright prices. As Chinese aluminum exports alleviated overseas supply strains, market fears over tight supplies faded, dragging aluminum prices lower.

Evidence 1: Robust Chinese Aluminum Exports – A Major Relief Valve for Overseas Supply Gaps According to data from the General Administration of Customs of China, China’s exports of unwrought aluminum and aluminum products reached 598,000 metric tons in April 2026, representing a year-on-year increase of 15.4% and hitting a 17-month high. Cumulative exports over the first four months stood at 2.053 million metric tons, up 8.9% year on year.

With LME aluminum prices trading at a substantial premium over Shanghai aluminum (the SHFE/LME price ratio fell to around 6.66), China’s export window opened wide. Sustained growth in Chinese aluminum shipments has made up for part of the overseas physical supply deficit.

Evidence 2: Accelerated Commissioning of Overseas Capacity – Gradual Release of New Supply New overseas aluminum capacity continues to ramp up. Several Indonesian producers have applied for LME brand registration, which will potentially boost deliverable stocks on the exchange. In addition, market sources indicate that while the restart of some Middle East smelters has lagged expectations, new overseas capacity is set to come online at a faster pace.

Improving marginal supply has further undermined the narrative of prolonged supply disruptions and put pressure on forward contracts.

2. Macroeconomic Headwinds: Heightened Rate Hike Expectations Weigh on Risk Assets

U.S. non-farm payrolls for May far exceeded market forecasts, triggering a sharp repricing of the Federal Reserve’s monetary policy outlook. Supported by rate hike bets, the U.S. dollar strengthened notably, creating downward pressure on dollar-denominated LME base metals.

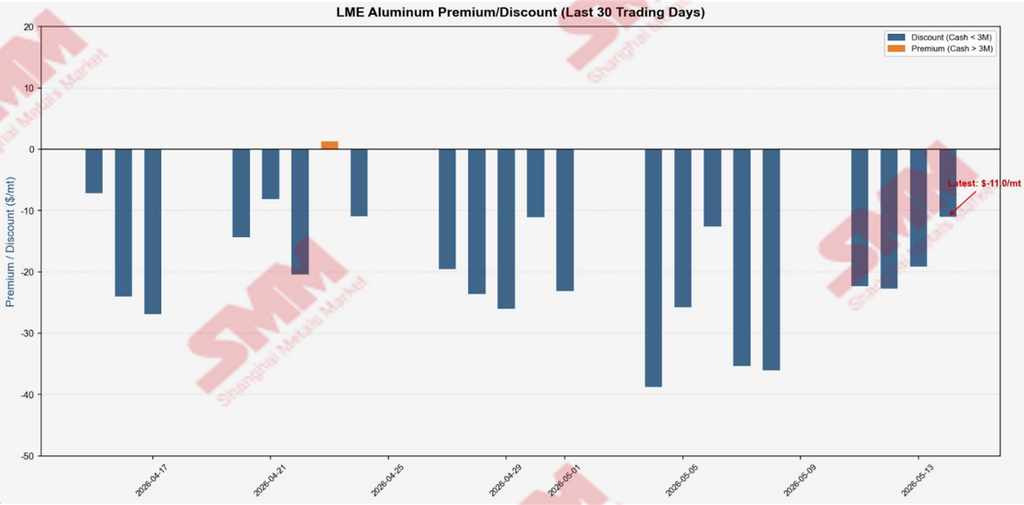

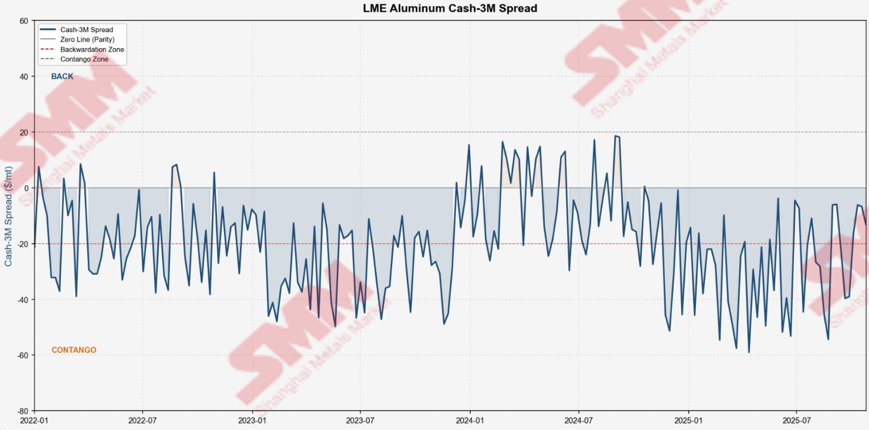

II. Why Did the Backwardation Structure Narrow Sharply?

From $104.56/MT to $15.17/MT: What Happened Within One Week?

Core View: The steep drop in LME Cash-3M premium from $104.56 per metric ton on June 1 to $15.17 per metric ton on June 9 resulted from the simultaneous impact of multiple factors: unwinding of overcrowded speculative long positions, surging Chinese aluminum exports easing physical shortages, and market repricing toward structural supply tightness. These factors combined to form a negative feedback loop across expectations, capital flows and physical markets.

