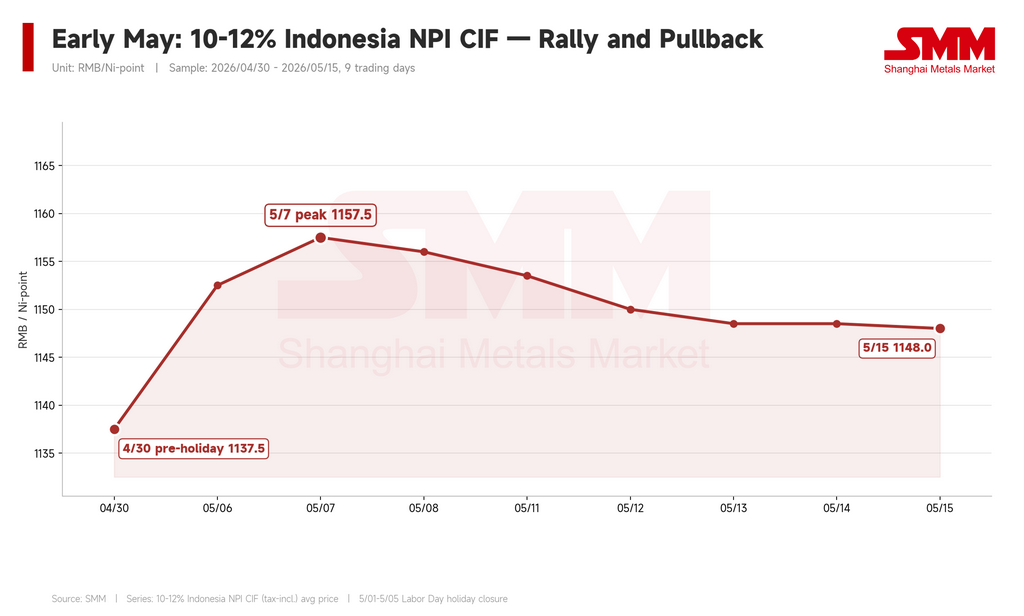

The rally that carried Nickel Pig Iron (NPI) prices higher through late April did not collapse in early May — but it did stop advancing. Indonesian NPI (10–12% Ni grade, DDP China) averaged approximately $170/Ni point (RMB 1,157.5/Ni point) on May 7, up from $167/Ni point (RMB 1,137.5/Ni point) at the end of April. But the high didn't hold. By May 15, prices had pulled back to around $169/Ni point (RMB 1,148/Ni point).

The market has shifted from a consensus rally into what can best be described as a "high-price validation phase." The question is no longer whether mills will accept higher NPI prices — they already did in late April. The question now is whether they'll keep accepting them as the conditions that justified those prices erode one by one.

The rally's last push — and why it peaked

NPI continued higher immediately after the May Day holiday. Sellers came back with offers at $172–176/Ni point (RMB 1,170–1,200/Ni point), particularly for premium material above 11.5% Ni. Three factors sustained the bullish mood briefly.

First, the price anchor had already been reset. Multiple transactions above $169/Ni point (RMB 1,150/Ni point) had been confirmed in late April, giving sellers confidence to push higher. Second, port inventories remained tight — NPI stocks at Chinese ports fell from 345,000 mt on April 30 to 315,000 mt by May 7, drawing down 30,000 mt in a single week. Third, high-grade material (12–14% Ni) stayed scarce, with those grades commanding approximately $175/Ni point (RMB 1,190/Ni point), and ultra-high-grade material (≥14% Ni) pricing near $177/Ni point (RMB 1,202.5/Ni point).

But the $176/Ni point level proved to be more of a seller aspiration than a market-clearing price for standard 10–12% material. Mainstream transactions stayed well below that, and the early-May peak was short-lived.

