Around April 23, 2026, import and export data for cobalt and lithium battery industry chain products in March were released in bulk. Data showed that March spodumene imports rebounded significantly from February, hitting a new record high of 837,400 mt in physical content. Lithium carbonate side, China imported 29,974 mt of lithium carbonate in March, up 13% MoM and up 65% YoY...SMM compiled the import and export data for battery materials as follows:

Upstream

Lithium Concentrates

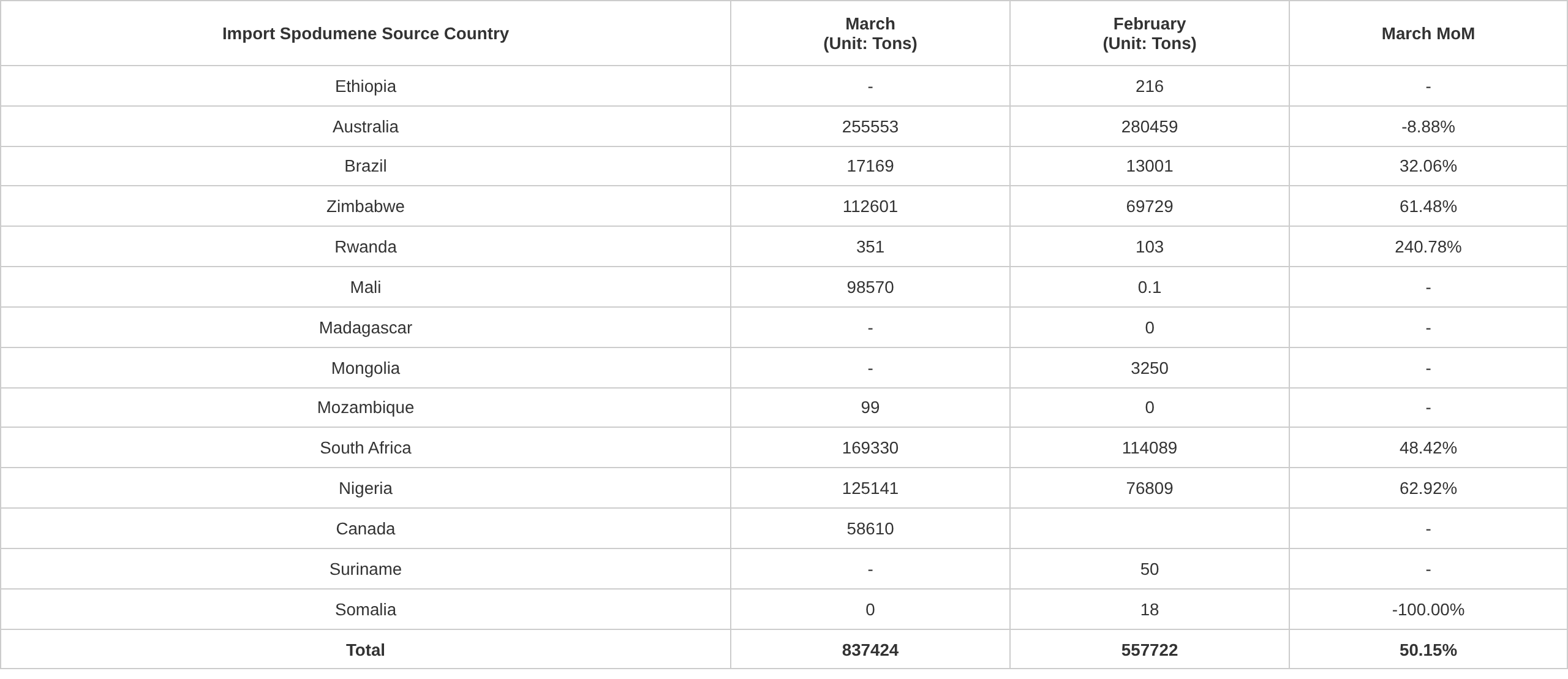

Customs data showed that March spodumene imports rebounded significantly from February, hitting a new record high of 837,400 mt in physical content. By source country: African ore arrivals increased notably — Nigeria imports reached 125,100 mt, up 63% MoM; Zimbabwe shipments from earlier periods arrived at ports in the month totaling 112,600 mt, up 61% MoM; Canada broke the zero-import streak of January–February with 58,600 mt arriving in March; while Australian ore arrivals declined MoM due to shipping schedule impacts.

