ในปี 2025 ตลาดยานยนต์พลังงานใหม่ (NEV) และระบบกักเก็บพลังงานรูปแบบใหม่ทั่วโลกยังคงเติบโตอย่างแข็งแกร่ง บริษัทแบตเตอรี่ลิเทียมของจีนอาศัยความเชี่ยวชาญด้านเทคโนโลยีและข้อได้เปรียบด้านขนาด ยังคงครองห่วงโซ่อุปทานระดับโลก เมื่อเร็วๆ นี้ บริษัทแบตเตอรี่ลิเทียมจดทะเบียนของจีนได้เผยแพร่รายงานประจำปี 2025 อย่างต่อเนื่อง จากการรวบรวมข้อมูลสาธารณะ รายงานฉบับนี้วิเคราะห์การผลิต การจัดส่ง และยอดขายของอุตสาหกรรมแบตเตอรี่ลิเทียมของจีนตลอดปี 2025 เพื่อให้ข้อมูลเชิงลึกเกี่ยวกับแนวโน้มการพัฒนาของอุตสาหกรรม

การวิเคราะห์นี้คัดเลือกบริษัทจดทะเบียนที่เปิดเผยข้อมูลการผลิตและยอดขายเซลล์แบตเตอรี่โดยเฉพาะ ได้แก่ CATL, EVE, Gotion High-tech, Sunwoda, REPT Battero และ Zenergy ในด้านหนึ่ง บริษัทเหล่านี้เป็นตัวแทนของอุตสาหกรรมอย่างสูง ครอบคลุมตั้งแต่ผู้นำสูงสุดไปจนถึงผู้เล่นหน้าใหม่ที่แข็งแกร่ง อีกด้านหนึ่ง ช่วงเวลานี้เป็นช่วงที่บริษัทจดทะเบียนเผยแพร่รายงานประจำปี 2025 และรายงานไตรมาส 1/2026 อย่างเข้มข้น ทำให้ข้อมูลของบริษัทเหล่านี้มีความทันสมัยและน่าเชื่อถือที่สุด สะท้อนสถานะปัจจุบันของอุตสาหกรรมได้อย่างแม่นยำ นอกจากนี้ บริษัทแบตเตอรี่ลิเทียมจดทะเบียนอื่นๆ บางแห่งเปิดเผยเฉพาะตัวเลขรายได้ในรายงานประจำปีโดยไม่ได้เผยแพร่ข้อมูลการผลิตและยอดขายเชิงกายภาพในหน่วยกำลังการผลิต (GWh) หรือพลังงาน (Ah) เพื่อให้มั่นใจในความถูกต้องและความสามารถในการเปรียบเทียบของมิติข้อมูลในรายงาน เราจึงคัดเลือกเฉพาะบริษัทที่เปิดเผยข้อมูลกำลังการผลิตและยอดขายอย่างโปร่งใส

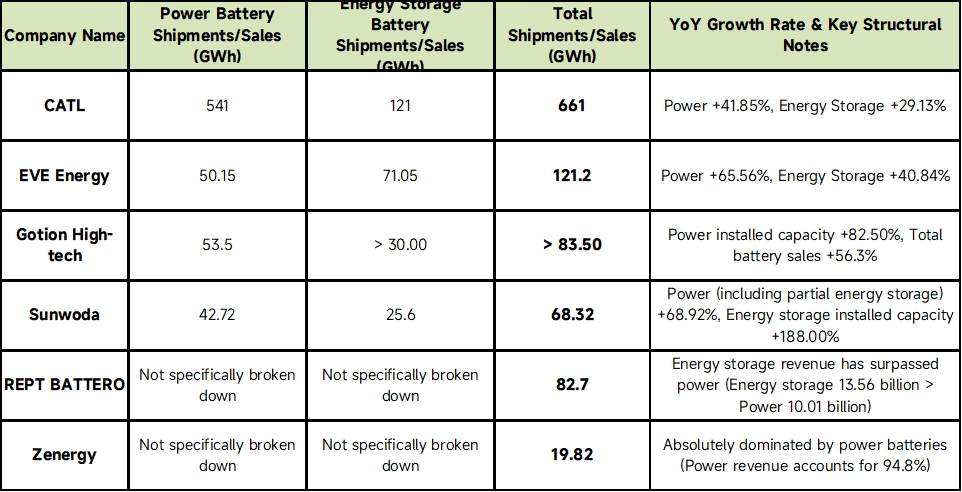

I. ภาพรวมข้อมูลการผลิตและยอดขายปี 2025 ของบริษัทแบตเตอรี่ลิเทียมหลัก

ข้อมูลต่อไปนี้รวบรวมจากรายงานประจำปีที่เผยแพร่ของแต่ละบริษัท:

(แหล่งข้อมูล: รายงานประจำปีของบริษัทที่เกี่ยวข้อง)