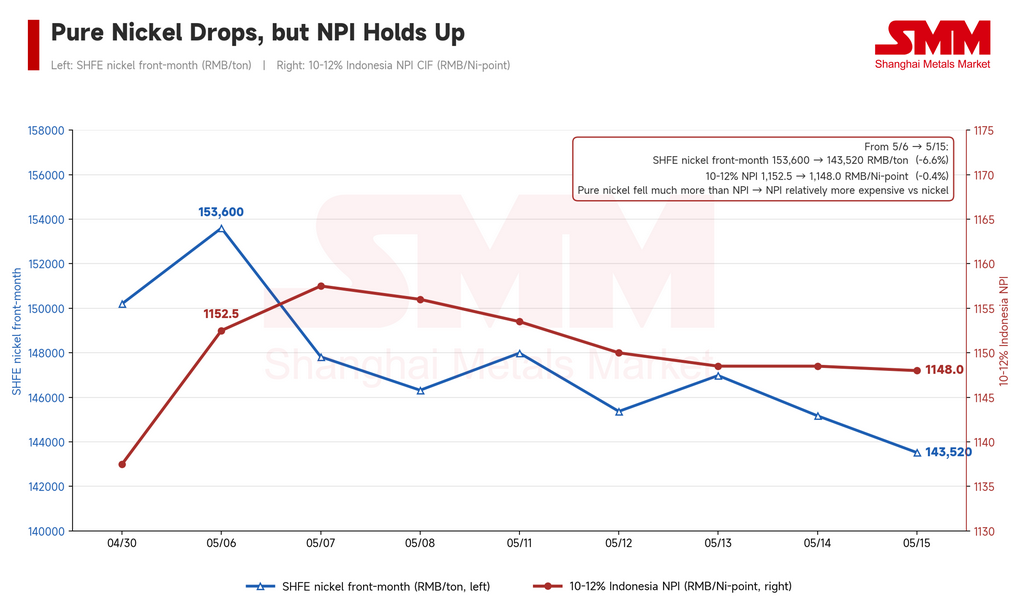

Refined nickel retreated — but NPI didn't follow

The most important shift in early May came from the SHFE nickel contract. The front-month nickel futures dropped from approximately $22,555/mt (RMB 153,600/mt) on May 6 to around $21,074/mt (RMB 143,520/mt) by May 15 — a decline of roughly 6.6%.

NPI prices, however, barely moved. This created a critical repricing dynamic: NPI became more expensive relative to refined nickel.

The NPI-to-electrolytic-nickel discount — a closely watched metric in China that measures how "cheap" NPI is versus pure nickel on a per-nickel-point basis — tells the story clearly. On April 30, NPI traded at a discount of approximately $53/Ni point (RMB 361/Ni point) to refined nickel. By May 6, that discount widened briefly to $55/Ni point (RMB 376/Ni point). But as nickel futures fell and NPI held firm, the discount narrowed rapidly: to $47/Ni point (RMB 322/Ni point) on May 7 and just $42/Ni point (RMB 284/Ni point) by May 15.

The implication is straightforward. In late April, rising nickel prices had opened headroom for NPI to follow higher — refined nickel was effectively pulling NPI up. But once nickel reversed, that external support disappeared. If NPI insists on holding elevated levels while the reference metal falls, mills start questioning the value proposition. Refined nickel is no longer NPI's tailwind; it's becoming the buyers' benchmark for pushing back.