According to SMM's screening analysis, total port arrivals for the month were equivalent to 81,000 mt LCE. Lithium concentrates accounted for 72% of the month's imports, down slightly compared to the same period last year, mainly due to a notable increase in South African raw ore port arrivals recently. Notably, driven by prices and local beneficiation plant development, Nigerian ore arrivals surged, with not only raw ore volumes rising significantly but also concentrates share increasing notably YoY.

Source: China Customs, compiled by SMM

Spodumene concentrates (CIF China) spot pricing side, according to SMM spot quotes, March spodumene concentrates (CIF China) spot prices showed a V-shaped trend, dropping to a low of $2,028/mt at month-end before rebounding to $2,313/mt at month-end, with a monthly average of $2,081.4/mt.

According to SMM, in March, spodumene and lepidolite profit trends diverged, with notable structural cost differences among lithium chemicals enterprises. Available spodumene volumes were tight, ore traders held back from selling, and inventory continued to be drawn down. Enterprises purchasing spodumene externally suffered losses on spot margins throughout the month, and non-integrated enterprises faced increasing difficulties in hedging and procurement.

Entering April, spodumene concentrates (CIF China) spot prices also showed a pattern of initial decline followed by recovery. Recently, spodumene concentrates prices continued to probe higher. As of April 27, spodumene concentrates (CIF China) spot prices rose to $2,507/mt, up $194/mt from $2,313/mt at end-March, an increase of 8.39%.

According to recent SMM research, driven by market expectations of improving future demand, speculative sentiment in the lithium carbonate futures market remained strong, pushing futures prices up. Lithium ore merchants showed increased willingness to sell, with pricing-against-futures prices staying high.Looking ahead, lithium chemical plant operating rates stay high, and demand for lithium ore continues to climb. Meanwhile, Zimbabwe has suspended spodumene exports for nearly two months, leading to persistently tight available-for-sale lithium ore in the market. Overall, spodumene prices are expected to hold up well.

Lithium Carbonate

According to customs data, China's lithium carbonate imports in March totaled 29,974 mt, up 13% MoM and up 65% YoY. Of this, imports from Chile were 18,000 mt (61% of total imports), Argentina 8,292 mt (28%), and Indonesia 2,100 mt (7%). Cumulative lithium carbonate imports from January to March reached 83,000 mt, up 65% YoY.

China exported 448 mt of lithium carbonate in March, down 25% MoM and up 104% YoY. Cumulative exports from January to March totaled 1,516 mt, up 46% YoY.

