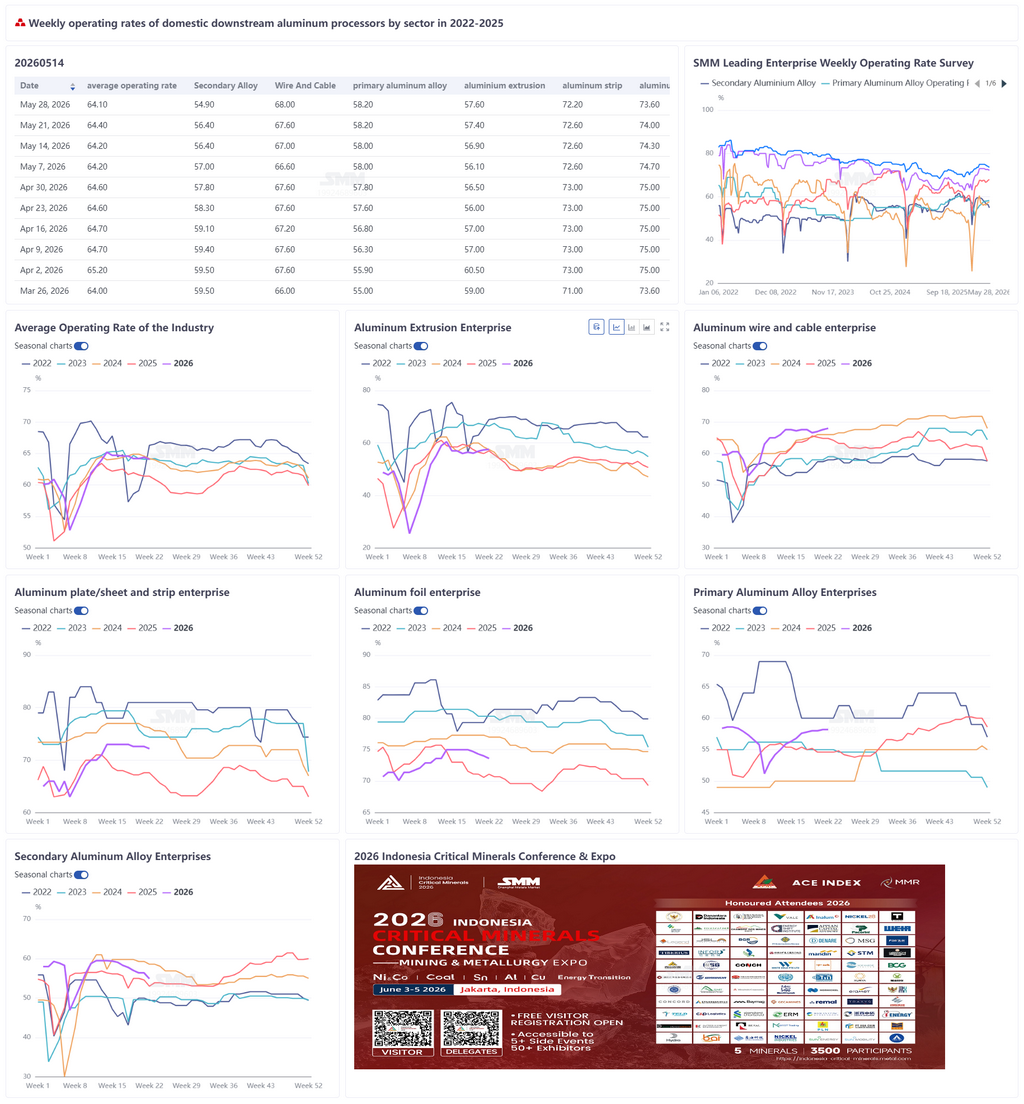

28 พฤษภาคม 2569:

สัปดาห์นี้ อัตราการเดินเครื่องของผู้ประกอบการแปรรูปอะลูมิเนียมขั้นปลายน้ำรายใหญ่ของจีนอยู่ที่ 64.1% ลดลง 0.3 จุดเปอร์เซ็นต์เมื่อเทียบรายสัปดาห์ ภาพรวมอุตสาหกรรมแสดงแนวโน้มฟื้นตัวอย่างอ่อนแอ แต่ยังคงมีความแตกต่างเชิงโครงสร้างอย่างมีนัยสำคัญภายใน อัตราการเดินเครื่องสายไฟและสายเคเบิลอะลูมิเนียมเพิ่มขึ้น 0.4 จุดเปอร์เซ็นต์เมื่อเทียบรายสัปดาห์มาอยู่ที่ 68.0% ได้แรงหนุนจากคำสั่งซื้อส่งออกที่เติบโตแข็งแกร่งและการสนับสนุนจากโครงการระบบสายส่งไฟฟ้า อัตราการเดินเครื่องแผ่นและแถบอะลูมิเนียมลดลง 0.4 จุดเปอร์เซ็นต์มาอยู่ที่ 72.6% แม้ราคาอะลูมิเนียมที่สูงจะกดดันการรับสินค้าของปลายน้ำ แต่ความต้องการเปลือกแบตเตอรี่และวัสดุบัดกรีในภาคระบบกักเก็บพลังงาน (ESS) ประกอบกับคำสั่งซื้อส่งออกรถยนต์พลังงานใหม่ที่เติบโตแข็งแกร่ง ช่วยพยุงชดเชยความต้องการแผ่นมาตรฐานที่อ่อนแอ อัตราการเดินเครื่องอะลูมิเนียมอัลลอยขั้นต้นทรงตัวที่ 58.2% ได้แรงหนุนจากการส่งออกที่ยืดหยุ่น โดยอุปสงค์ในประเทศมีเสถียรภาพ การปรับตัวลงของราคาอะลูมิเนียมกระตุ้นให้ปลายน้ำสอบถามเพิ่มขึ้น แต่การแปลงเป็นคำสั่งซื้อยังจำกัด อัตราการเดินเครื่องอะลูมิเนียมรีดขึ้นรูปเพิ่มขึ้นเล็กน้อย 0.2 จุดเปอร์เซ็นต์มาอยู่ที่ 57.6% เนื่องจากฤดูก่อสร้างสูงสุดในภาคเหนือของจีนและการส่งมอบคำสั่งซื้อกรอบแผงโซลาร์เซลล์ช่วยหนุนการฟื้นตัวของอะลูมิเนียมรีดขึ้นรูปสำหรับก่อสร้างและอุตสาหกรรม แม้การฟื้นตัวของภาคอสังหาริมทรัพย์ที่อ่อนแอยังคงเป็นปัจจัยกดดัน อัตราการเดินเครื่องอะลูมิเนียมฟอยล์ลดลง 0.4 จุดเปอร์เซ็นต์มาอยู่ที่ 73.6% ความต้องการฟอยล์แบตเตอรี่ ESS เฟื่องฟู ขณะที่ผลผลิตฟอยล์เครื่องปรับอากาศถูกฉุดรั้งจากอุปสงค์ในประเทศที่อ่อนแอและสินค้าคงคลังสูง