Introduction

For decades, aluminium scrap has been traded globally as a conventional recyclable commodity, with trade flows largely driven by price, logistics costs and regional supply-demand dynamics. However, as energy transition, low-carbon manufacturing and resource security become increasingly important, the strategic value of aluminium scrap is being reassessed worldwide.

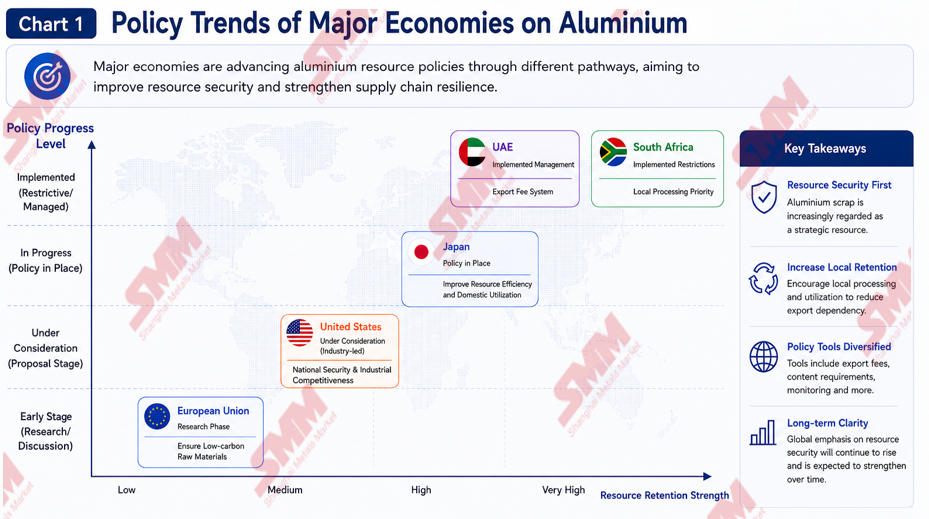

From the European Union's consideration of scrap export restrictions, to the U.S. aluminium industry's call to classify scrap as a strategic asset, Japan's efforts to strengthen circular economy systems, and the UAE's implementation of metal scrap export fees, major economies are gradually redefining the role of aluminium scrap within industrial supply chains.

For Asian markets that rely heavily on imported scrap to produce ADC12 and secondary aluminium alloys, this trend could become an important factor influencing future raw material availability and production costs.

Why Is Aluminium Scrap Becoming a Strategic Resource?

The growing importance of aluminium scrap is closely linked to global decarbonisation efforts. Compared with primary aluminium production, secondary aluminium typically requires only around 5% of the energy consumption while reducing carbon emissions by approximately 95%. As industries such as electric vehicles, power infrastructure, construction, packaging and advanced manufacturing pursue increasingly ambitious carbon reduction targets, recycled aluminium has become a critical pathway for industrial decarbonisation.

At the same time, geopolitical tensions, supply chain disruptions, energy market volatility and growing concerns over industrial resilience have prompted governments to reassess the security of critical raw material supplies. Aluminium scrap is therefore increasingly viewed not merely as a recyclable commodity, but as a strategic industrial input capable of supporting low-carbon manufacturing, supply chain security and long-term industrial competitiveness.

As governments place greater emphasis on strategic autonomy and resource resilience, global aluminium scrap trade is gradually shifting from a purely price-driven model towards one increasingly influenced by policy objectives and resource security considerations.

1. European Union: Defending Scrap Resources in the CBAM Era

The European Union is currently one of the most closely watched regions in the global aluminium scrap market.

