ข่าว SMM วันที่ 15 พฤษภาคม:

ในเดือนพฤษภาคม 2026 ตลาดโมลิบดีนัมโลกยังคงอยู่ในภาวะอุปทานตึงตัวต่อเนื่อง โดยราคาขยายและเร่งแนวโน้มขาขึ้นที่เห็นในเดือนเมษายน ราคามอลิบดีนัมออกไซด์ในต่างประเทศพุ่งต่อเนื่องในระดับสูง ขณะที่ราคาโมลิบดีนัมคอนเซนเทรตและเฟอร์โรโมลิบดีนัมในประเทศทำจุดสูงสุดใหม่เป็นระยะ ๆ ณ วันที่ 15 พฤษภาคม ราคาโมลิบดีนัมคอนเซนเทรตเกรด 45% แตะ 5,200 หยวนต่อหน่วยตัน และเฟอร์โรโมลิบดีนัมทำธุรกรรมสูงสุดที่ 330,000 หยวนต่อตัน ห่วงโซ่อุตสาหกรรมโมลิบดีนัมปรับขึ้นทั่วกระดาน โดยราคาเข้าใกล้สถิติสูงสุดที่ทำไว้ในเดือนกุมภาพันธ์ 2023

ด้านอุปทาน พลวัตตลาดถูกจำกัดจากการยืนราคาของผู้ผลิตเหมืองในประเทศและความไม่เต็มใจขาย รวมถึงการหยุดชะงักของอุปทานต่างประเทศ เมื่อผนวกกับความคาดหวังการหดตัวของอุปทานที่เกิดจากกฤษฎีกาภาวะฉุกเฉินด้านพลังงานของเปรู ปัจจัยเหล่านี้จึงกลายเป็นตัวเร่งหลักของการปรับขึ้นในเดือนนี้ ด้านอุปสงค์ การบริโภคแบบจำเป็นจากภาคเหล็กพิเศษและสเตนเลสยังคงทรงตัว ขณะที่อุปสงค์จากพลังงานใหม่และการผลิตระดับไฮเอนด์ขยายตัวต่อเนื่อง ช่วยพยุงราคาโมลิบดีนัมให้อยู่ในระดับสูง ตลาดมีลักษณะ ขึ้นง่าย ลงยาก ในระยะสั้น