อัตราการเดินเครื่องของผู้ผลิตอะลูมิเนียมทุติยภูมิลดลงอย่างมาก 1.5 จุดเปอร์เซ็นต์มาอยู่ที่ 54.9% เนื่องจากปัญหาขาดแคลนวัตถุดิบและแรงกดดันด้านต้นทุนยังคงมีอยู่ ซ้ำเติมด้วยอุปสงค์ที่อ่อนแอ บีบให้ผู้ประกอบการต้องลดกำลังการผลิต ปัจจุบัน อุตสาหกรรมแปรรูปอะลูมิเนียมโดยรวมพึ่งพาความยืดหยุ่นของการส่งออก การเติบโตที่แข็งแกร่งของ ESS และคำสั่งซื้อโครงสร้างพื้นฐานเพื่อชดเชยอุปสงค์ในประเทศที่อ่อนแอ ในระยะข้างหน้า ควรจับตาความยั่งยืนของอุปสงค์นอกจีน ผลกระทบของแนวโน้มราคาอะลูมิเนียมต่อความเต็มใจในการซื้อ และโมเมนตัมการฟื้นตัวในภาคดั้งเดิม

อะลูมิเนียมอัลลอยขั้นต้น: สัปดาห์นี้ อัตราการเดินเครื่องของผู้ประกอบการอะลูมิเนียมอัลลอยขั้นต้นรายใหญ่ของจีนทรงตัวเมื่อเทียบรายสัปดาห์ที่ 58.2% ด้านอุปทาน ผู้ประกอบการโดยรวมยังคงผลิตตามสัญญาระยะยาวตามปกติ โดยไม่มีการปรับแผนการผลิตอย่างมีนัยสำคัญ รักษาการดำเนินงานที่มีเสถียรภาพอุปสงค์แสดงการเปลี่ยนแปลงเชิงโครงสร้าง ประการแรก ด้านการส่งออกยังคงมีผลงานดี โดยข้อมูลการส่งออกล้ออะลูมิเนียมเดือนเมษายนเพิ่มขึ้น 19.43% เมื่อเทียบรายเดือน และเพิ่มขึ้น 12.71% เมื่อเทียบรายปี การฟื้นตัวของคำสั่งซื้อส่งออกให้การสนับสนุนอุปสงค์อะลูมิเนียมอัลลอยในระดับหนึ่ง ประการที่สอง อุปสงค์ตลาดจีนยังคงมีเสถียรภาพโดยรวม โดยยังไม่มีปัจจัยขับเคลื่อนการเติบโตที่ชัดเจน ที่น่าสังเกตคือ ราคาอะลูมิเนียมปรับตัวลงเมื่อเร็วๆ นี้ และผู้ประกอบการปลายน้ำบางรายเริ่มสอบถามราคาและเสนอราคาอย่างแข็งขัน ความเต็มใจในการซื้อปรับตัวดีขึ้นเล็กน้อยเมื่อเทียบกับช่วงก่อนหน้า อย่างไรก็ตาม เนื่องจากการส่งผ่านราคาและการดำเนินการตามคำสั่งซื้อยังต้องใช้เวลา ปริมาณธุรกรรมที่เพิ่มขึ้นจริงในสัปดาห์นี้ยังมีจำกัด และไม่ได้ส่งผลกระทบอย่างมีนัยสำคัญต่ออัตราการเดินเครื่องในปัจจุบัน โดยรวมแล้ว