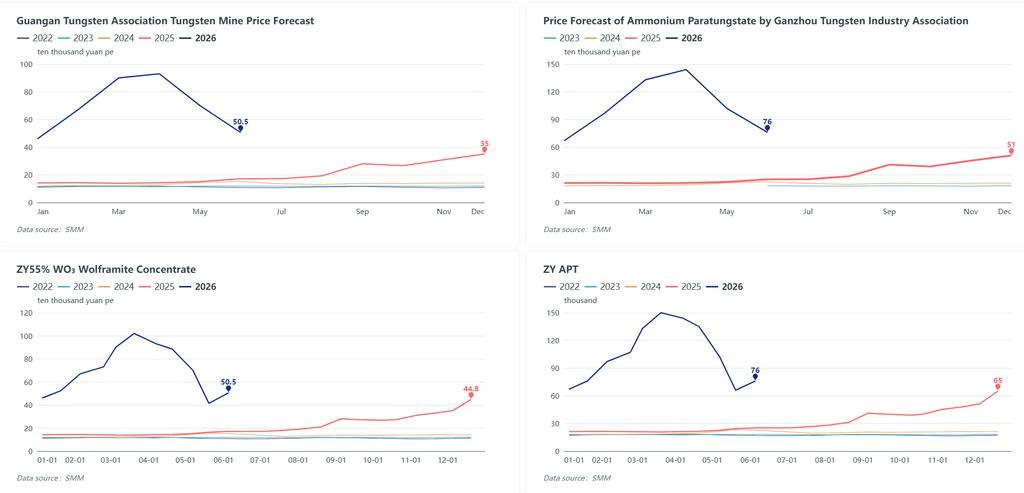

SMM Report, June 5: Benchmark monthly long-term contract prices for China’s tungsten sector were officially released recently. The Ganzhou Tungsten Association unveiled its June 2026 domestic tungsten forecast prices: 55% WO₃ black tungsten concentrate at RMB 505,000 per metric ton, down RMB 195,000/MT month-on-month; ammonium paratungstate (APT) priced at RMB 760,000 per metric ton, a MoM drop of RMB 260,000/MT; medium-sized tungsten powder quoted at RMB 1,300 per kilogram, falling RMB 620/kg from May. Shortly afterwards, a leading major tungsten producer based in Zhangyuan published its first-half June long-term settlement prices: 55% black tungsten concentrate settled at RMB 505,000/MT and 55% white tungsten concentrate at RMB 504,000/MT, representing a rise of RMB 91,000/MT versus late-May levels. APT long-term price was fixed at RMB 760,000/MT, up RMB 100,000/MT compared with late-May. All aforementioned prices include 13% VAT. Published long-term prices are largely in line with mainstream spot market transactions, while listed tungsten powder quotations stand slightly above prevailing spot market levels, effectively lifting market bullish sentiment.

Tungsten Concentrate Sector

As of Friday’s close, SMM spot assessment for 55% black tungsten concentrate settled at RMB 495,500 per metric ton, climbing RMB 30,000/MT from the previous trading session and accumulating a monthly gain of RMB 74,000/MT. The concentrate benchmark has registered eight consecutive trading days of gains, with an overall rebound of RMB 100,000/MT during this rally cycle. Mines across Southwest China have gradually released spot cargoes recently; with current profit margins restored, mine operators opt to liquidate partial inventories and realize earnings amid improved downstream demand, boosting market spot liquidity and easing enterprises’ capital pressure. Market participants will keep a close eye on upcoming mine tender results as well as downstream purchasing appetite next week.

APT Sector

SMM spot APT closed at RMB 760,000 per metric ton on Friday, up RMB 10,000/MT day-on-day with a total rebound of RMB 130,000/MT so far. Domestic APT manufacturers hold robust bullish expectations and carry high-cost raw material inventories, leaving most producers reluctant to cut prices for cargo disposal and tightening available spot supply. Certain small-batch spot APT has been concluded above RMB 800,000/MT. Next week’s small-lot trading is expected to be negotiated based on confirmed long-term contract benchmarks. Downstream tungsten powder mills maintain steady purchasing willingness, forming solid fundamental support for APT prices. Nevertheless, subdued off-take volumes during April and May left some producers with leftover stockpiles, raising risks of concentrated inventory dumping down the line, which needs ongoing tracking.

Overseas Market

Weekly APT CIF Rotterdam assessment stabilized at USD 3,000–3,200 per metric ton unit, edging up USD 50 from last week despite muted concluded volumes. China’s domestic tungsten price rebound boosted European market sentiment, prompting holders to firmly defend asking prices and limiting availability of cheap cargoes, pointing to sideways consolidation for near-term overseas quotations. FOB India scrap tungsten drill bits were marked at USD 110–120/kg, rising 9.52% week-on-week on improved trader optimism driven by China’s price uptick. Persistent price premium of European APT over domestic Chinese levels keeps import costs elevated and restricts inbound tungsten concentrate arrivals, providing bottom-line support for domestic spot prices. Additionally, China’s price bottoming-out and rebound has spurred overseas end-users’ procurement interest in Chinese upstream tungsten raw materials and intermediate products; local exporters reported notable pick-ups in inbound inquiries and fresh export orders for tungsten powder, ammonium metatungstate and other fabricated tungsten grades.

