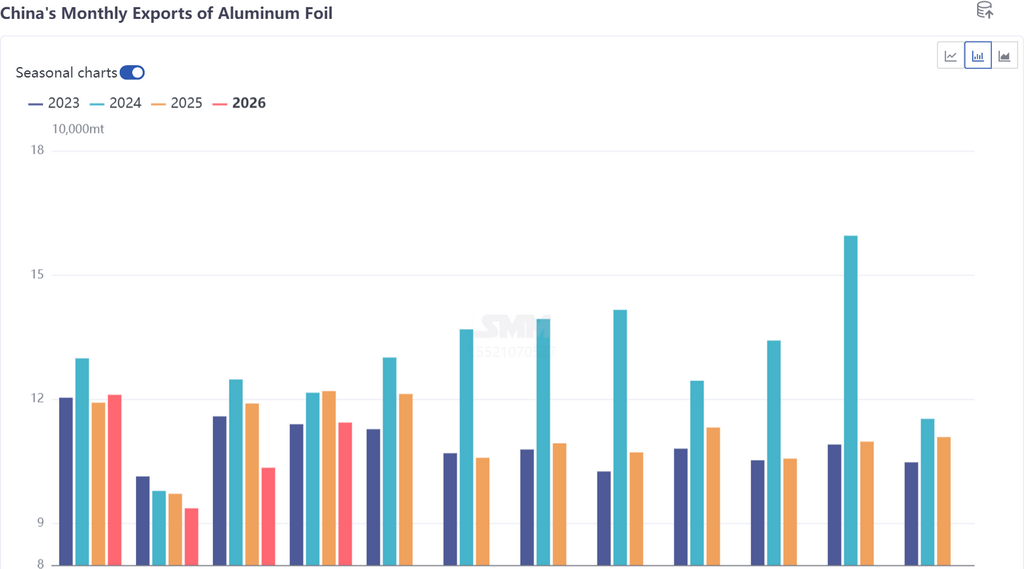

According to customs data, China's total aluminum foil exports (tariff codes 76071110, 76071120, 76071190, 76071900, 76072000) reached 114,400 mt in April 2026, up 10.5% MoM but down 6.2% YoY.

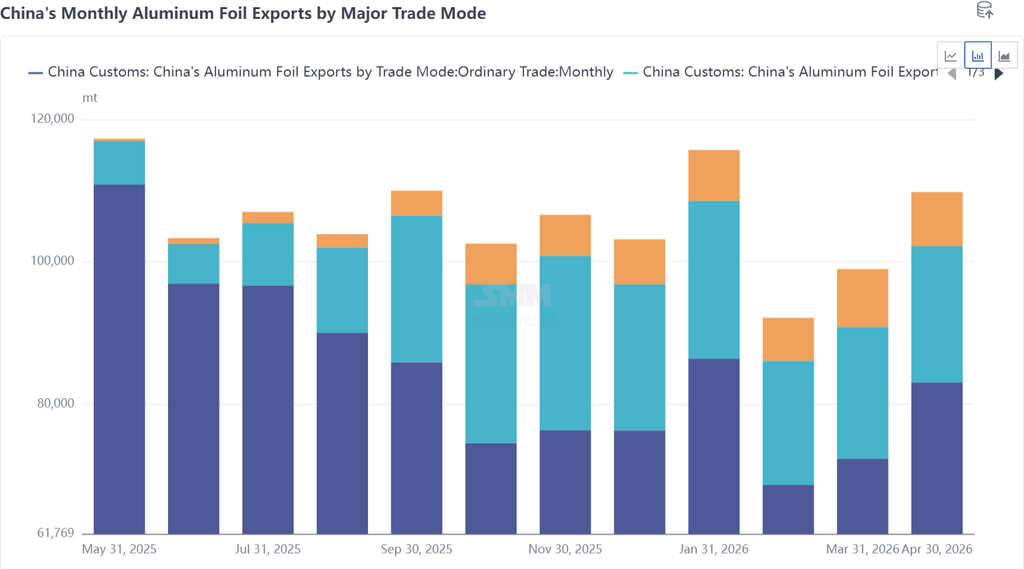

Trade mode: In April 2026, China's aluminum foil exports via processing trade with imported materials were approximately 19,200 mt, accounting for about 16.8%; exports via processing trade with supplied materials were approximately 7,500 mt, accounting for 6.6%.

By country, the top five destinations for China's aluminum foil exports in April 2026 were Thailand (11,000 mt, 10.62%), South Korea (8,700 mt, 8.4%), Mexico (8,100 mt, 7.78%), India (7,000 mt, 6.8%), and Indonesia (0.64 mt, 6.2%), with the remaining countries collectively accounting for about 60%. The Southeast Asian market maintained stable contributions. Notably, exports to the Middle East showed initial recovery: exports to the UAE rebounded from 2,515 mt in March to 4,441 mt in April, and exports to Saudi Arabia rebounded from 4,868 mt to 6,387 mt. However, according to SMM survey, the recovered volumes were mainly rerouted via the Red Sea and represented only a small fraction of normal levels. Most clients had not yet resumed placing orders, and the Middle East trade chain remained far from normalcy.

Entering Q2, China's aluminum foil exports exhibited a typical geopolitically-driven cyclical boom: On one hand, some double zero foil production lines switching to battery foil led to supply contraction in traditional packaging foil. Combined with overseas clients rushing to export due to concerns over prolonged Strait of Hormuz blockade, enterprise production schedules had been extended to late June through July, with processing fees for double zero standard pouch export surging to $1,000-1,200/mt. On the other hand, high processing fees themselves were already slowing the pace of additional client orders, and the widening price spread between domestic and overseas markets had not brought significant order growth (above 20%), indicating limited actual shortages overseas, with incremental volumes driven more by precautionary restocking rather than a comprehensive recovery in end-use demand. For the full year, cumulative aluminum foil exports from January to April were still down 5.4% YoY. To recover the ground lost in 2025 (1.3406 million mt), subsequent monthly exports would need to reach 113,500 mt. In an optimistic scenario, if the strait blockade continues into Q3 and the export rush persists, full-year exports will reach 1.4 million mt; in a conservative scenario, if the blockade is lifted, leading to convergence of overseas market premiums and demand being front-loaded, full-year exports will only reach 1.3 million mt. The duration of geopolitical conflict and the extent of actual overseas shortages are the core variables determining whether full-year exports can "recover lost ground."