อุตสาหกรรมอะลูมิเนียมอัลลอยขั้นต้นกำลังดำเนินงานอย่างมีเสถียรภาพ โดยอัตราการเดินเครื่องคงอยู่ที่ 58.2% ติดต่อกันสองสัปดาห์ เมื่อพิจารณาผลกระทบกระตุ้นจากการปรับตัวลงของราคาอะลูมิเนียมต่อความเต็มใจในการซื้อของปลายน้ำ และกิจกรรมการสอบถามที่เพิ่มขึ้นทีละน้อย คาดว่าอัตราการเดินเครื่องของอุตสาหกรรมจะปรับตัวเพิ่มขึ้นเล็กน้อยในสัปดาห์หน้า

แผ่นอะลูมิเนียมและแถบอะลูมิเนียม: สัปดาห์นี้ อัตราการเดินเครื่องของผู้ประกอบการแผ่นอะลูมิเนียมและแถบอะลูมิเนียมชั้นนำลดลง 0.4 จุดร้อยละเมื่อเทียบรายสัปดาห์ มาอยู่ที่ 72.2% ในระดับการดำเนินงานของผู้ประกอบการ ผู้ประกอบการแผ่นอะลูมิเนียมชั้นนำบางรายถูกกดดันจากราคาอะลูมิเนียมที่สูงและบรรยากาศรอดูของปลายน้ำที่แผ่ขยาย ราคาอะลูมิเนียมแท่งเฉลี่ยเดือนพฤษภาคมยังคงอยู่ในระดับสูงราว 24,300 หยวน/ตัน โดยลูกค้าปลายทางกลัวราคาลดลงมากขึ้นและโดยทั่วไปใช้รูปแบบ "ซื้อปริมาณน้อยตามความต้องการ คิดราคารายวัน" ทำให้เกิดการหยุดชะงักเป็นระยะต่อจังหวะการส่งสินค้าของผู้ประกอบการแปรรูป แยกตามผลิตภัณฑ์ คำสั่งซื้อสต็อกกระป๋องในประเทศและอุปสงค์แข็งอื่นๆ ยังคงมีเสถียรภาพ ขณะที่ภาคระบบกักเก็บพลังงานแสดงอุปสงค์ที่แข็งแกร่งสำหรับเปลือกแบตเตอรี่ วัสดุบัดกรี และผลิตภัณฑ์ที่เกี่ยวข้อง โดยผู้ประกอบการที่เกี่ยวข้องเร่งตารางการผลิตเพื่อให้ส่งมอบทัน ซึ่งเป็นแรงสนับสนุนพื้นฐานสำหรับอัตราการเดินเครื่อง คำสั่งซื้อแผ่นอะลูมิเนียมสำหรับยานยนต์ได้รับประโยชน์จากการเติบโตเมื่อเทียบรายปีของการผลิตและยอดขายรถยนต์พลังงานใหม่ในประเทศ และการเติบโตของการส่งออกที่ยังคงแข็งแกร่ง อยู่ในช่วงฟื้นตัว ด้านการส่งออก ภายใต้บริบทการขาดดุลอุปทานอะลูมิเนียมทั่วโลก คำสั่งซื้อส่งออกแผ่นอะลูมิเนียมมีผลงานแข็งแกร่ง โดยคำสั่งซื้อส่งออกของผู้ประกอบการจองเต็มถึงปลายเดือนกรกฎาคมมองไปข้างหน้าในเดือนมิถุนายน ราคาอะลูมิเนียมที่สูงจะยังคงครองจังหวะตลาด เนื่องจากคำสั่งซื้อแผ่นมาตรฐานในประเทศถูกกดดัน อัตราการเดินเครื่องคาดว่าจะรักษาแนวโน้มทรงตัวถึงอ่อนตัว

