เมื่อกระบวนการเพิ่มกำลังการผลิตและการพาณิชย์ของแบตเตอรี่โซเดียมไอออนเร่งตัวต่อเนื่อง ผลประโยชน์ของอุตสาหกรรมถูกปลดปล่อยออกมาเร็วขึ้นในปี 2026 โดยเดือนเมษายนซึ่งเป็นช่วงสำคัญต้นไตรมาส 2 ตลาดวัสดุแคโทดและแอโนดของแบตเตอรี่โซเดียมไอออนฟื้นตัวอย่างเด่นชัด ความต้องการกักตุนของฝั่งอุปสงค์เพิ่มขึ้น จังหวะการขยายกำลังการผลิตเร่งตัว ความแตกต่างของพอร์ตผลิตภัณฑ์ชัดเจนขึ้น และอุตสาหกรรมโดยรวมมุ่งสู่การประสานกันเชิงบวกระหว่างอุปสงค์และอุปทาน

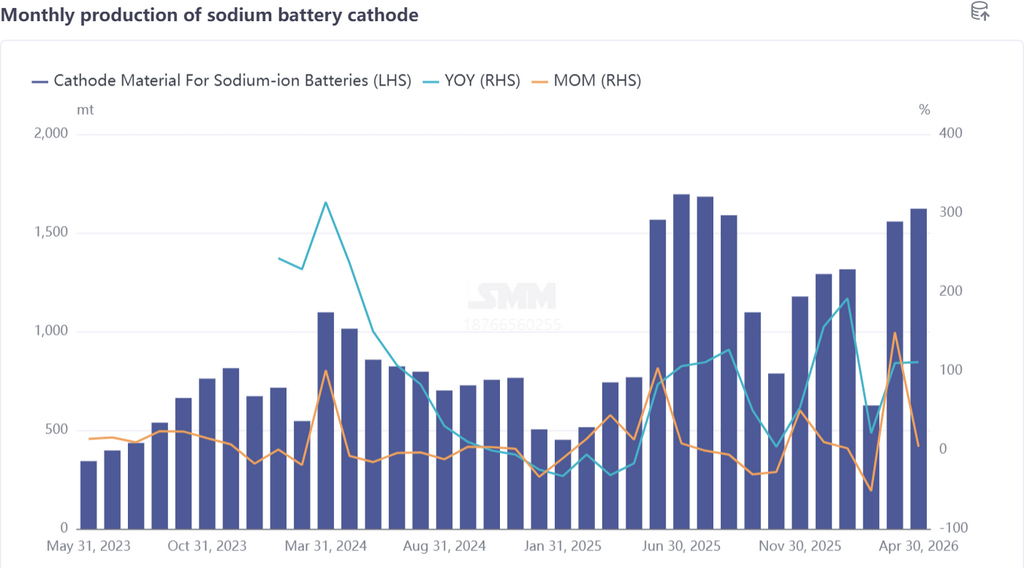

I. วัสดุแคโทด: การกักตุนคึกคักก่อนช่วงพีคซีซัน NFPP กลายเป็นแรงขับเคลื่อนการเติบโตหลัก

ในเดือนเมษายน อุปสงค์วัสดุแคโทดของแบตเตอรี่โซเดียมไอออนฟื้นตัวพร้อมบรรยากาศกักตุนที่เข้มข้น และการผลิตเติบโตทั้งเทียบรายปีและรายเดือน ข้อมูล SMM ระบุว่า ปริมาณการผลิตรายเดือนเพิ่มขึ้น 4% MoM และเพิ่มขึ้น 111% YoY สะท้อนโมเมนตัมการเติบโตที่แข็งแกร่ง

ด้านโครงสร้างผลิตภัณฑ์ วัสดุโพลีแอนไอออนครองความเป็นผู้นำอย่างเด็ดขาด คิดเป็นเกือบ 82% ของทั้งหมด เพิ่มขึ้น 5 จุดเปอร์เซ็นต์จากเดือนก่อน โดยสมรรถนะที่ยอดเยี่ยมตอบโจทย์งานกักเก็บพลังงานและระบบสตาร์ท-สต็อป ในกลุ่มนี้ NFPP (โซเดียมเหล็กฟอสเฟตไพโรฟอสเฟต) โดดเด่นเป็นพิเศษและกลายเป็นแรงขับเคลื่อนการเติบโตหลัก

ฝั่งอุปสงค์ คำสั่งซื้อแสดงเจตนาซื้อล่วงหน้า NFPP เพิ่มขึ้นอย่างมีนัยสำคัญในเดือนเมษายน โดยส่วนใหญ่ส่งมอบช่วงพฤษภาคม–มิถุนายน และเริ่มมีการส่งมอบแล้วตั้งแต่ปลายเดือนเมษายน คาดว่าในไตรมาส 2 ผู้ประกอบการ NFPP จะเห็นยอดส่งมอบพุ่งขึ้นระยะสั้น ในทางตรงกันข้าม การผลิตแคโทดแบบเลเยอร์ออกไซด์ลดลง นอกจากผู้ประกอบการแบบบูรณาการแล้ว ส่วนใหญ่เผชิญภาวะวัตถุดิบต้นน้ำ (พรีเคอร์เซอร์) ขาดแคลน—ก่อนหน้านี้จากอุปสงค์เลเยอร์ออกไซด์ที่อ่อนตัวและความคุ้มค่าต้นทุนไม่เพียงพอ ผู้ผลิตพรีเคอร์เซอร์ส่วนใหญ่ได้สลับไลน์กลับไปผลิตวัสดุไตรภาค ทำให้เติมช่องว่างอุปทานได้ยากในระยะสั้น