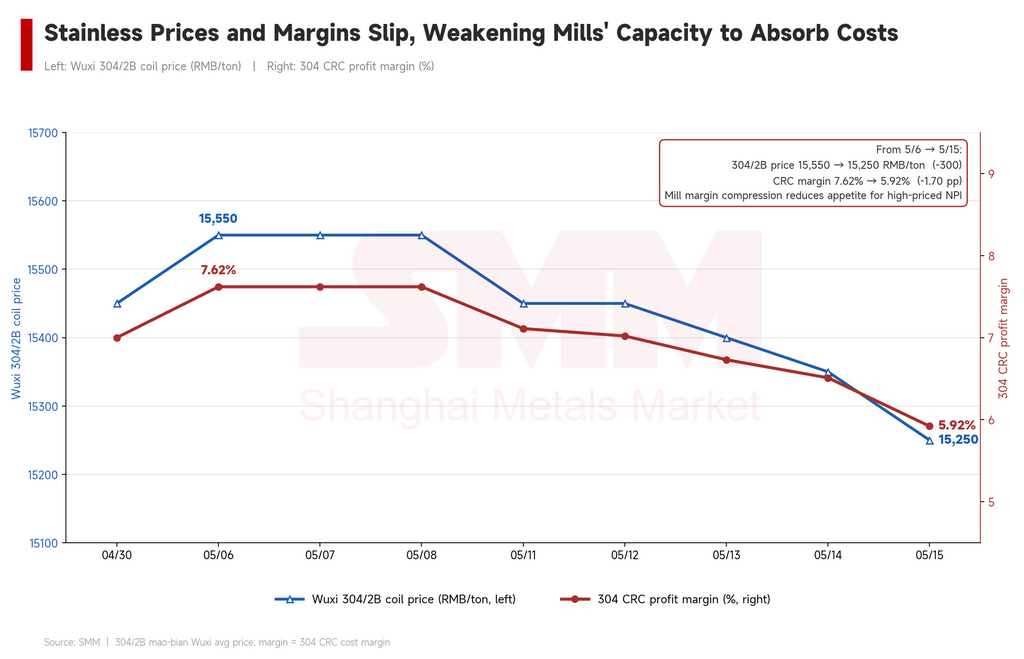

Stainless margins narrow, weakening mills' ability to absorb high-cost feedstock

The second leg of support that is fading: stainless steel profitability.

The late-April NPI rally was underpinned by improving mill margins — stainless prices were rising, and mills could afford to pay more for raw materials. That equation has shifted. SMM data shows that Wuxi 304/2B cold-rolled coil (trimmed edge) averaged around $2,283/mt (RMB 15,550/mt) in early May before falling to approximately $2,239/mt (RMB 15,250/mt) by May 15 — a drop of roughly $44/mt (RMB 300/mt) from the recent peak.

Correspondingly, 304 cold-rolled margins declined from 7.62% in early May to 5.92% by May 15. Margins remain positive — mills are still profitable — but the trajectory is unmistakably downward. As margins compress, mills' willingness to accept high-priced NPI diminishes. They begin shifting from "secure supply at whatever cost" mode back to "optimize procurement cost" mode.

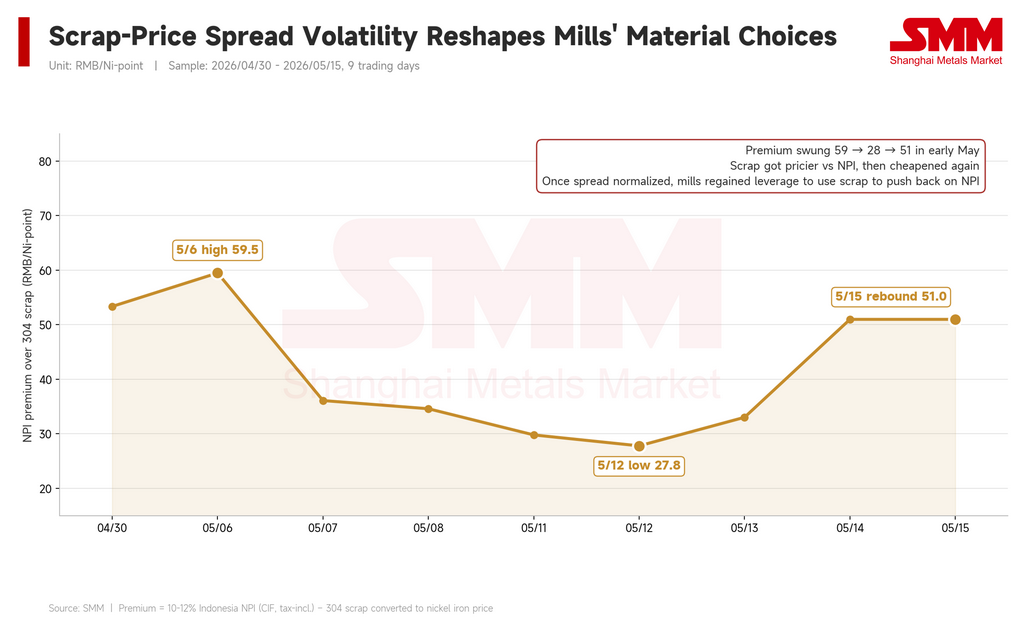

Scrap prices fall, giving mills fresh ammunition to pressure NPI

The scrap market added a third source of pressure. In late April, rising stainless steel prices had pulled scrap higher as well, compressing NPI's cost premium over scrap and temporarily making NPI more competitive in furnace economics. That gave mills less reason to resist NPI price increases.