สายไฟและสายเคเบิลอะลูมิเนียม: สัปดาห์นี้ อัตราการเดินเครื่องของอุตสาหกรรมสายไฟและสายเคเบิลอะลูมิเนียมของจีนอยู่ที่ 68.0% เพิ่มขึ้น 0.4 จุดเปอร์เซ็นต์เมื่อเทียบรายสัปดาห์ อัตราการเดินเครื่องของอุตสาหกรรมแข็งแกร่งขึ้นอีกครั้งในสัปดาห์นี้ โดยมีแรงขับเคลื่อนหลักจากปริมาณคำสั่งซื้อส่งออกสายอะลูมิเนียมที่เติบโตต่อเนื่อง ปริมาณการจัดซื้อและการส่งมอบของอุตสาหกรรมยังคงเติบโตเป็นบวก ผู้ประกอบการรายงานว่าตารางการผลิตคำสั่งซื้อส่งออกสายอะลูมิเนียมตีเกลียวครอบคลุมคำสั่งซื้อครึ่งเดือนถึงสองเดือนแล้ว ผลักดันให้อัตราการเดินเครื่องแข็งแกร่งต่อเนื่องในระยะสั้น ด้านอุปสงค์ ผู้ค้ารายงานว่าเนื่องจากราคาอะลูมิเนียมสปอตนอกจีนยังคงปรับตัวสูงขึ้น จึงได้รับคำสั่งซื้อจำนวนมากจากเอเชียตะวันออกเฉียงใต้ ซึ่งกำลังถูกส่งต่อไปยังผู้ผลิตในประเทศทีละน้อย ด้วยการสนับสนุนจากคำสั่งซื้อส่งออกปัจจุบัน ประกอบกับผู้ผลิตดำเนินการผลิตคำสั่งซื้อโครงการระบบสายส่งไฟฟ้าในประเทศตามแผน การส่งมอบของอุตสาหกรรมยังคงแสดงแนวโน้มเติบโต อัตราการเดินเครื่องของอุตสาหกรรมสายอะลูมิเนียมของจีนคาดว่าจะยังคงแข็งแกร่งในระยะสั้น

อะลูมิเนียมอัดรีด: สัปดาห์นี้ อัตราการเดินเครื่องของอุตสาหกรรมอะลูมิเนียมอัดรีดของจีนอยู่ที่ 57.6% เพิ่มขึ้น 0.2 จุดเปอร์เซ็นต์เมื่อเทียบรายสัปดาห์ โดยอุตสาหกรรมยังคงมีแนวโน้มฟื้นตัวอย่างค่อยเป็นค่อยไป สำหรับอะลูมิเนียมอัดรีดก่อสร้าง ผู้ประกอบการบางรายจัดการผลิตตามคำสั่งซื้อโครงการวิศวกรรมขนาดใหญ่ที่มีอยู่ในมือ ให้การสนับสนุนการดำเนินงานโดยรวม ผู้ประกอบการในภูมิภาคซานตงรายงานว่าอุณหภูมิปรับตัวสูงขึ้นอย่างต่อเนื่องเมื่อเร็วๆ นี้ และภาคเหนือของจีนเข้าสู่ช่วงฤดูก่อสร้าง