I. Market Status: Negative TCs Enter Triple Digits, Structural Tightening in Copper Concentrate Supply-Demand

As global smelter capacity continues to climb, China, as the world's largest copper smelting country, faces a continuously declining self-sufficiency rate in copper concentrates and rising external dependency. Compounded by geopolitical crises, production cuts by ex-China miners, declining mine grades, and frequent production accidents, the copper industry has undergone a dramatic shift from "tight balance" to "structural deficit." Currently, the global copper concentrate market has fallen into a state of persistently tight supply.

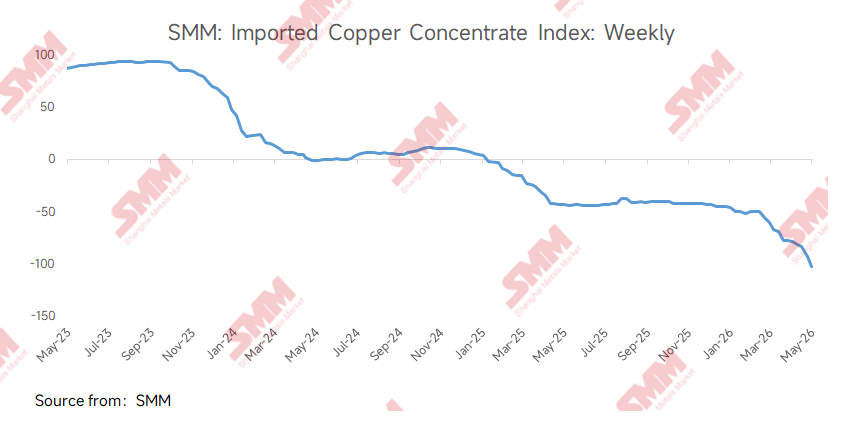

On May 15, the SMM Imported Copper Concentrate Index (weekly) reported -$102.84/dmt, breaking through the -$100/dmt threshold for the first time in history, setting a record negative depth. The payable indicator for 20%-grade domestic trade ore was 97.5%-98.5%, up 0.5 percentage points MoM.

Supply-side factors driving TCs persistently lower continue to accumulate. 1) Full production resumptions at Freeport's Grasberg mine have fallen short of expectations. According to Freeport's Q1 earnings call, the company plans to achieve full production resumptions by the end of 2027; 2) The Peruvian government signed Emergency Decree No. 003-2026 on May 11, triggering widespread market concerns over the country's energy supply and copper mine output; 3) Geopolitical disruptions—the continued blockade of the Strait of Hormuz has driven sulfur prices persistently higher, pushing smelting acid prices to rise continuously. With smelting profits climbing, smelters' purchase willingness has increased, driving copper concentrate TCs persistently lower.

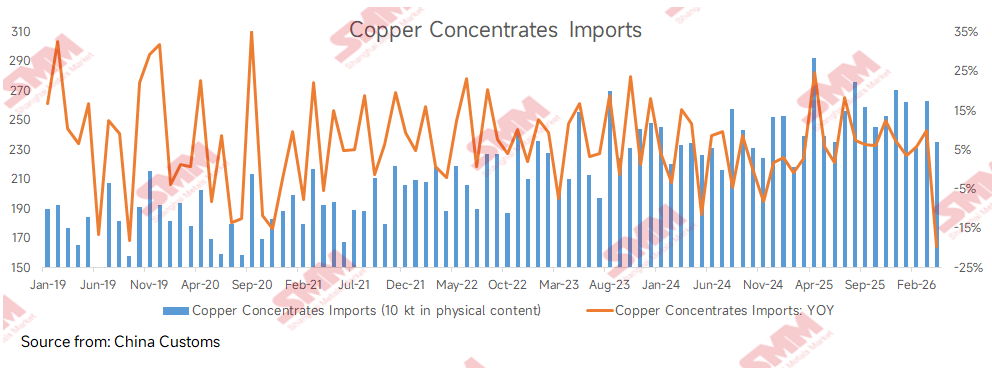

Customs data showed that China's copper ore and concentrate imports in April 2026 were 2.352 million mt in physical content, down 19.57% YoY; cumulative imports from January to April were 9.915 million mt in physical content, down 0.8% compared to the same period last year. Since December 2020, China's copper concentrate cumulative imports had maintained positive YoY growth; this marks the first decline in over five years.