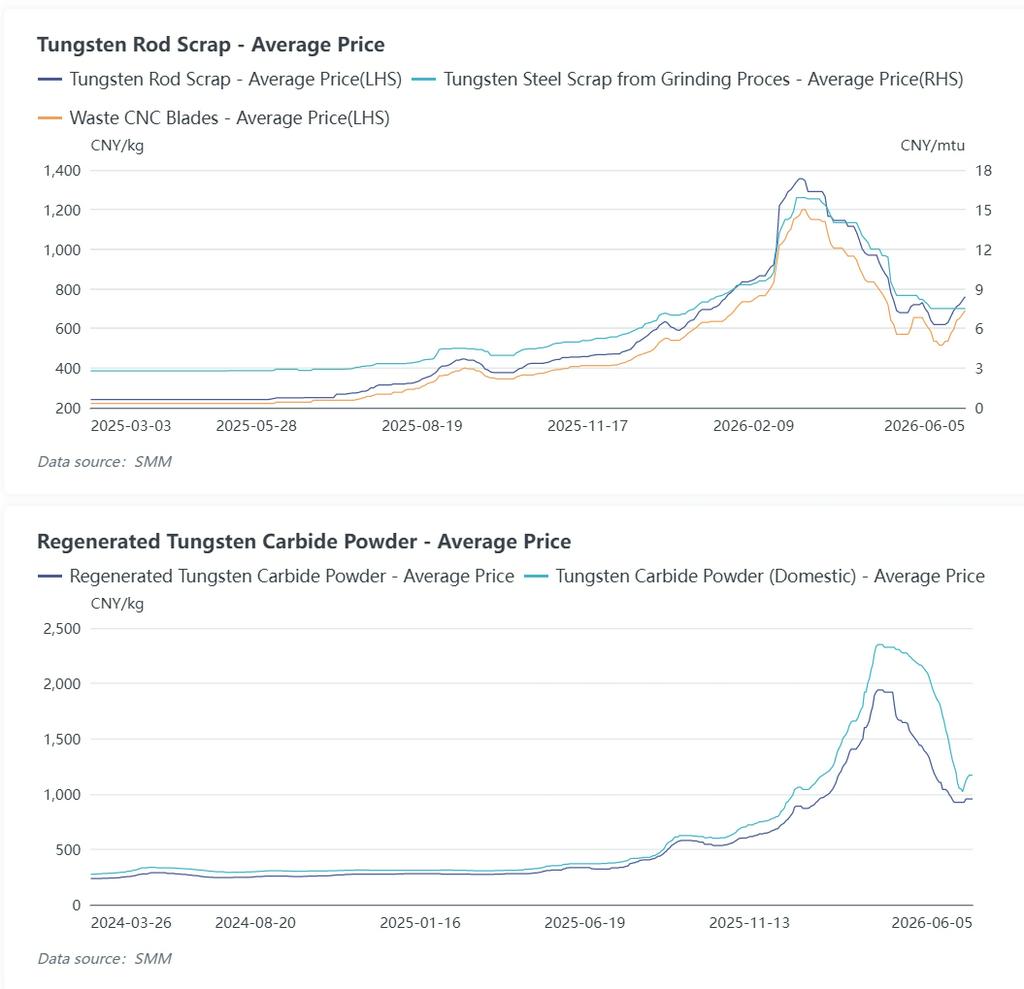

Scrap Tungsten Market

Domestic scrap tungsten prices trended higher alongside rising primary tungsten feedstock this week. Driven by upward movements of tungsten concentrate and APT, scrap collectors hold cargoes back and lift asking prices, tightening availability of used tungsten drill bits, tungsten bars and cemented carbide scrap. Recyclers refrain from bargain sales amid limited cheap spot supply, while secondary smelters gradually raise buying prices amid climbing raw material costs to cover regular production needs. That said, small-to-medium scrap merchants stay cautious on fresh high-priced purchases due to depleted low-cost historic inventories and scaled back speculative restocking activities, narrowing the price gap between scrap and virgin tungsten feedstock. Spot trades are mostly limited to genuine end-user demand. Near-term scrap prices are underpinned by firm primary tungsten quotations. However, smelters in key producing hubs including Jiangxi and Hunan have halted purchases of undocumented scrap resources, diverting bulk scrap volumes to intermediate traders instead of formal downstream production links and building up latent risks of concentrated sell-offs, which may trigger divergent price performance versus primary tungsten in due course.

Market Outlook

In the short run, the whole industrial chain presents a differentiated pattern: upstream mines restrict large-scale cargo release and defend spot prices, APT smelters resist price cuts, while downstream buyers only cover rigid production needs. Upward momentum for raw material prices remains intact, yet weak downstream acceptance will cap further sharp gains. Next week’s market direction will hinge on cargo volumes from mine auctions and sustained buying activity from cemented carbide manufacturers, with tungsten prices projected to fluctuate with a firm bias. Over the medium-to-long term, after over 70 days of cyclic market movement, downstream smelters and carbide producers have largely depleted low-cost raw material stockpiles, shifting the whole industry towards low inventory levels and paving the way for potential restocking demand alongside gradual recovery of end-user manufacturing activity. Still, rapid excessive price spikes would inflate carbide production costs drastically, squeeze downstream manufacturers’ profit margins and curb raw material procurement and production schedules, in turn dragging upstream demand. Gradual and moderate price appreciation that balances interests across the industrial chain is conducive to sustainable industrial development, securing reasonable earnings for miners while preserving profitability of midstream and downstream fabricators.