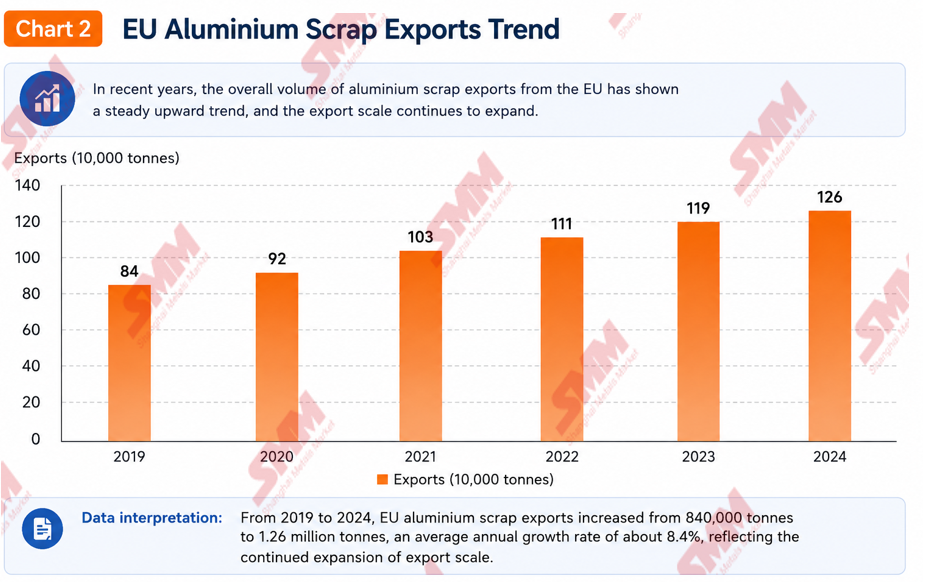

According to industry estimates, EU aluminium scrap exports increased from approximately 840,000 tonnes in 2019 to around 1.26 million tonnes in 2024, representing growth of nearly 50% within five years. A significant portion of this material has been shipped to destinations including India, Türkiye, Malaysia, Thailand and other Asian markets.

This trend has raised growing concerns among European aluminium producers. European Aluminium has argued that continued exports of high-quality scrap are weakening the competitiveness of Europe's domestic recycling industry. The association has pointed out that some European secondary aluminium production capacity remains underutilised despite large volumes of valuable scrap leaving the region.

The issue is closely linked to the EU's broader industrial and climate strategies. Initiatives such as the European Green Deal, the Net-Zero Industry Act and the Carbon Border Adjustment Mechanism (CBAM) have significantly increased the importance of low-carbon raw materials within Europe's manufacturing supply chains.

CBAM, which entered its transitional phase in 2023 and will enter its definitive phase in 2026, will require imported aluminium products to bear carbon-related costs based on their production emissions. Against this backdrop, recycled aluminium has gained strategic importance due to its significantly lower carbon footprint.

Compared with primary aluminium production, secondary aluminium requires only around 5% of the energy while reducing carbon emissions by approximately 95%. As a result, recycled aluminium is increasingly regarded as one of the most effective pathways for the aluminium industry's decarbonisation efforts.

For European manufacturers, increasing recycled content not only helps lower product carbon footprints but may also mitigate future CBAM-related costs. With industries such as electric vehicles, packaging, construction and renewable energy accelerating their low-carbon transition, aluminium scrap is gradually evolving from a conventional recyclable material into a strategic industrial resource.

Consequently, European Aluminium has advocated stronger measures to retain scrap resources within Europe. One of the most closely watched proposals is the association's recommendation for a 30% export duty on aluminium scrap. Supporters argue that higher export costs could increase domestic scrap availability and strengthen Europe's recycling industry.

Against this backdrop, the European Commission has launched targeted consultations on aluminium scrap exports and is assessing potential measures under the forthcoming REsourceEU Action Plan. Policy tools currently under discussion include export duties, export licensing systems, enhanced export monitoring mechanisms and higher recycled-content requirements.

However, these proposals have faced opposition from the recycling sector. In May 2026, Recycling Europe, together with the Bureau of International Recycling (BIR) and several other industry organisations, submitted a joint letter to the European Commission opposing export restrictions on aluminium scrap. These groups argue that Europe does not face a structural scrap shortage and warn that export controls could harm recyclers, reduce investment and weaken the circular economy.

While the final policy outcome remains uncertain, the EU's focus on increasing domestic utilisation of scrap resources is becoming increasingly clear.

2. United States: Aluminium Scrap Enters the National Security Framework

In the United States, discussions surrounding aluminium scrap have increasingly moved beyond recycling and entered the broader debate over manufacturing competitiveness, supply chain resilience and national security.

In 2025, The Aluminum Association released its white paper titled Scrap the Exports, Save U.S. Supply, describing aluminium scrap as a strategic asset. The report argues that retaining more scrap within the United States could strengthen domestic supply chains, reduce import dependence and support long-term industrial growth.

According to the association, approximately 85% of aluminium produced in the United States today is secondary aluminium derived from recycled scrap. Despite this heavy reliance on recycled material, the country continues to export approximately 2 million tonnes of aluminium scrap annually.

The association also estimates that the United States faces an annual primary aluminium supply gap of approximately 4 million tonnes. Against this backdrop, retaining more domestically generated scrap is increasingly viewed as a cost-effective way to strengthen supply chain security and reduce reliance on imported metal.