กระตุ้นอุปสงค์ปลายทางสำหรับการตกแต่งบ้านและเปลี่ยนหน้าต่าง/ประตู สำหรับอะลูมิเนียมอัดรีดอุตสาหกรรม การอ่อนตัวเป็นช่วงๆ ของราคาอะลูมิเนียมเมื่อเร็วๆ นี้ เพิ่มความเต็มใจในการซื้อของปลายน้ำ ผลักดันการเติบโตของคำสั่งซื้อและกระตุ้นการดำเนินงาน นอกจากนี้ ผู้ประกอบการกรอบแผงโซลาร์เซลล์ในเหอเป่ยรายงานว่าคำสั่งซื้อส่งมอบมาถึงในต้นเดือนมิถุนายน โดยตารางการผลิตที่เพิ่มขึ้นในสัปดาห์นี้ผลักดันการดำเนินงานให้สูงขึ้น โดยรวมแล้ว แม้การฟื้นตัวของตลาดอสังหาริมทรัพย์ยังคงอ่อนแอ แต่คำสั่งซื้อโครงการวิศวกรรมขนาดใหญ่ที่มีอยู่ในมือมีข้อได้เปรียบด้านปริมาณและรอบการส่งมอบที่ยาวนานกว่า ให้การสนับสนุนที่มั่นคงสำหรับการดำเนินงานในระยะใกล้ ประกอบกับอุณหภูมิที่สูงขึ้นกระตุ้นการบริโภคหน้าต่างและประตูสำหรับตกแต่งบ้าน การดำเนินงานอะลูมิเนียมอัดรีดก่อสร้างจะยังคงฟื้นตัวต่อเนื่องปัจจัยพื้นฐานของอุตสาหกรรมอะลูมิเนียมอัดรีดยังคงแข็งแกร่ง โดยมีอุปสงค์คงที่จากภาคการผลิตปลายน้ำ แต่ควรระมัดระวังความผันผวนของราคาอะลูมิเนียมในระยะถัดไปที่อาจกดดันความต้องการซื้อของปลายน้ำ คาดว่าอัตราการดำเนินงานอะลูมิเนียมอัดรีดจะยังคงปรับตัวขึ้นในสัปดาห์หน้า

อะลูมิเนียมฟอยล์: สัปดาห์นี้ อัตราการดำเนินงานของผู้ผลิตอะลูมิเนียมฟอยล์รายใหญ่ปรับลดลง 0.4 จุดเปอร์เซ็นต์ เมื่อเทียบรายสัปดาห์ มาอยู่ที่ 73.6% ในแง่โครงสร้างคำสั่งซื้อ อุปสงค์ปลายทางระบบกักเก็บพลังงาน (ESS) ยังคงร้อนแรง โดยการผลิตแบตเตอรี่เดือนพฤษภาคมเกิน 80 GWh และคำสั่งซื้อของผู้ผลิตชั้นนำถูกจองเต็มถึงไตรมาส 3 และหลังจากนั้น ให้การสนับสนุนที่แข็งแกร่งแก่ฟอยล์แบตเตอรี่ เนื่องจากสายการผลิตฟอยล์ดับเบิลซีโร่ถูกเปลี่ยนมาผลิตฟอยล์แบตเตอรี่ตามลำดับ อุปทานฟอยล์บรรจุภัณฑ์ในตลาดจึงหดตัวอย่างเห็นได้ชัด ภายใต้บริบทที่อุปทานผลิตภัณฑ์กึ่งสำเร็จรูปอะลูมิเนียมทั่วโลกตึงตัว