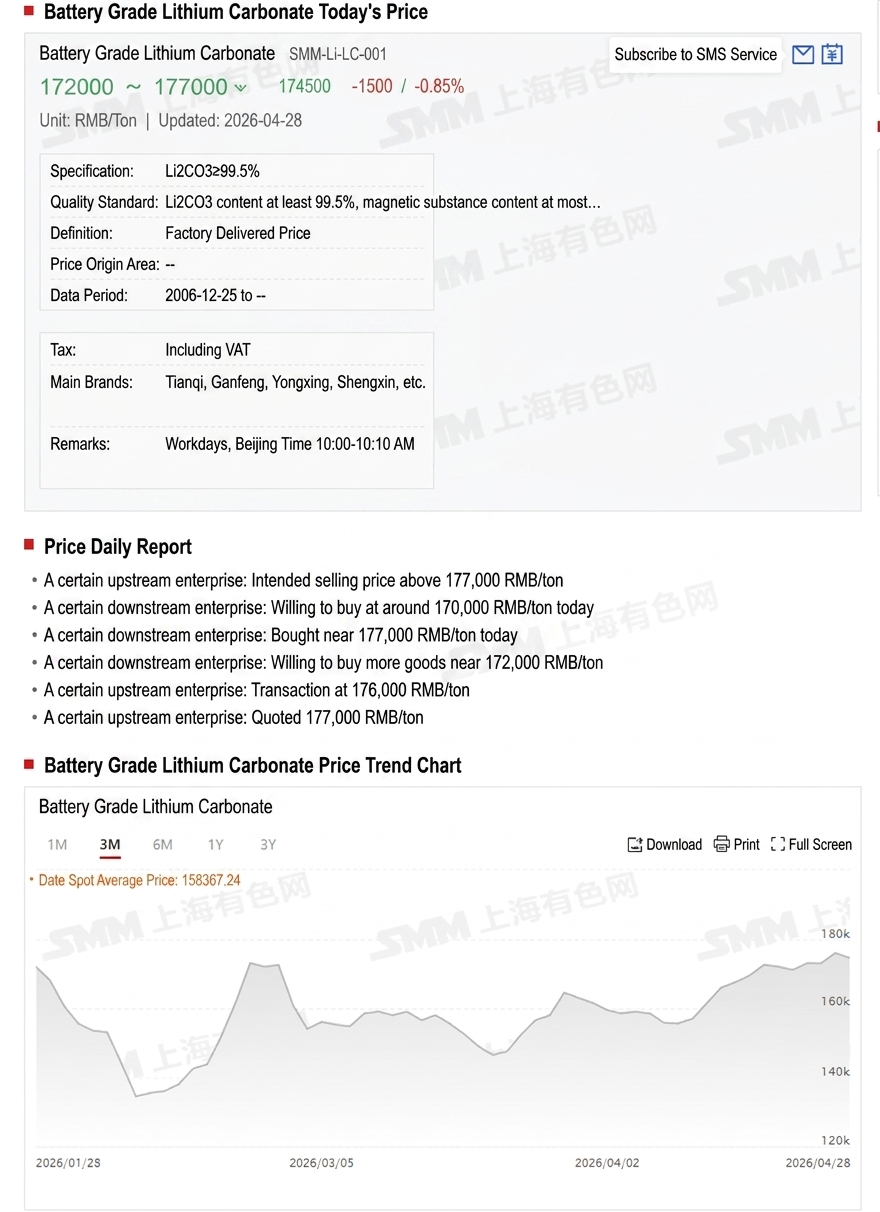

According to SMM spot quotes, lithium carbonate showed a volatile trend of first declining then rising in March. As of March 31, the average spot price of battery-grade lithium carbonate was 163,000 yuan/mt, with a monthly average price of 156,700 yuan/mt.

According to SMM analysis, spot lithium carbonate prices in China showed a significantly volatile upward trend in March, with the monthly average price up 5% MoM. Fundamentals side, supply-side production gradually recovered as maintenance ended, and lithium chemical plants showed increased willingness to sell spot orders at the relatively high level of around 170,000 yuan/mt; demand-side, downstream cathode material producers basically adopted a dip-buying strategy, with strong purchase willingness at around 140,000 to 150,000 yuan/mt. As demand continued to improve, some enterprises restocked heavily at low prices. In March, battery-grade lithium carbonate spot prices rose to 172,500 yuan/mt at the beginning of the month and pulled back to around 163,000 yuan/mt at month-end.

Recently, battery-grade lithium carbonate spot quotes have stayed high above 170,000 yuan/mt. As of April 28, battery-grade lithium carbonate spot quotes were at 172,000-177,000 yuan/mt, with an average price of 174,500 yuan/mt.

Lithium Hydroxide

According to customs data, in March 2026, China imported 6,111 mt of lithium hydroxide, up 66% MoM and up 200% YoY. Of this, 2,927 mt came from Indonesia, accounting for approximately 48% of imports, with another 40% from Australia and South Korea. China exported 3,143 mt of lithium hydroxide in March, up 20% MoM and down 26% YoY, of which 2,059 mt went to South Korea and 278 mt to Japan.