Industry groups argue that rising demand from electric vehicles, power infrastructure, data centres, aerospace and defence manufacturing will require greater access to domestic scrap resources. As a result, the association has called for priority retention of high-quality scrap streams such as used beverage cans (UBCs), mill-ready scrap and industrial scrap.

UBCs are considered one of the most valuable categories due to their role in closed-loop recycling systems, while mill-ready scrap can be directly fed into melting operations with minimal processing. Industrial scrap generated during manufacturing is also highly valued because of its consistent quality and composition.

By contrast, the association has adopted a more cautious position regarding lower-grade mixed scrap streams such as Zorba and Twitch, arguing that restrictions on these materials could create logistical bottlenecks and discourage investment in sorting and processing infrastructure.

Although no formal export restrictions have been introduced, the debate itself reflects a significant shift in policy thinking. Aluminium scrap is increasingly being viewed not only as a recyclable material but also as a strategic resource capable of supporting industrial competitiveness and national security objectives.

3. Japan: Strengthening Resource Security Through Circular Economy

Unlike the European Union and the United States, Japan is not currently considering export duties, export licensing systems or export bans for aluminium scrap. Instead, the country is focusing on strengthening resource security through circular economy development and greater utilisation of recycled materials.

As a resource-poor nation heavily dependent on imported raw materials, Japan has long regarded resource security as a key element of industrial policy. Global supply chain disruptions and rising geopolitical uncertainty have further reinforced this priority.

In 2026, Japan introduced a new Circular Economy Action Plan, targeting approximately ¥1 trillion in circular economy-related investment by 2030. The initiative aims to improve resource productivity, increase recycling rates and strengthen industrial resilience while reducing reliance on imported raw materials.

The Japanese aluminium industry is also promoting greater use of recycled and low-carbon aluminium. One of the most notable examples is the collaboration between Toyota and UACJ on closed-loop vehicle recycling systems, which recover aluminium from end-of-life vehicles and return it to automotive manufacturing.

At the same time, the Japan Aluminium Association has repeatedly highlighted the importance of green aluminium, recycling and resource efficiency in supporting the country's carbon neutrality objectives.

While Japan remains committed to free trade principles and is unlikely to introduce direct export restrictions in the near future, stronger domestic demand for recycled aluminium could gradually reduce export availability over time.

In this respect, Japan's influence on future aluminium scrap flows may come through increased domestic consumption rather than regulatory intervention.

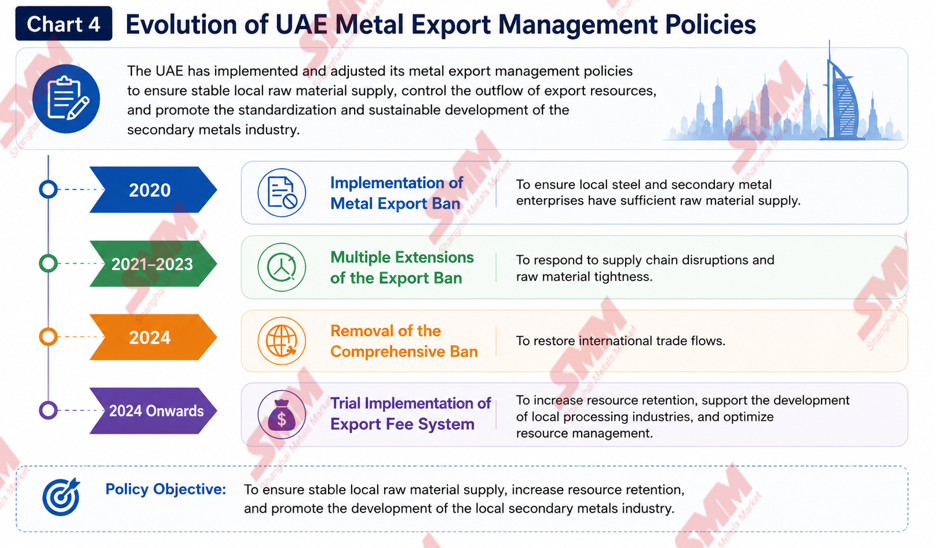

4. UAE: From Export Ban to Export Fee System

The UAE represents one of the most practical examples of resource retention policies already being implemented.

As a major regional trading hub for ferrous and non-ferrous scrap, the UAE introduced export restrictions on scrap metals during the pandemic period to support domestic manufacturers facing raw material shortages and supply chain disruptions.

Between 2020 and 2023, the country repeatedly extended scrap export restrictions to ensure sufficient feedstock availability for local industries. However, rather than maintaining a permanent export ban, the government later shifted towards a market-based approach.

