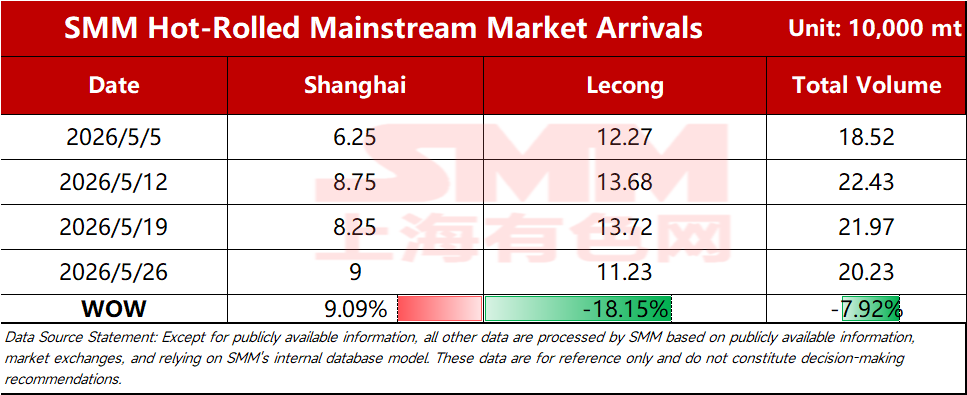

SMM Steel News, May 26: According to SMM statistics, estimated total shipments from mainstream markets this week were 202,300 mt, down 7.92% WoW. By market:

Table 1: Mainstream Market Arrivals Comparison

Source: SMM Steel

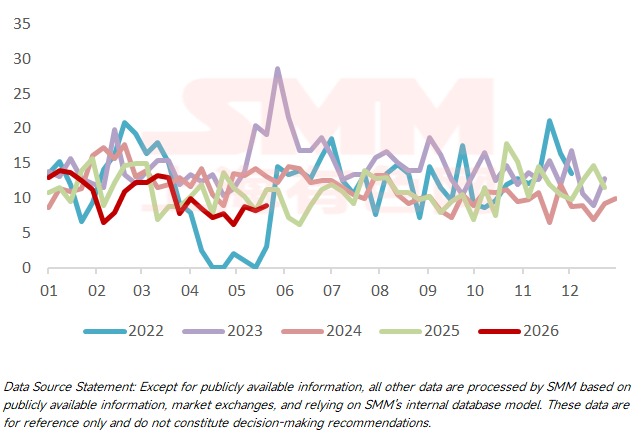

Shanghai market: HRC shipments in the Shanghai market showed relatively small fluctuations WoW. Specifically, shipments from northeast steel mills decreased somewhat, shipments from north China and east China steel mills remained stable, and shipments from mainstream steel mills in south China edged up slightly. Looking ahead to next week, considering that shipments from mainstream steel mills in south China to the east China market have remained at relatively low levels recently, coupled with weakening HRC prices and lackluster market transactions, arrivals in the Shanghai market are expected to continue at low levels next week.

Chart-1: Shanghai Market Arrivals

Source: SMM Steel

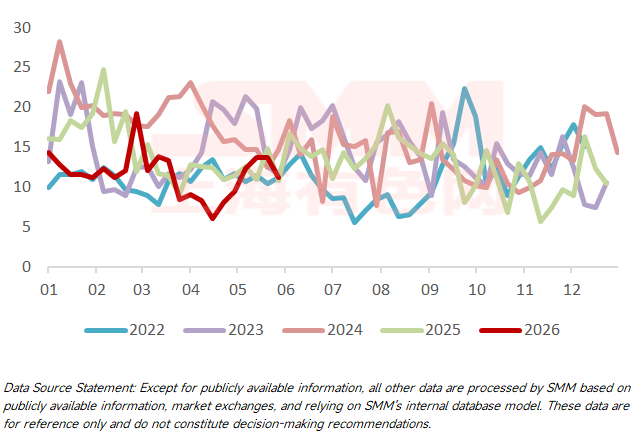

Lecong market: Shipments destined for Lecong pulled back WoW. Specifically, north China resources edged up slightly WoW, while a mainstream resource that had shipped more in the prior period saw reduced shipments recently, leading to a notable decrease in overall arrivals. Going forward, the price difference between north and south China remains insignificant in the near term, and the redirection of mainstream resource shipments may persist, meaning Lecong arrivals may still have room to pull back in the short term.

Chart-2: Lecong Market Arrivals

Source: SMM Steel

SMM publishes mainstream market HRC shipment flow data every Tuesday. To subscribe or follow more data, please scan the QR code below.

![[SMM Lecong HRC Inventory] Lecong Inventory Continued to Accumulate This Week](https://imgqn.smm.cn/usercenter/LSkpO20251217171720.jpg)

![[SMM Ningbo HRC Inventory] Inventory Decline Narrowed This Week](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)