But in early May, as stainless prices weakened, scrap followed. Grade 304 stainless scrap in Shanghai fell from approximately $1,593/mt (RMB 10,850/mt) in early May to around $1,564/mt (RMB 10,650/mt) by May 15. NPI's premium over scrap on a nickel-equivalent basis, which had compressed to as low as $4.1/Ni point (RMB 27.8/Ni point) on May 12, widened back to $7.5/Ni point (RMB 50.98/Ni point) by May 15.

The dynamic is clear: when scrap gets cheaper, it re-emerges as a viable alternative — and as a lever mills can use to pressure NPI sellers. In late April, mills had limited scrap-based pushback options. By mid-May, that tool is back in their hands.

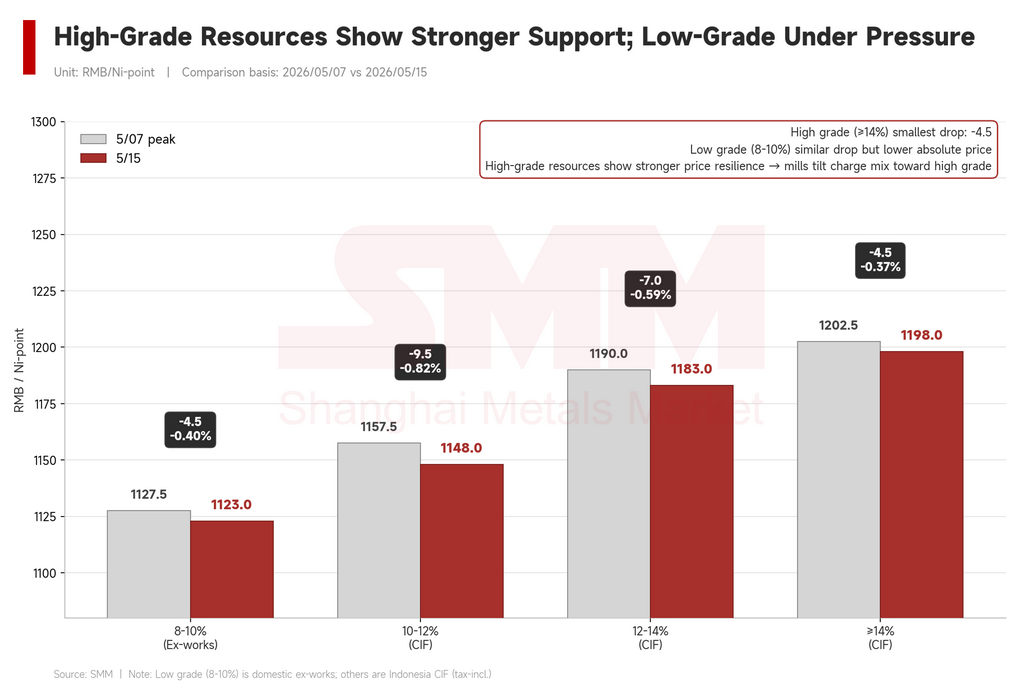

High-grade holds, low-grade struggles — the grade divide persists

Not all NPI weakened equally. The grade-based divergence that has been building for months remained firmly in place.

Standard 10–12% Indonesian NPI fell from $170/Ni point to $169/Ni point over the period. Higher-grade 12–14% material eased from $175/Ni point (RMB 1,190/Ni point) to $174/Ni point (RMB 1,183/Ni point). Ultra-high-grade ≥14% material slipped marginally from $177/Ni point (RMB 1,202.5/Ni point) to $176/Ni point (RMB 1,198/Ni point). The higher the grade, the smaller the pullback.

Meanwhile, domestically produced low-grade NPI (8–10% Ni) fell from approximately $166/Ni point (RMB 1,127.5/Ni point) to $165/Ni point (RMB 1,123/Ni point). The absolute decline looks modest, but in a high-price environment, low-grade material's transaction elasticity and bargaining power are visibly weaker than high-grade alternatives. Mills operating under margin pressure prioritize charge efficiency and comprehensive cost — they'll pay up for 12%+ material but push hard on anything below 10%.

The structural story remains unchanged: high-grade is tight and supported; low-grade faces persistent selling pressure.