Battery Materials

Ternary Cathode Material

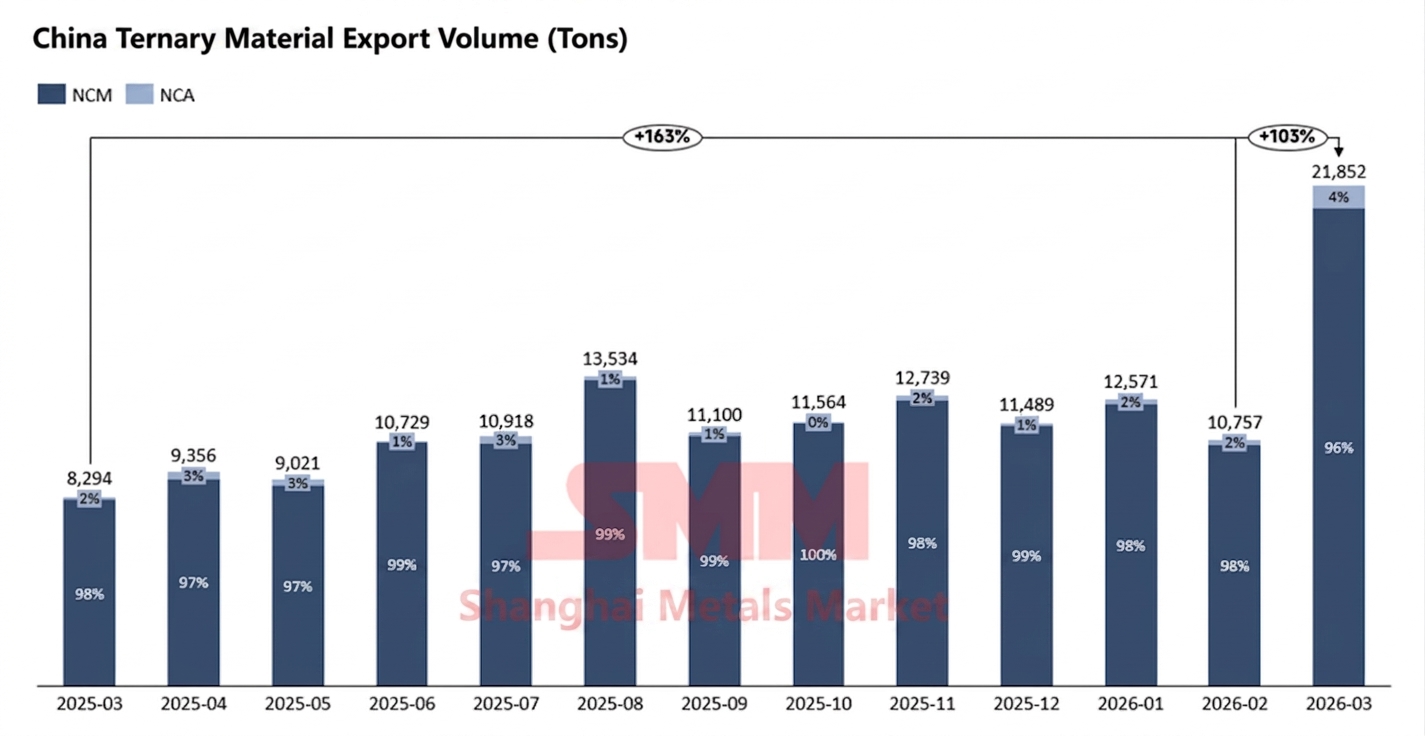

In March 2026, China's ternary cathode material (NCM and NCA combined) exports reached 21,900 mt, up 103% MoM and up 163% YoY. Of this, NCM exports were 20,900 mt, accounting for 96%.

In terms of export destinations, South Korea was the largest NCM importer with 8,500 mt in March; Poland, Malaysia, and Japan ranked second, third, and fourth with 3,720 mt, 2,409 mt, and 2,363 mt respectively. Additionally, Germany's imports saw significant growth compared to the same period last year.

China's ternary cathode material exports hit a record high in March, mainly driven by the cancellation of the 13% export VAT rebate policy effective April 1. Four leading battery cell manufacturers in Japan and South Korea placed orders in advance, boosting demand not only for their domestic plants but also for their battery cell production sites in Southeast Asia and Europe. Beyond the rebate policy impact, EV subsidy policies in Europe also contributed to strong demand growth, increasing China's ternary cathode material exports. Among them, Northern Europe led in EV penetration rate with the largest subsidies; the UK, France, and Germany continued to serve as key sources of NEV sales support. In contrast, US NEV sales declined notably in Q1, down nearly 30% YoY, significantly impacting Q1 orders for some ex-China battery cell manufacturers targeting the North American market.

Looking ahead to Q2, Europe is expected to remain the largest source of ex-China ternary cathode material demand growth. Despite some disruption from the rebate policy change, as more battery cell manufacturers and ternary cathode material producers plan to complete construction and commence production this year and next, the outlook for European market demand remains optimistic.