I. แนวโน้มราคา: ปรับขึ้นวงกว้างและเพิ่มขึ้นเด่นชัด

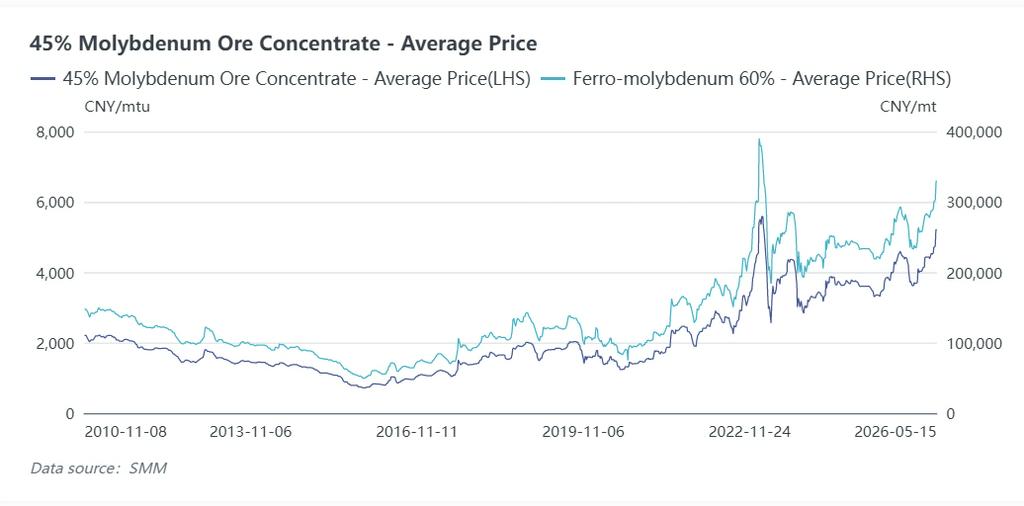

ราคาโมลิบดีนัมในประเทศยังคงแข็งแกร่งในเดือนพฤษภาคม โดยจุดศูนย์กลางราคาขยับสูงขึ้นอย่างต่อเนื่อง และผลตอบแทนรายเดือนขยายตัวอย่างมีนัยสำคัญ ณ วันที่ 15 พฤษภาคม ราคาซื้อขายหลักของโมลิบดีนัมคอนเซนเทรตเกรด 45%–50% อยู่ที่ 5,180–5,210 หยวนต่อหน่วยตัน เพิ่มขึ้นราว 450 หยวนต่อหน่วยตันเมื่อเทียบเดือนก่อน และเพิ่มสะสมตั้งแต่ต้นปี 38.7%

ราคาเสนอขายสปอตเฟอร์โรโมลิบดีนัมรวมภาษีปรับขึ้นเป็น 325,000–332,000 หยวนต่อตัน เพิ่มขึ้น 28,000 หยวนต่อตันเมื่อเทียบเดือนก่อน และเพิ่มสะสมตั้งแต่ต้นปี 32.2% ราคาประมูลจัดซื้อของโรงงานเหล็กก็ปรับขึ้นต่อเนื่อง จาก 300,000 หยวนต่อตันช่วงต้นเดือนเป็น 324,000 หยวนต่อตัน ท่ามกลางการปรับขึ้นรวดเร็ว โรงงานเหล็กชะลอการเข้าร่วมประมูล โดยบางแห่งระงับการจัดซื้อและรอดูสถานการณ์

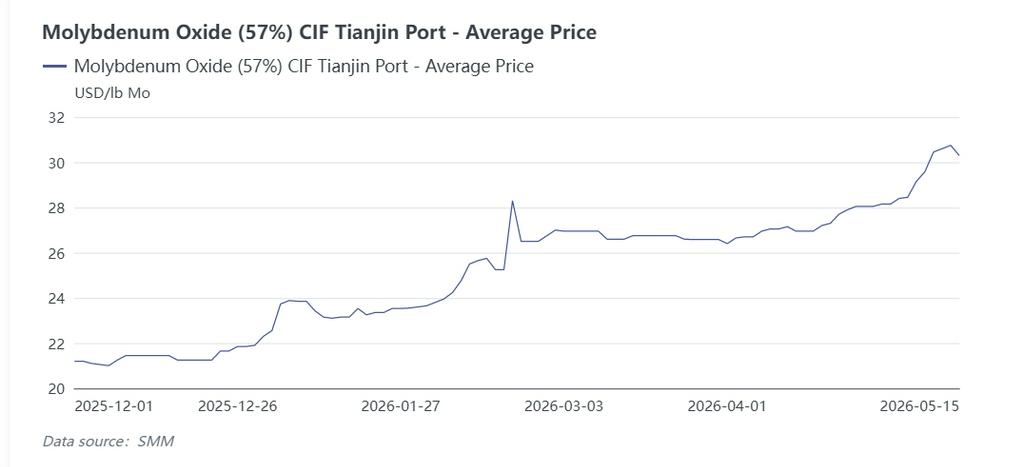

ในตลาดต่างประเทศ ราคา CIF ของมอลิบดีนัมออกไซด์ที่ท่าเรือเทียนจินปิดที่ 30.3 ดอลลาร์สหรัฐต่อปอนด์โมลิบดีนัม เพิ่มขึ้น 2.15 ดอลลาร์สหรัฐต่อปอนด์เมื่อเทียบเดือนก่อน และเพิ่มสะสมตั้งแต่ต้นปี 35.9% ความคาดหวังอุปทานตึงตัวในต่างประเทศผลักดันให้ราคาโมลิบดีนัมสากลทรงตัวในระดับสูง สะท้อนความเชื่อมโยงที่ชัดเจนระหว่างตลาดในประเทศและต่างประเทศ