ที่น่าสังเกตคือ ผลิตภัณฑ์ NFPP แบบความหนาแน่นอัดสูงพึ่งพาพรีเคอร์เซอร์อย่างมาก แต่กำลังการผลิตพรีเคอร์เซอร์ NFPP ในปัจจุบันขาดแคลนรุนแรงและมีการปรับขึ้นราคา ส่งผลให้ต้นทุน NFPP ความหนาแน่นอัดสูงสูงขึ้น เนื่องจากตลาดแบตเตอรี่โซเดียมไอออนยังอยู่ในช่วงพัฒนา ผู้ผลิตเซลล์แบตเตอรี่ปลายน้ำยังคงควบคุมต้นทุนอย่างเข้มงวด การขึ้นราคา NFPP อาจเผชิญแรงต้าน ในเดือนเมษายน อุปสงค์จากภาคสตาร์ท-สต็อป ยานพาหนะสองล้อ และ ESS ถูกปลดปล่อยออกมา หนุนตลาดแคโทด มองไปเดือนพฤษภาคม การผลิตแคโทดกำลังเข้าสู่ช่วงพีคซีซัน และคาดว่าการปล่อยกำลังการผลิตเซลล์ใหม่จะหนุนให้อุปทานและอุปสงค์เติบโตพร้อมกัน โดยคาดว่าการผลิตจะเพิ่มขึ้น 19% MoM และ 23% YoY

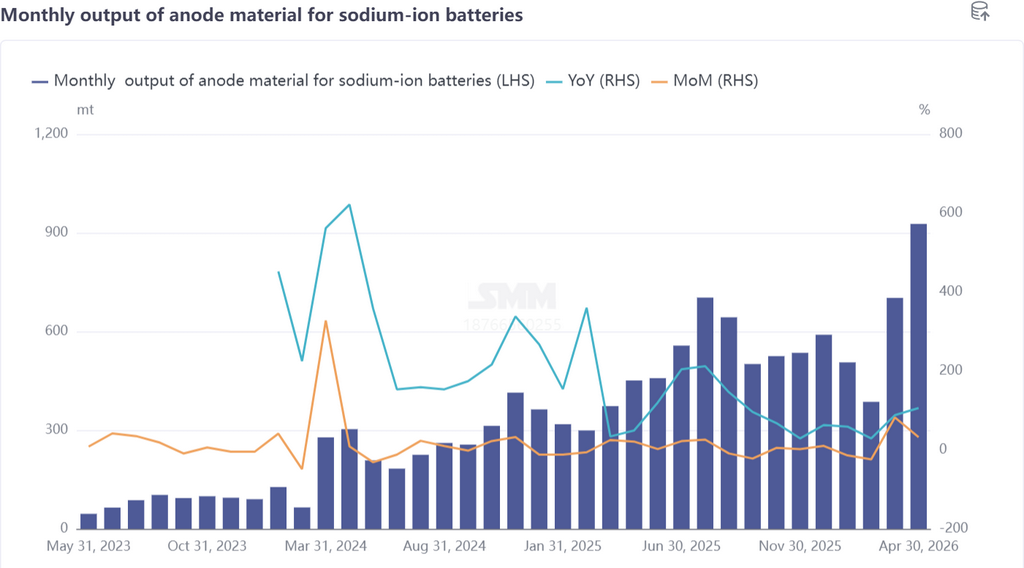

II. แอโนดฮาร์ดคาร์บอน: การผลิตพุ่งเติมช่องว่าง ขยายกำลังการผลิตเร่งตัวทะลุคอขวด

ตลาดแอโนดฮาร์ดคาร์บอนของแบตเตอรี่โซเดียมไอออนทำผลงานแข็งแกร่งในเดือนเมษายน โดยการผลิตเพิ่มขึ้นอย่างมีนัยสำคัญเมื่อผู้ประกอบการเร่งขยายกำลังการผลิตเพื่อเติมช่องว่างอุปสงค์-อุปทาน ตามข้อมูล SMM การผลิตแอโนดแบตเตอรี่โซเดียมไอออนเพิ่มขึ้น 32% MoM และ 108% YoY โดยฮาร์ดคาร์บอนซึ่งเป็นวัสดุกระแสหลักมีการเติบโตของการผลิตเด่นชัดเป็นพิเศษ ช่วงหลังมานี้ กำลังการผลิตฮาร์ดคาร์บอนใหม่เริ่มเดินเครื่อง และคาดว่าการเร่งเพิ่มอัตราการเดินเครื่องในระยะถัดไปจะช่วยบรรเทาปัญหาขาดกำลังการผลิตที่เคยจำกัดการพัฒนาแบตเตอรี่โซเดียมไอออน