LiPF6

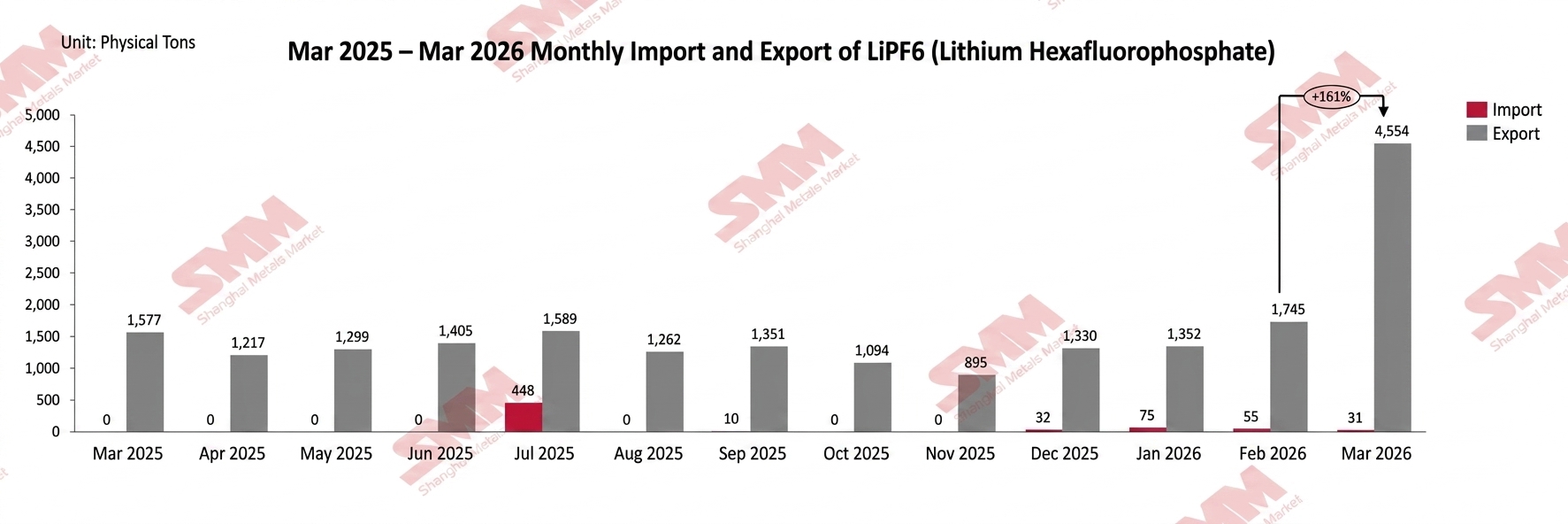

According to China Customs data, in March 2026, China's cumulative LiPF6 exports were approximately 4,554 mt, up approximately 161% MoM, while cumulative imports were approximately 31 mt.

Export side, China's LiPF6 exports in March 2026 were approximately 4,554 mt, up approximately 161% MoM from February and up approximately 188.8% YoY. Specifically, as the LiPF6 export VAT rebate policy was officially cancelled effective April 1, 2026, enterprises rushed to export in March, resulting in MoM increases in exports to multiple major destination countries. Exports to Poland were 1,723.602 mt, up approximately 693.63% MoM; exports to South Korea were 1,099.429 mt, up approximately 184.26% MoM; exports to Czech Republic were 460.5 mt, up approximately 237.36% MoM; exports to Malaysia were 249.346 mt, up approximately 141.39% MoM. However, exports to the US declined in volume — exports to the US were 266.146 mt, down approximately 53.70% MoM.