II. Smelter Operating Rates Stay High

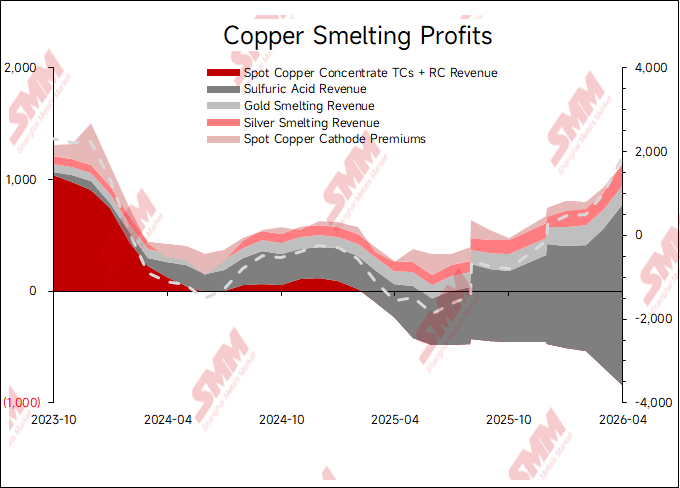

Contrary to the intuition of "industry-wide losses" implied by deeply negative TCs, operating rates at China's copper smelters have not experienced a cliff-like decline. From a pure smelting perspective, operating willingness and actual profitability across different types of enterprises show significant divergence. Under the extreme environment of deeply negative TCs, the core reason China's copper smelters can maintain relatively resilient operations is that by-product revenues are becoming the key variable determining break-even. Meanwhile, China's copper cathode production declined MoM due to the maintenance peak. SMM data showed that China's copper cathode production in April fell 2.26% MoM. Cumulative copper cathode production from January to April 2026 reached 4.7067 million mt. However, according to SMM, some smelters postponed their maintenance plans or completed crude smelting maintenance ahead of schedule to capture revenue from the by-product sulphuric acid.