II. ด้านอุปทาน: ยืนราคาในประเทศ + สะดุดต่างประเทศ ความยืดหยุ่นอุปทานจำกัด

(1) ในประเทศ: เหมืองยืนราคาและจำกัดการขาย การเติบโตของผลผลิตเพิ่มเพียงเล็กน้อย

อุปทานแร่โมลิบดีนัมในประเทศยังคงตึงตัว เหมืองหลักชะลอจังหวะการส่งมอบด้วยความตั้งใจยืนราคาและพยุงระดับตลาด ทำให้ราคาฐานประมูลถูกยกขึ้นต่อเนื่อง ปริมาณหมุนเวียนสปอตจากเหมืองขนาดกลางและเล็กตึงตัว ส่งผลให้ทรัพยากรสปอตที่มีอยู่ในตลาดมีจำกัด

ผู้ผลิตโมลิบดีนัมคอนเซนเทรตมีคำสั่งซื้อค้างส่งแข็งแกร่ง บางรายใช้การขายรายเดือนแบบประมูล โดยส่วนใหญ่ปิดการประมูลที่ราคาพรีเมียม ช่วยหนุนการปรับขึ้นต่อเนื่องของธุรกรรมสปอตล็อตใหญ่

ขณะเดียวกัน เกรดแร่โมลิบดีนัมในประเทศลดลงปีต่อปี และการกำกับดูแลด้านสิ่งแวดล้อมและความปลอดภัยเข้มงวดขึ้น ปีนี้มีเพียงเฟส 2 ของเหมืองจูหลงที่ปล่อยกำลังการผลิตใหม่เพิ่มเล็กน้อย ทำให้การเติบโตของผลผลิตโมลิบดีนัมคอนเซนเทรตในประเทศมีจำกัด คาดว่าผลผลิตทั้งปีจะเพิ่มขึ้น 12% เมื่อเทียบปีก่อน เป็นราว 160,000 ตันโมลิบดีนัม (โลหะ) ขณะที่ผลผลิตช่วงมกราคม–เมษายนเพิ่มขึ้นเมื่อเทียบปีก่อนเพียง 5%

(2) ต่างประเทศ: วิกฤตพลังงานของเปรูจุดชนวนความกังวลอุปทานหดตัว

เมื่อวันที่ 11 พฤษภาคม ประธานาธิบดีรักษาการของเปรูลงนามและประกาศใช้ กฤษฎีกาภาวะฉุกเฉินเลขที่ 003-2026 ประกาศภาวะฉุกเฉินด้านพลังงานทั่วประเทศอย่างเป็นทางการ มีผลถึงวันที่ 31 ธันวาคม 2026

มาตรการหลักรวมถึงการให้อำนาจกระทรวงพลังงานและเหมืองแร่จัดหาเงินทุนที่รัฐค้ำประกัน 2 พันล้านดอลลาร์สหรัฐ เพื่อค้ำจุนการดำเนินงานของ Petroperú และรับประกันอุปทานน้ำมันเบนซิน ดีเซล และเชื้อเพลิงอื่น ๆ ภายในประเทศ พร้อมกันนี้จะใช้มาตรการปันส่วนพลังงานโดยให้ความสำคัญกับความเป็นอยู่ของประชาชน และจำกัดการใช้ไฟฟ้าและก๊าซของภาคอุตสาหกรรมและเหมืองแร่อย่างเข้มงวด โดยยังไม่มีการระบุข้อยกเว้นเฉพาะสำหรับเหมืองอย่างชัดเจน ในฐานะผู้จัดหาทรัพยากรแร่สำคัญของโลก เปรูทำให้ตลาดกังวลต่อความเสี่ยงอุปทานของโมลิบดีนัมและทรัพยากรแร่อื่น ๆ