(หมายเหตุ: REPT Battero และ Zenergy ไม่ได้แยกรายละเอียดปริมาณเชิงกายภาพของ EV และ ESS ในหน่วย GWh ในรายงานประจำปี แต่สามารถระบุจุดเน้นเชิงกลยุทธ์ที่แตกต่างกันอย่างชัดเจนจากยอดขายรวมและโครงสร้างรายได้)

II. สรุปอุตสาหกรรมและแนวโน้มในอนาคต

จากข้อมูลรายงานประจำปีข้างต้นและบริบทมหภาคปัจจุบันของอุตสาหกรรมแบตเตอรี่ลิเทียมของจีน สามารถระบุแนวโน้มการพัฒนาตลาดสำหรับปี 2025 และต่อไปได้ดังนี้:

1 ยอดขายและการผลิตแข็งแกร่ง ระบบกักเก็บพลังงานกลายเป็นสนามรบหลักคู่ขนาน

ในปี 2025 ข้อมูลการผลิตและยอดขายของบริษัทแบตเตอรี่ลิเทียมกระแสหลักของจีนล้วนแสดงการเติบโต YoY สูงระดับสองหลักหรือแม้แต่สามหลัก (เช่น แบตเตอรี่กำลังของ Gotion High-tech +82.5%, ระบบกักเก็บพลังงานของ Sunwoda +188%) โดยรวม โครงสร้าง "เครื่องยนต์คู่" ของอุตสาหกรรมได้เป็นรูปเป็นร่างอย่างสมบูรณ์: NEV เป็นฐานหลัก ขณะที่แบตเตอรี่ ESS ได้เปลี่ยนจาก "ธุรกิจเสริม" เป็นเสาหลักธุรกิจหลักของหลายบริษัท (เช่น EVE, REPT Battero) ปริมาณการผลิตสูงกว่ายอดขายเล็กน้อยในทุกบริษัท รักษาสถานะการหมุนเวียนสินค้าคงคลังที่ดี สะท้อนความเชื่อมั่นอย่างแข็งแกร่งต่ออุปสงค์ในอนาคต

2 การพัฒนาเทคโนโลยี: ความจุขนาดใหญ่และอัตราการชาร์จสูงกลายเป็นกระแสหลัก

เบื้องหลังการเติบโตอย่างก้าวกระโดดของการผลิตและยอดขาย การพัฒนาเทคโนโลยีเป็นตัวขับเคลื่อนหลัก

แบตเตอรี่กำลัง: แบตเตอรี่ชาร์จเร็วอัตรา C สูง (เช่น ชาร์จเร็วพิเศษ 4C/5C) โซลูชันความหนาแน่นพลังงานสูง และแบตเตอรี่เฉพาะสำหรับรถ PHEV/รถยนต์ขยายระยะทางกำลังเติบโต ขณะเดียวกัน บริษัทต่างๆ กำลังเร่งพัฒนาเทคโนโลยีแบตเตอรี่กึ่งโซลิดสเตต/โซลิดสเตตทั้งหมดและเทคโนโลยีแนวหน้าอื่นๆ

แบตเตอรี่ ESS: ความจุเซลล์แบตเตอรี่กำลังพัฒนาไปสู่ขนาดที่ใหญ่ขึ้น (เช่น 314Ah, 588Ah หรือสูงกว่า) มุ่งสู่อายุการใช้งานที่ยาวนานขึ้น (มากกว่า 15,000 รอบ) และประสิทธิภาพพลังงานระบบที่สูงขึ้น เพื่อลดต้นทุนพลังงานเฉลี่ย (LCOE) ตลอดวงจรชีวิต

3 การแข่งขันด้านราคาและตลาดรุนแรงขึ้น: ใช้ปริมาณชดเชยราคา ลดต้นทุนด้วยขนาด

แม้บริษัทข้างต้นจะมีการเติบโตอย่างระเบิดในปริมาณการผลิตและยอดขาย แต่อุตสาหกรรมโดยรวมเผชิญ "สงครามราคา" ที่รุนแรงและแรงกดดันในการลดต้นทุน หลังจากราคาลิเทียมคาร์บอเนตและวัตถุดิบต้นน้ำอื่นๆ ปรับตัวลง ราคาเซลล์แบตเตอรี่ต่อวัตต์-ชั่วโมงในปี 2025 อยู่ในระดับต่ำสุดเป็นประวัติการณ์ ภายใต้บริบทนี้ ตรรกะการอยู่รอดหลักของบริษัทได้เปลี่ยนเป็น "ใช้ปริมาณชดเชยราคา" และ "ลดต้นทุนด้วยขนาด" ยักษ์ใหญ่อย่าง CATL รักษาอัตรากำไรผ่านข้อได้เปรียบด้านห่วงโซ่อุปทาน ขณะที่บริษัทอื่นๆ ชดเชยความเสี่ยงจากราคาที่ลดลงด้วยอัตราการเติบโตของการจัดส่งที่มากกว่า 50%

![[แบตเตอรี่ลิเธียม: CATL และ Octopus Energy จะจัดตั้งกิจการร่วมค้า]](https://imgqn.smm.cn/usercenter/olwlF20251217171731.jpg)