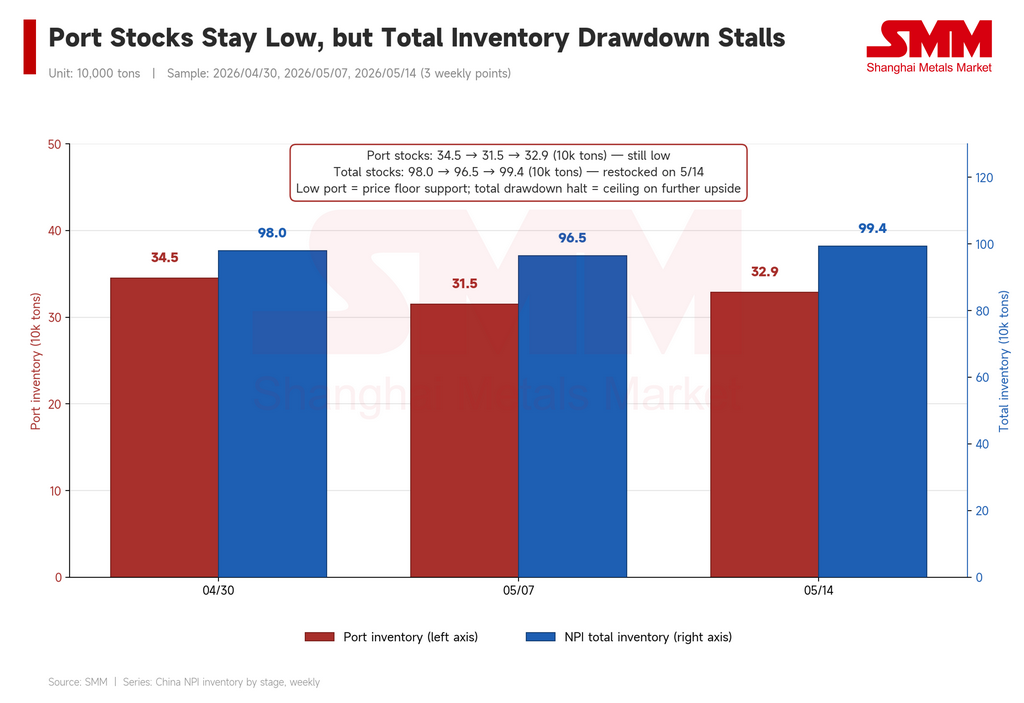

Inventories provide a floor — not a springboard

Port inventories recovered modestly from their early-May lows — rising from 315,000 mt on May 7 to 329,000 mt by May 14 — but remained below end-of-April levels. Total NPI inventories (port plus inland) dipped to 965,000 mt on May 7 before rebounding to 993,800 mt by May 14, with days of inventory cover holding steady around 25 days.

The takeaway: available material at ports — especially tradeable high-grade stock — remains limited, which is enough to prevent sellers from capitulating. But overall inventories have stopped drawing down, meaning the post-holiday restocking impulse has faded. Low stocks can defend a price floor, but they alone cannot push standard 10–12% material toward the $176/Ni point level that sellers aspire to — not when nickel, margins, and scrap are all moving in the other direction.

Outlook: a market in standoff

Early May marked a transition from momentum-driven buying to price discovery under tightening constraints. The bull case isn't dead — port stocks remain lean, high-grade material is genuinely scarce, and some mills still need to cover June requirements. Premium material (12%+ Ni) retains near-term support.

But the bear case has strengthened materially. SHFE nickel has dropped over $1,470/mt (RMB 10,000/mt) from its post-holiday high. Stainless steel margins have retreated from 7.6% to under 6%. Scrap is cheapening. And critically, NPI's discount to refined nickel has compressed from $55 to $42 per nickel point in under two weeks — meaning NPI is no longer the obvious value play it was in late April.

The likely near-term range for standard 10–12% NPI sits around $166–172/Ni point (RMB 1,130–1,170/Ni point). Whether prices break higher or lower from that range depends on three variables: whether stainless steel prices stabilize, whether scrap availability remains constrained, and whether mills' June procurement needs generate a fresh wave of buying. Absent those catalysts, standard-grade NPI will likely consolidate at current levels while low-grade material faces increasing difficulty finding buyers.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Analysis] Indonesia's Nickel Benchmark Price Broke Through $18,000 with Strong Momentum, Extreme Weather and Policy Dynamics Intensified Price Divergence](https://imgqn.smm.cn/usercenter/sKmGT20251217171733.jpg)