เปรูเป็น ผู้ผลิตโมลิบดีนัมรายใหญ่อันดับ 4 ของโลก คิดเป็นราว 12.7% ของผลผลิตโมลิบดีนัมโลกในปี 2025 การผลิตโมลิบดีนัมของเปรูเกือบทั้งหมดเป็นผลพลอยได้จากเหมืองทองแดงซึ่งใช้พลังงานสูง การเปลี่ยนแปลงผลผลิตโมลิบดีนัมจึงสามารถประเมินคร่าว ๆ จากแนวโน้มการผลิตทองแดงของเปรูได้

ตามการวิเคราะห์อุตสาหกรรมของ SMM ผลผลิตทองแดงของเปรูลดลง 10%–15% เมื่อเทียบเดือนก่อนในเดือนเมษายน โดยอัตราการเดินเครื่องเหมืองเคยลดลงเหลือ 60%–70% แหล่งข่าวในอุตสาหกรรมประเมินว่าการฟื้นตัวของการจ่ายไฟเต็มรูปแบบจะใช้เวลา 2–3 เดือน คาดว่าผลผลิตโมลิบดีนัมของเปรูจะลดลง 4%–6% ในระยะสั้น ทำให้ช่องว่างอุปทานโมลิบดีนัมโลกกว้างขึ้น ขณะเดียวกัน ผลผลิตโมลิบดีนัมของชิลียังคงลดลงเมื่อเทียบปีก่อน โดยผลผลิตช่วงมกราคม–กุมภาพันธ์ลดลงสะสม 6.0% ซ้ำเติมการหยุดชะงักของอุปทานต่างประเทศและหนุนราคาโมลิบดีนัมอย่างแข็งแกร่ง

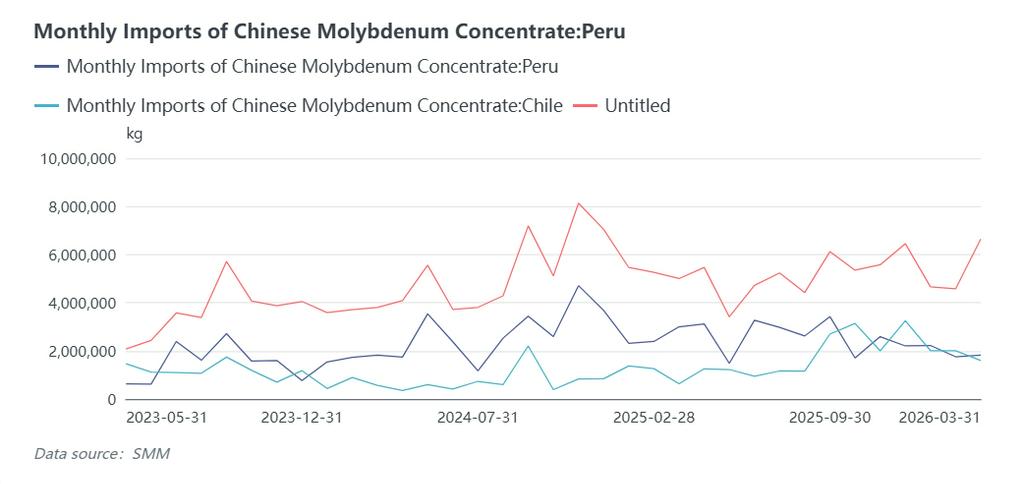

ข้อมูลศุลกากรระบุว่าในปี 2025 เปรูส่งออกโมลิบดีนัมคอนเซนเทรตไปจีนราว 31,000 ตัน คิดเป็น 49.6% ของการนำเข้ารวมของจีน ไตรมาส 1 ปี 2026 จีนนำเข้าโมลิบดีนัมคอนเซนเทรตจากเปรู 5,796 ตัน ลดลง 24.7% เมื่อเทียบปีก่อน และคิดเป็น 36.5% ของการนำเข้ารวมในไตรมาส 1 เนื่องจากขาดกำลังการถลุงปลายน้ำภายในประเทศ เปรูจึงส่งออกโมลิบดีนัมคอนเซนเทรตเกือบทั้งหมด โดยหลักไปยังชิลี จีน และภูมิภาคอื่น ๆ