May 28 – June 1: Backwardation Peaks as Geopolitical Premium Hits Extreme

The cash premium stood at $92.53/MT on May 28, jumped to $101.18/MT on May 29, and hit a recent peak of $104.56/MT on June 1. At this stage, the market priced in prolonged blockages in the Strait of Hormuz and an uncertain timeline for the resumption of Middle East capacity. Long positions became heavily concentrated, making aluminum the most crowded long trade among LME metals.

June 2: Turning Point – Geopolitical Premium Starts to Ease

The market began to unwind excessive geopolitical premiums built up earlier. Strong Chinese aluminum exports effectively relieved overseas physical demand, weakening the extreme pricing based on supply disruption fears. The geopolitical premium that had propelled aluminum prices higher started to recede, with the cash premium edging down slightly to $98.09/MT on the day.

June 3: Mass Liquidation of Speculative Longs – Premium Plunges by Nearly $30/MT in One Day

The cash premium tumbled from $98.09/MT to $68.22/MT, a single-day loss of almost $30 per metric ton. This marked a classic reversal of an overcrowded trade. As market sentiment shifted, massive accumulated speculative long positions were liquidated in a rush, triggering a long liquidation spiral. Although LME aluminum inventories continued to draw down (falling 250 metric tons to 335,200 metric tons), inventory declines could no longer sustain the strong cash premium.

June 4 – June 5: China’s Export Data Confirms Trend – Expectations of Physical Shortages Revised

The cash premium rebounded moderately to $72.21/MT on June 4 before falling again to $54.89/MT on June 5. The market digested the impact of China’s April aluminum export volume of 598,000 metric tons (up 15.4% year on year), acknowledging that Chinese exports have become a key source of additional supply for overseas markets. With the wide SHFE/LME price spread maintaining healthy export margins, the market reassessed the role of Chinese shipments in easing LME physical tightness.

June 8 – June 9: Accelerated Narrowing – Triple Factors Lead to a Near-Collapse of Backwardation

The cash premium dropped to $47.85/MT on June 8 and further slid to $15.17/MT on June 9, losing nearly $90 per metric ton within a week. Three major dynamics played out simultaneously:

- Market expectations shifted from a general supply shortage to a structural shortage. Sustained Chinese exports and accelerated overseas capacity rollout triggered a broad retreat of extreme bullish bets on supply disruptions.

- Panicked liquidation of speculative longs intensified the long-liquidation negative feedback.

- Rising inflation concerns and a stronger U.S. dollar dampened overall risk appetite.

III. Comprehensive Assessment & Outlook

Core View: LME aluminum prices are currently in a phase of receding geopolitical premiums and downward expectation revisions. The sharp narrowing of backwardation essentially reflects a market shift from panic-driven pricing back to rational valuation.

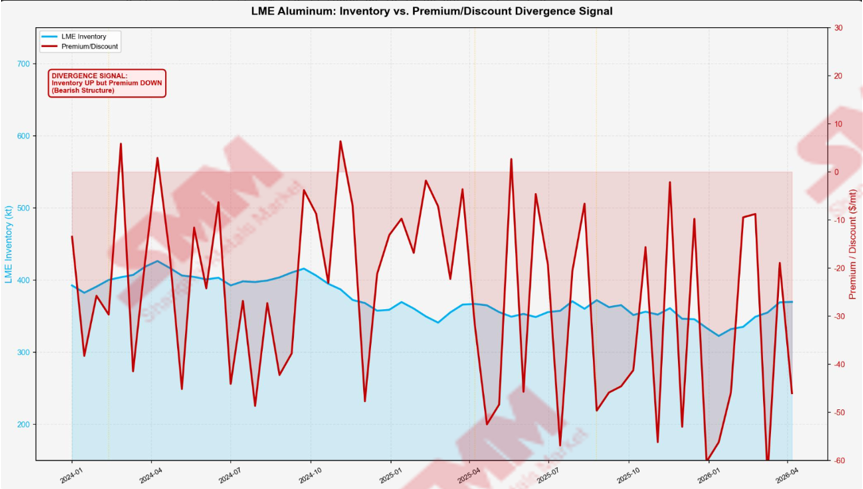

Nevertheless, LME aluminum inventories remain at a 20-year low. Physical supply tightness is still a fundamental reality, temporarily masked by revised expectations and increased Chinese exports. Four key variables will dictate future market moves:

- Developments in U.S.-Iran tensions, which will shape energy costs and inflation expectations.

- Sustainability of China’s aluminum exports, determining the extent of relief for overseas physical shortages.

- Actual progress of production restarts in the Middle East, which will define the pace of supply improvement for forward contracts.

- Commissioning progress of new overseas aluminum projects.

In the short term, aluminum prices will trend weakly with choppy fluctuations, yet downside potential is limited. Ultra-low inventories will act as a solid floor for prices.

![Rising Raw Material Costs Squeeze Profits, Aluminum Fluoride Market Stagnant with Stable Prices [SMM Fluoride Salt Weekly Review]](https://imgqn.smm.cn/usercenter/RLjGN20251217171652.jpg)

![Expectations for US Fed Interest Rate Hikes Game Persists, China’s Accelerating Destocking Signals Short-Term Stabilization [SMM Aluminum Weekly Review]](https://imgqn.smm.cn/usercenter/DRlGu20251217171652.jpg)