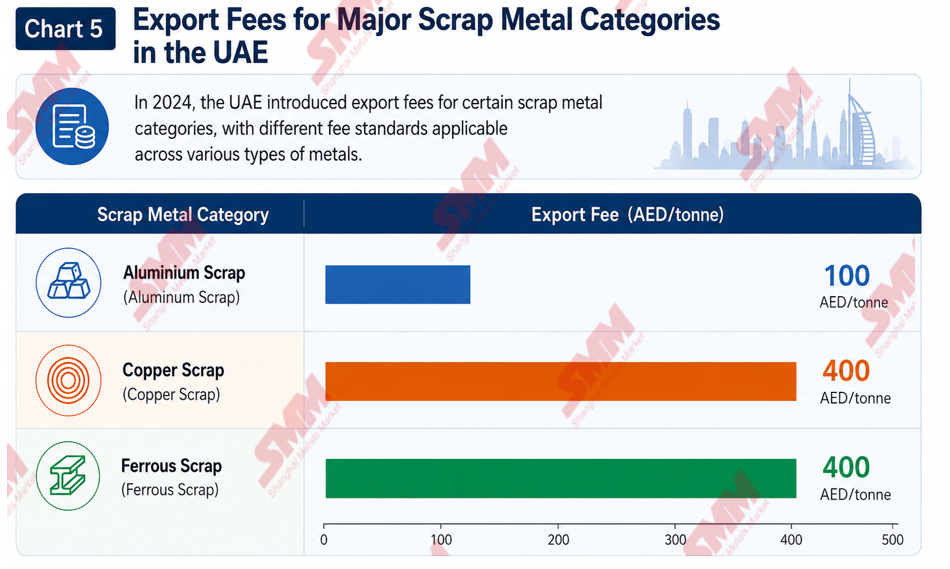

In 2024, the UAE officially replaced its export ban with an export fee system. Current fees include AED100 per tonne for aluminium scrap and AED400 per tonne for both copper and ferrous scrap.

Compared with a complete export ban, the fee system allows international trade to continue while encouraging more material to remain within the domestic market. The policy reflects a broader shift from administrative restrictions toward market-based resource management.

The UAE's approach seeks to balance resource security, industrial development and international trade. As demand for recycled metals continues to grow across construction, packaging, transportation and renewable energy sectors, scrap materials are increasingly viewed as strategic industrial resources rather than simple trading commodities.

The UAE's experience is increasingly viewed as a reference case for other countries exploring ways to retain valuable scrap resources without fully disrupting international trade flows.

5. South Africa: Prioritising Domestic Processing

South Africa provides another example of resource retention policies being implemented to support domestic industrial development.

In recent years, the country has strengthened controls on scrap metal exports and introduced measures aimed at prioritising local processing. In 2022, South Africa implemented a scrap metal export ban covering several categories of metal scrap.

The policy was designed to improve raw material availability for domestic manufacturers and support local value-added production. South African authorities have argued that exporting large volumes of scrap may generate short-term trade revenue but does little to support industrialisation and employment growth.

Unlike the European Union's focus on decarbonisation or the United States' emphasis on supply chain security, South Africa's policy is largely centred on industrial development, value addition and job creation.

The country's experience demonstrates that resource retention policies are not limited to developed economies. Increasingly, emerging markets are also seeking to retain more recyclable resources within their domestic industrial ecosystems.

SMM View

Although the policy approaches adopted by the EU, the United States, Japan, the UAE and South Africa differ significantly, they all point toward the same underlying trend: aluminium scrap is increasingly being recognised as a strategic resource rather than merely a recyclable commodity.

At present, most of these measures are unlikely to trigger an immediate disruption to global trade flows. However, the direction of travel is becoming increasingly clear. Governments and industry organisations are placing greater emphasis on domestic resource utilisation, supply chain resilience and low-carbon industrial development.

For market participants, the key question is not whether policies are changing, but whether those policies will ultimately alter resource flows. If more high-quality scrap remains within producing regions such as Europe and North America, competition for premium scrap grades could intensify across international markets.

This trend is particularly relevant for ADC12 producers and secondary aluminium smelters that rely on imported raw materials. In the coming years, monitoring policy developments may become just as important as tracking aluminium prices, freight rates or exchange rates.

Ultimately, the global aluminium scrap market is entering a new phase in which price, policy and resource security are becoming increasingly interconnected. In such an environment, access to stable scrap supply chains may prove to be one of the most important competitive advantages for secondary aluminium producers.