ก่อนหน้านี้ ฮาร์ดคาร์บอนกลายเป็นคอขวดหลักของการพัฒนาแบตเตอรี่โซเดียมไอออนจากกำลังการผลิตไม่เพียงพอและคุณภาพผลิตภัณฑ์ไม่สม่ำเสมอ ปัจจุบัน อุปสงค์ปลายน้ำกระจุกตัวอยู่ในกลุ่มผู้ผลิตชั้นนำรายใหญ่

โดยภาคกักเก็บพลังงานขนาดใหญ่มีอุปสงค์เติบโตเร็วและกำหนดข้อกำหนดเข้มงวดต่อสมรรถนะฮาร์ดคาร์บอน (อายุการใช้งานรอบยาวและสมรรถนะอุณหภูมิต่ำ) ทำให้ราคาฮาร์ดคาร์บอนสมรรถนะสูงปรับขึ้น อุปสงค์ที่แข็งแกร่งหนุนให้คำสั่งซื้อแสดงเจตนาซื้อฮาร์ดคาร์บอนเพิ่มขึ้นอย่างรวดเร็ว โดยบางบริษัทอยู่ในช่วงเร่งเพิ่มกำลังการผลิตและบางบริษัทวางแผนกำลังการผลิตใหม่ คาดว่าแผนการผลิตฮาร์ดคาร์บอนจะเพิ่มขึ้นต่อในเดือนพฤษภาคม โดยการผลิตเพิ่มขึ้น 16% MoM และ 134% YoY

III. สรุปและแนวโน้มตลาด: อุปสงค์-อุปทานดีขึ้น ไตรมาส 2 เข้าสู่ช่วงเติบโตสำคัญ

โดยรวมแล้ว ตลาดแคโทดและแอโนดของแบตเตอรี่โซเดียมไอออนในเดือนเมษายนแสดงรูปแบบ “อุปสงค์ฟื้นตัว กำลังการผลิตเร่งตัว และความแตกต่างเชิงโครงสร้าง” ฝั่งแคโทด วัสดุโพลีแอนไอออนยังคงครองความเป็นผู้นำอย่างมั่นคง โดย NFPP นำการเติบโต ขณะที่เลเยอร์ออกไซด์ลดลงจากข้อจำกัดด้านความคุ้มค่าต้นทุน-สมรรถนะ ขณะเดียวกัน กำลังการผลิตพรีเคอร์เซอร์ NFPP ที่ไม่เพียงพอและต้นทุนที่สูงขึ้นยังเป็นจุดเจ็บปวดระยะสั้น ฝั่งแอโนด การผลิตฮาร์ดคาร์บอนพุ่งขึ้น กำลังการผลิตใหม่ที่เดินเครื่องช่วยบรรเทาช่องว่างอุปทาน อุปสงค์จากกักเก็บพลังงานขนาดใหญ่หนุนความต้องการสินค้าระดับสูง การขยายกำลังการผลิตที่เร่งตัวช่วยทะลุคอขวด ตอกย้ำความคืบหน้าต่อเนื่องของการพาณิชย์แบตเตอรี่โซเดียมไอออน

คาดว่าไตรมาส 2 จะเป็นช่วงเติบโตสำคัญของอุตสาหกรรม ฝั่งแคโทด ช่วงพีคซีซันมาถึงในเดือนพฤษภาคม โดยการปล่อยกำลังการผลิตเซลล์ใหม่จะหนุนการเติบโตของอุปสงค์ คาดว่า NFPP จะมียอดส่งมอบพุ่งขึ้นเล็กน้อย แต่ควรติดตามอุปทานพรีเคอร์เซอร์และแรงกดดันด้านต้นทุน ฝั่งแอโนด การเร่งเพิ่มกำลังการผลิตฮาร์ดคาร์บอนดำเนินต่อเนื่อง รูปแบบอุปสงค์-อุปทานยังดีขึ้น และการยกระดับสมรรถนะผลิตภัณฑ์กำลังเร่งตัวเพื่อรองรับการใช้งานระดับสูง

ในระยะยาว เมื่อการพาณิชย์แบตเตอรี่โซเดียมไอออนเร่งตัวและฉากทัศน์การใช้งานปลายน้ำขยายต่อเนื่อง อุปสงค์แคโทดและแอโนดจะสนับสนุนการขยายกำลังการผลิตอย่างต่อเนื่อง คาดว่าอุตสาหกรรมจะค่อย ๆ คลี่คลายจุดเจ็บปวดด้านกำลังการผลิตและต้นทุน ปรับโครงสร้างผลิตภัณฑ์ให้เหมาะสม และตอกย้ำสถานะกระแสหลักของแคโทดโพลีแอนไอออนและแอโนดฮาร์ดคาร์บอน ผลักดันอุตสาหกรรมแบตเตอรี่โซเดียมไอออนไปสู่การพัฒนาขนาดใหญ่และคุณภาพสูง