III. Breakdown of Smelter Profit Sources

(i) Sulphuric Acid: The Strongest Profit Contributor at the Current Stage

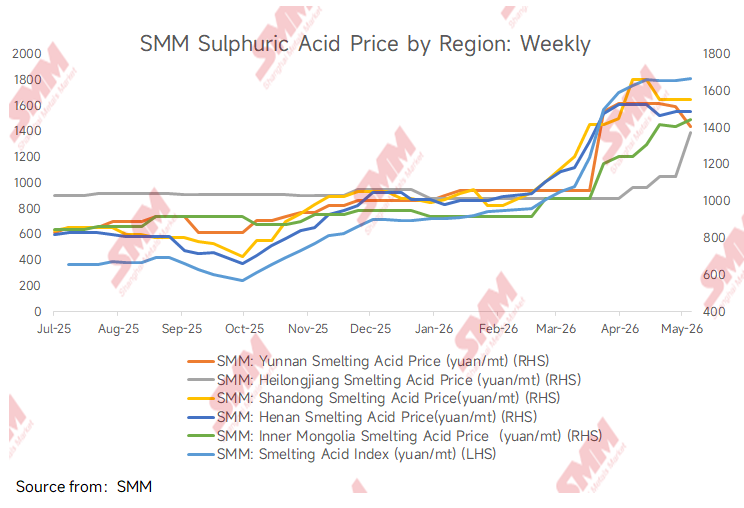

Sulphuric acid is currently the most important by-product profit source for smelters. In pyrometallurgy-based copper cathode production, approximately 3-4 mt of sulphuric acid is produced as a by-product for every 1 mt of copper cathode. As of May 15, the SMM China Copper Smelting Acid Index stood at 1,665 yuan/mt, up 83.7% from the beginning of the year. Sulphuric acid prices currently stay high, meaning sulphuric acid revenue can offset a considerable portion of the revenue loss caused by negative TCs. However, this "sulphuric acid moat" is facing policy challenges. China suspended exports of ordinary industrial sulphuric acid and smelting by-product sulphuric acid starting in May for a period of 8 months. The export ban is not intended to suppress domestic sulphuric acid prices, but rather to prioritize domestic supply for agricultural phosphate fertiliser production and strategic industries such as new energy. Demand side, overall sulphuric acid demand remains tight. Although downstream sectors including phosphate fertiliser, titanium dioxide, and new energy materials saw declining operating rates due to high-priced raw materials, just-in-time procurement still exists. Meanwhile, the supply side is also constrained by concentrated smelter maintenance and high sulphur-based acid production costs, with industry-wide capacity utilization rates at low levels. Cost side, firm sulphur prices provide bottom support for sulphuric acid; supply side, concentrated maintenance limits downside room; demand side, although weak, has not yet formed a substantial enough impact to break down high prices. This means sulphuric acid continues to serve as a profit pillar for smelters.

(ii) Precious Metal Recovery: "Incremental Game" Under High Copper Prices

In addition, copper concentrates typically contain associated precious metals such as gold and silver, which can be recovered through anode slime processing during smelting. Copper prices are currently at historically high levels, and gold prices also fluctuate at highs, greatly enhancing the economics of precious metal recovery. According to SMM market sources, when gold and silver prices are at high levels, raw materials with impurities rich in gold and silver are assigned extremely high added value. The profit contribution of precious metal recovery to smelters is reflected in: smelters can achieve recovery utilization rates exceeding the gold and silver payable indicators through refined processing, profiting from spot smelting revenue. This portion of revenue is often a significant component of smelters' comprehensive profit structure. However, as gold and silver prices continue to rise, suppliers in the copper concentrates spot trade are simultaneously raising gold and silver payable indicators. The continuously rising precious metal payable indicators and payable benchmark pose an increasingly severe challenge to smelter profitability.

IV.Future Trends: Coexistence of Industry Landscape Evolution and Technology Upgrade Requirements

However, industry chain profits are irreversibly shifting toward the upstream ore side. Under the medium and long-term landscape of persistently tightening copper concentrates supply and demand, the scarcity value of the resource side is being reassessed by the market. As the copper concentrates supply-demand gap persists over the medium and long-term horizon, and smelters' bargaining power will remain under pressure over the long term. The market is widely concerned about whether TC can quickly pull back in tandem once the continuously rising sulphuric acid prices reach a turning point. Facing the long-term trend of profit squeeze at the mine end and losses in the smelting segment, the future landscape of the copper smelting industry will evolve in the following directions: Direction 1: Integrated consolidation extending upstream. Enterprises with upstream mine assets will have a significant advantage in profitability. Direction 2: Technological upgrades to achieve differentiated competition. Against the backdrop of narrowing profit margins from non-payable metals, the technological barriers of smelters will become increasingly important. Those who can more efficiently extract valuable metals from low-grade ore or complex ore will seize the initiative in the industry reshuffle.

Under the extreme environment of persistently negative TCs, sulphuric acid by-product revenue and precious metal recovery are the core profit pillars currently sustaining smelter operations. The supply-demand pattern dictates that the pricing power and profit margins at the mine end will continue to outperform those at the smelting end. The copper smelting industry is transitioning from the traditional model of "earning TCs" to a new competitive landscape of "resource control + technological barriers + integrated operations."

![Macro Tailwinds Underpinned Copper Prices as BC Copper Price Spread Between Domestic and Overseas Markets Remained Inverted [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/LbxVx20251217171714.jpeg)