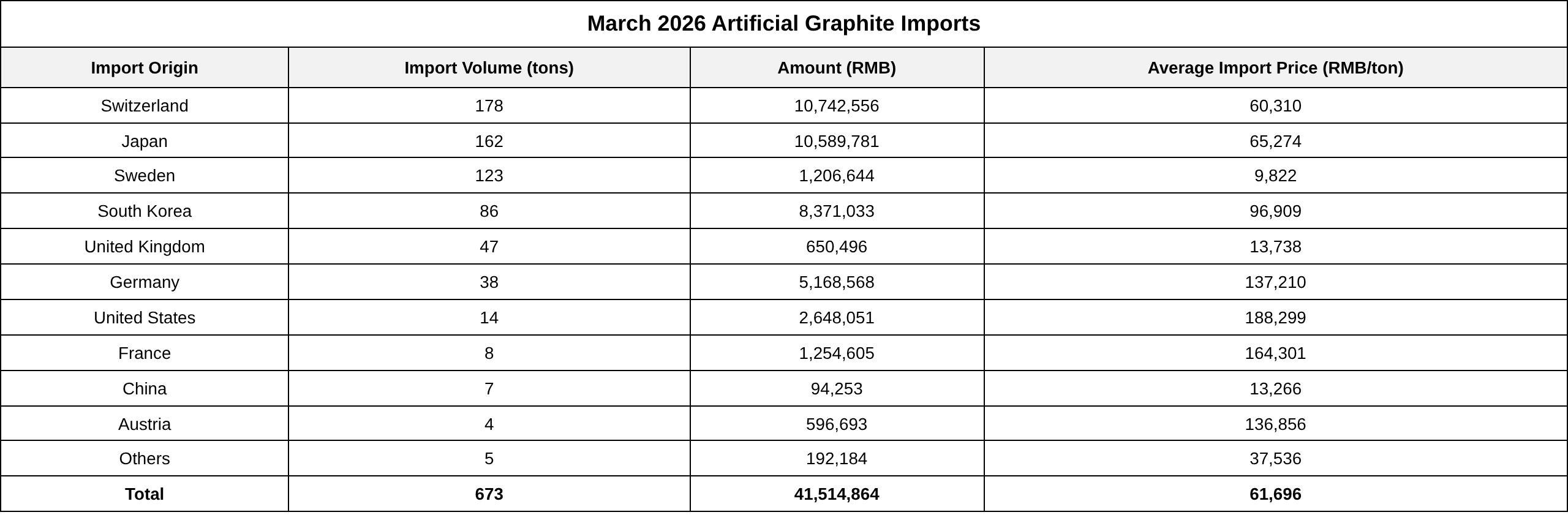

Artificial Graphite

In March 2026, China's artificial graphite imports were 673 mt, up 0.6% MoM and down 34.1% YoY. In terms of average import price, in March 2026, China's artificial graphite average import price was 61,696 yuan/mt, up 3.9% MoM and up 10.6% YoY.

Data source: China Customs, SMM

In March 2026, China's artificial graphite exports were 37,525 mt, up 6% MoM and down 16% YoY. In terms of average export price, in March 2026, China's artificial graphite average export price was 9,866 yuan/mt, up 14.4% MoM and down 7% YoY.

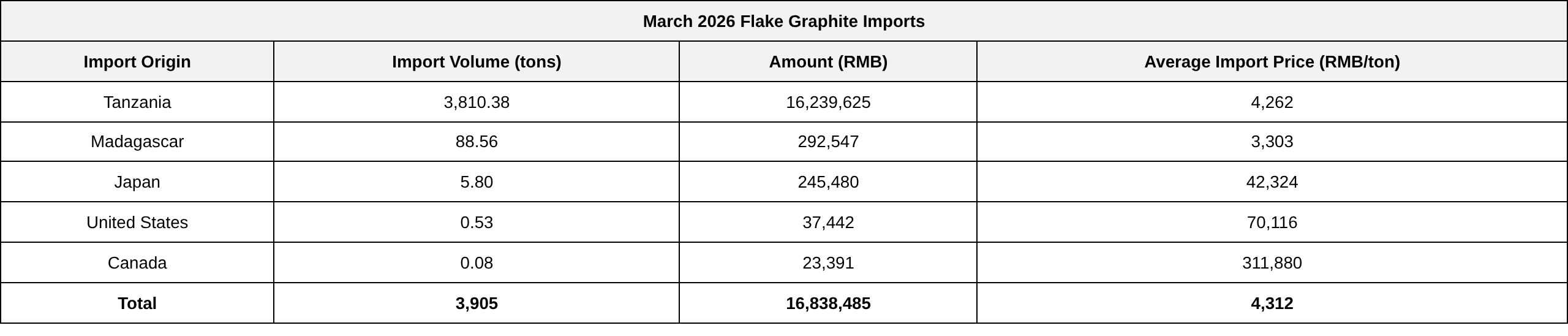

Flake Graphite

In March 2026, China's flake graphite imports were 3,905 mt, up 11% MoM and up 45% YoY.

Data source: China Customs, SMM

In March 2026, China's flake graphite exports were 8,118 mt, up 35% MoM and up 65% YoY.