คำสั่งซื้อส่งออกที่เพิ่มขึ้นยิ่งหนุนความเฟื่องฟูของฟอยล์บรรจุภัณฑ์ อย่างไรก็ตาม กลุ่มฟอยล์เครื่องปรับอากาศกลายเป็นปัจจัยฉุดหลัก: แผนการผลิตเพื่อจำหน่ายในประเทศของเครื่องปรับอากาศในครัวเรือนเดือนมิถุนายนลดลงอย่างมากเมื่อเทียบรายปี และภายใต้แรงกดดันจากสินค้าคงคลังสูงและต้นทุนสูง ผู้ประกอบการระมัดระวังอย่างยิ่งต่อแผนการผลิต คาดว่าแผนการผลิตฟอยล์เครื่องปรับอากาศจะลดลงต่อไป มองไปข้างหน้าในเดือนมิถุนายน อุปสงค์ ESS และบรรจุภัณฑ์จะยังคงเป็นฐานรองรับอัตราการดำเนินงาน แต่แนวโน้มขาลงที่ชัดเจนของคำสั่งซื้อฟอยล์เครื่องปรับอากาศในประเทศจะยังคงฉุดผลผลิตรวมของอุตสาหกรรม ส่งผลให้ศูนย์กลางอัตราการดำเนินงานอะลูมิเนียมฟอยล์โดยรวมยังคงเลื่อนลงต่อในเดือนมิถุนายน

อะลูมิเนียมทุติยภูมิ: สัปดาห์นี้ อัตราการดำเนินงานของผู้ผลิตอะลูมิเนียมทุติยภูมิรายใหญ่ลดลง 1.5 จุดเปอร์เซ็นต์ เมื่อเทียบรายสัปดาห์ มาอยู่ที่ 54.9% โดยการลดกำลังการผลิตแพร่กระจายทั่วทั้งอุตสาหกรรม เนื่องจากอุปทานวัตถุดิบที่ถูกต้องตามกฎหมายยังคงตึงตัว และแรงกดดันด้านต้นทุนยากที่จะส่งผ่านไปยังปลายน้ำ ผู้ประกอบการจึงลดภาระการผลิตทั้งแบบเชิงรุกและเชิงรับ สินค้าคงคลังวัตถุดิบของผู้ประกอบการยังคงถูกใช้ไป โดยปริมาณการเติมสต็อกใหม่มีจำกัด และความคาดหวังการหดตัวของอุปทานทวีความรุนแรงขึ้นตามไปด้วย ความกังวลของตลาดเกี่ยวกับแหล่งอุปทานในอนาคตที่ตึงตัวเพิ่มขึ้น โดยแหล่งราคาต่ำลดลงอย่างเห็นได้ชัด ด้านอุปสงค์ยังคงอ่อนแอ คำสั่งซื้อจากปลายน้ำตามมาอย่างซบเซา ธุรกรรมโดยรวมเงียบเหงา และการจัดซื้อมุ่งเน้นเฉพาะการเติมสต็อกตามความจำเป็น อุปสงค์ที่อ่อนแอยิ่งฉุดการดำเนินงานลง ในระยะสั้น ภายใต้แรงกดดันสองทางจากต้นทุนสูงและอุปสงค์อ่อนแอ อัตราการดำเนินงานของผู้ผลิตอะลูมิเนียมทุติยภูมิยังคงมีแนวโน้มลดลง