III. ด้านอุปสงค์: อุปสงค์สเตนเลสและเหล็กพิเศษทรงตัว ปริมาณประมูลเฟอร์โรโมลิบดีนัมเพิ่มขึ้น

ตารางการผลิตปลายน้ำของสเตนเลสและเหล็กพิเศษในจีนยังอยู่ในเกณฑ์ดีตั้งแต่ปี 2026 ผลผลิตสเตนเลสทั่วประเทศในเดือนเมษายน 2026 อยู่ที่ 3.499 ล้านตัน ลดลง 1.3% เมื่อเทียบเดือนก่อน และลดลง 0.38% เมื่อเทียบปีก่อน

แยกตามเกรด: ซีรีส์ 200 อยู่ที่ 1.011 ล้านตัน ลดลง 3.25% เมื่อเทียบเดือนก่อน; ซีรีส์ 300 อยู่ที่ 1.851 ล้านตัน เพิ่มขึ้น 0.38% เมื่อเทียบเดือนก่อน; ซีรีส์ 400 อยู่ที่ 637,000 ตัน ลดลง 2.9% เมื่อเทียบเดือนก่อน ผลผลิตสเตนเลสยังอยู่ในระดับค่อนข้างสูงในเดือนเมษายน โดยภาระการเดินเครื่องของโรงงานเหล็กทุกเกรดยังคงสูง และไม่มีการลดกำลังการผลิตแบบรวมศูนย์อย่างมีนัยสำคัญ

ผลผลิตสเตนเลสที่สูงในเดือนเมษายนมาจากการฟื้นตัวของการบริโภคช่วงฤดูกาลพีก ความเชื่อมั่นตลาดดีขึ้น กำไรโรงงานเหล็กฟื้นตัว และธุรกรรมตลาดดีขึ้น คาดว่าผลผลิตสเตนเลสจะยังอยู่ในระดับสูงในเดือนพฤษภาคม โดยภาระการเดินเครื่องไม่น่าลดลงอย่างเด่นชัด อัตราการเดินเครื่องปัจจุบันอยู่ในระดับค่อนข้างสูงแล้ว ทำให้มีพื้นที่จำกัดสำหรับการเพิ่มการผลิตเพิ่มเติม ด้วยกำไรการถลุงสเตนเลสที่ค่อนข้างแข็งแกร่งในช่วงไม่กี่ปีที่ผ่านมา โรงงานมีแรงจูงใจน้อยที่จะลดกำลังการผลิตเชิงรุก และแผนการผลิตจะยังแข็งแกร่งในระยะสั้น

ในภาคเหล็กพิเศษ ภายใต้แรงขับจากแนวโน้มอุตสาหกรรมและแนวนโยบายที่เอื้อต่อเหล็กพิเศษท่ามกลางผลงานเหล็กทั่วไปที่อ่อนแอ การผลิตเหล็กพิเศษในประเทศเติบโตเมื่อเทียบปีก่อน อุปสงค์ที่คึกคักจากพลังงานลม การต่อเรือ ท่อส่งน้ำมันและก๊าซ เครื่องจักรก่อสร้าง รถยนต์พลังงานใหม่ และสาขาอื่น ๆ ผลักดันให้โรงงานเหล็กจัดซื้อเฟอร์โรโมลิบดีนัมผ่านการประมูลแบบรวมศูนย์ โดยราคายื่นเสนอเพิ่มขึ้นอย่างต่อเนื่อง เป็นแรงหนุนอุปสงค์แบบจำเป็นที่มั่นคง

ปริมาณประมูลเฟอร์โรโมลิบดีนัมของโรงงานเหล็กในประเทศรวม 55,400 ตัน ในช่วงมกราคม–เมษายน เพิ่มขึ้นราว 7.8% เมื่อเทียบปีก่อน อย่างไรก็ดี เนื่องจากความสามารถทำกำไรของอุตสาหกรรมอ่อนแอ โรงถลุงเฟอร์โรโมลิบดีนัมมีศักยภาพจำกัดในการเพิ่มอัตราการเดินเครื่อง โดยผลผลิต 4 เดือนแรกอยู่ที่ราว 74,500 ตัน เพิ่มขึ้น 7.2% เมื่อเทียบปีก่อน ความตึงตัวของอุปทาน-อุปสงค์ในตลาดเฟอร์โรโมลิบดีนัมยังผลักดันให้ระดับราคาอุตสาหกรรมขยับขึ้น