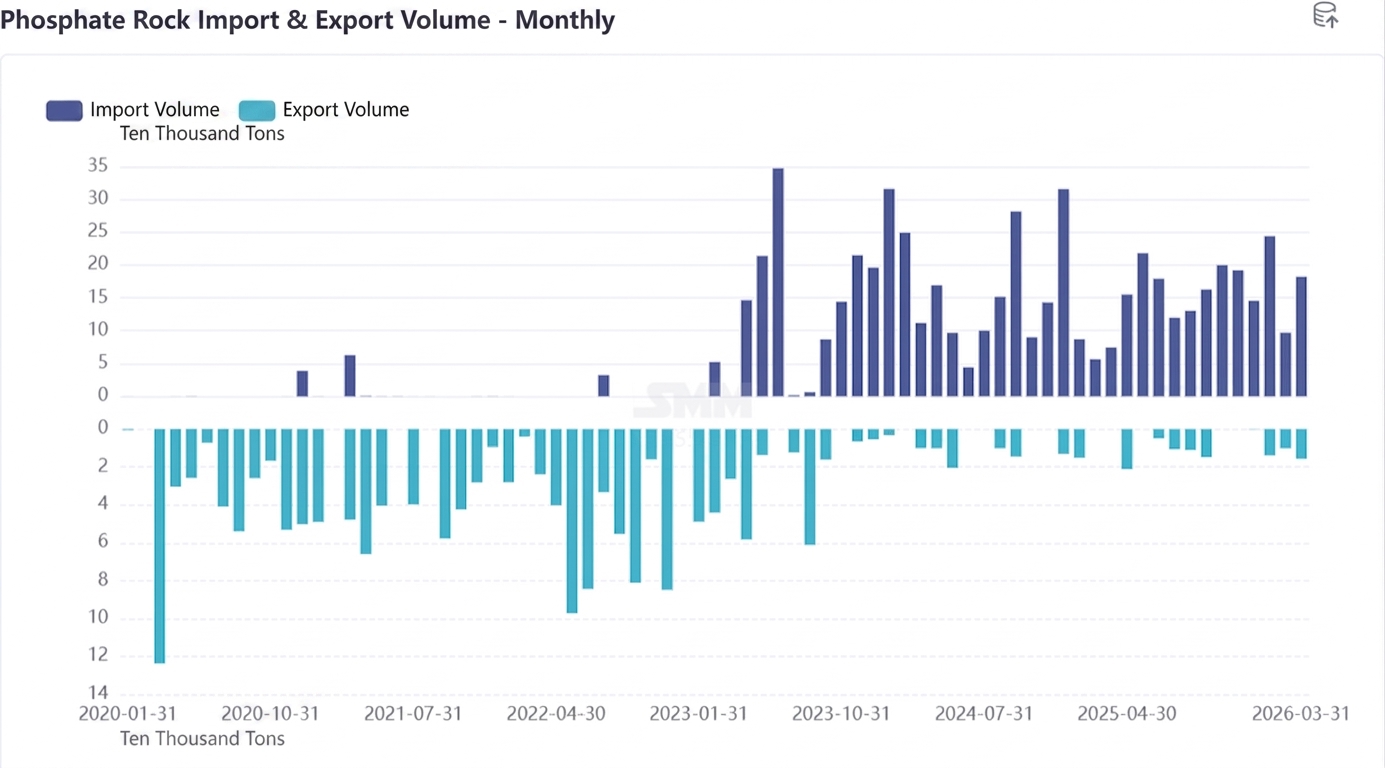

Phosphate Ore

According to customs data, in March 2026, China's phosphate ore imports were 182,000 mt. March imports were up 88.2% MoM from February's 97,000 mt, and up 144.4% YoY from 75,000 mt in the same period last year; March total import value was $14.552 million, up 74.6% MoM from February's $8.336 million. Unit price was $79.9/mt, down 7.2% significantly from February's $86.1/mt.

In March, China's phosphate ore imports mainly came from Egypt and Pakistan, with imports of 170,000 mt and 12,000 mt respectively. Affected by factors related to the Strait of Hormuz, Jordanian phosphate ore failed to be imported, though imports from other regions had filled the gap. Due to hindered transportation of high-priced Jordanian phosphate ore and lack of import volume support, the March phosphate ore import unit price declined from February, pulling back to below $80/mt.