แนวโน้มตลาด

ระยะสั้น รูปแบบอุปทานตึงตัวของตลาดโมลิบดีนัมยากจะพลิกกลับ ความคาดหวังการหดตัวของอุปทานจากวิกฤตพลังงานของเปรูจะยังคงก่อตัวต่อเนื่อง ขณะที่เหมืองในประเทศจะยังยืนราคาและจำกัดการขาย ราคาโมลิบดีนัมมีแนวโน้มแข็งแกร่งต่อไปพร้อมความผันผวนสูงในเดือนพฤษภาคม

อย่างไรก็ตาม ราคาที่พุ่งขึ้นของเฟอร์โรโมลิบดีนัม นิกเกิล และวัตถุดิบอื่น ๆ ได้สร้างแรงกดดันด้านต้นทุนอย่างชัดเจนต่ออุตสาหกรรมสเตนเลส ต้นทุนการถลุงสเตนเลสเกรดไฮเอนด์ที่มีโมลิบดีนัม เช่น 316L และดูเพล็กซ์ เพิ่มขึ้นอย่างมาก บีบอัตรากำไรของโรงงานเหล็ก ผู้ซื้อปลายน้ำรวมถึงโรงงานเหล็กมีความอ่อนไหวต่อราคามากขึ้น เลือกเติมสต็อกเท่าที่จำเป็นเมื่อราคาย่อตัว และไม่ค่อยต้องการจัดซื้อเชิงรุกล่วงหน้าขนาดใหญ่ ซึ่งจำกัดอัพไซด์เพิ่มเติมของราคาโมลิบดีนัม ตลาดโมลิบดีนัมเดือนพฤษภาคมจะเป็นเกมสองทาง: อุปทานตึงตัวหนุนราคา ขณะที่แรงกดดันต้นทุนปลายน้ำจำกัดการปรับขึ้นต่อ

ระยะกลางถึงยาว กำลังการผลิตโมลิบดีนัมใหม่ทั่วโลกจะเร่งปล่อยออกในช่วงปี 2027–2029 นำโดยเหมืองโมลิบดีนัมใหม่ขนาดใหญ่หลายแห่งในประเทศ อุปทานที่เพิ่มขึ้นอย่างเพียงพอในอนาคตจะช่วยคลายความตึงตัวอุปทาน-อุปสงค์อย่างมีประสิทธิภาพ ทำให้จุดศูนย์กลางราคาโมลิบดีนัมค่อย ๆ ลดลงสู่ระดับที่สมเหตุสมผล พร้อมความผันผวนของราคาที่แคบลง ราคาโดยรวมจะค่อย ๆ สอดคล้องกับตรรกะการกำหนดราคาที่ขับเคลื่อนด้วยต้นทุนการผลิตและกำไรอุตสาหกรรมที่เหมาะสม

![[SMM วิเคราะห์โมลิบดีนัม] เฟอร์โรโมลิบดีนัม: ความผันผวนสูงในเดือนเมษายน จากอุปสงค์คงที่และแรงหนุนด้านต้นทุน](https://imgqn.smm.cn/production/admin/news/cn/thumb/RWipd20171024152142.jpeg?imageView2/1/w/176/h/110/q/100)

![ตลาดโมลิบดีนัมต่างประเทศปรับตัวสูงขึ้นตามความต้องการซื้อสินค้าคงคลังจากโรงงานเหล็กในประเทศที่เพิ่มขึ้น ตลาดโมลิบดีนัมเดินหน้า [สรุปตลาดโมลิบดีนัมประจำวันโดย SMM]](https://imgqn.smm.cn/usercenter/gKDYO20251217171723.jpeg)