Cobalt

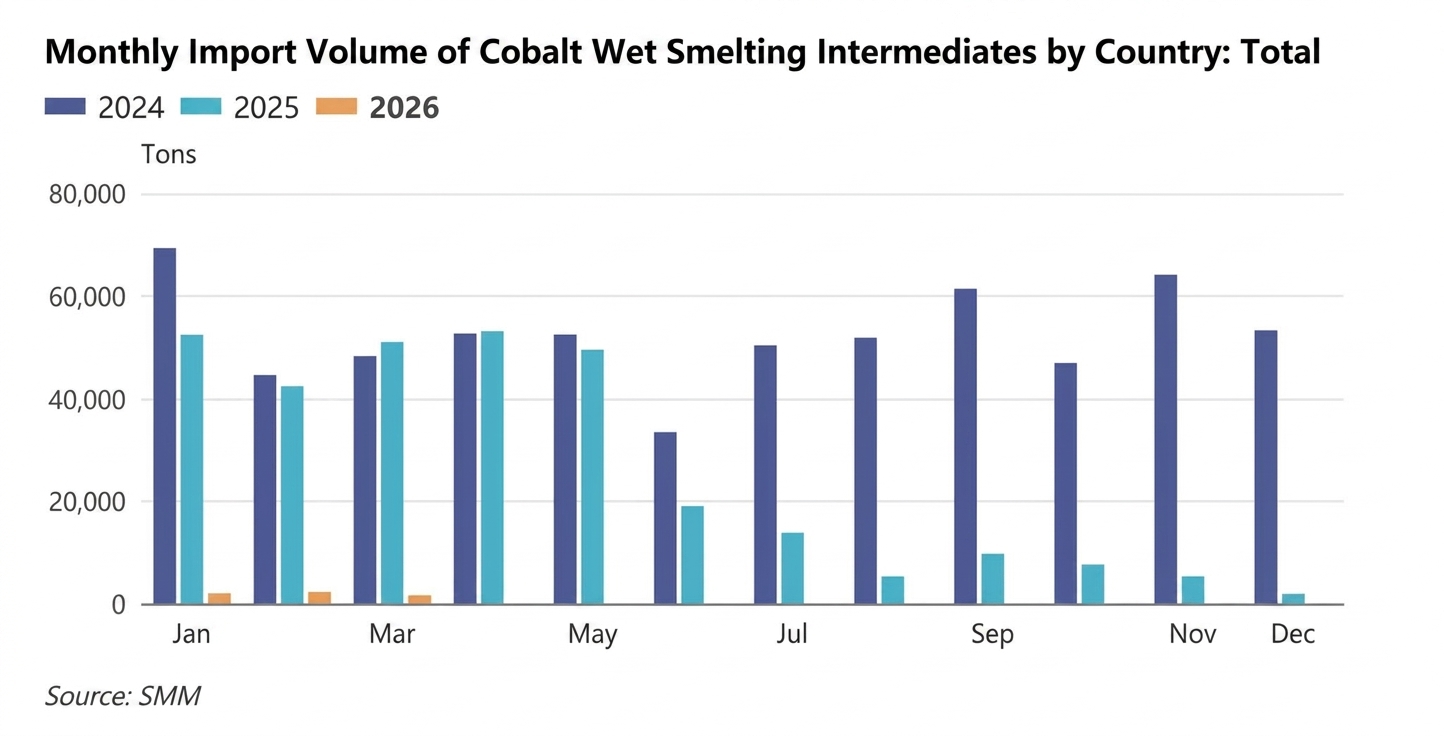

Cobalt Hydrometallurgy Intermediate Products

In March 2026, China's cobalt hydrometallurgy intermediate products imports were approximately 1,690 mt in physical content, down 26% MoM and down 97% YoY, of which imports from DRC were approximately 1,668 mt in physical content, up 10% MoM and down 97% YoY. In March 2026, China's average import price of cobalt hydrometallurgy intermediate products was $16,730/mt in physical content, up 2.92% MoM. It was learned that the volume of cobalt intermediate products exported from the DRC increased significantly in March. If the government maintains this efficient approval pace going forward, the quotas for Q4 2025 and Q1/Q2 2026 will most likely be exported within the stipulated timeframe, reducing the probability of further delays. However, shipping in Africa is currently tight, with only a few miners completing small-batch vessel bookings in April. Based on a 1-2 month shipping time from South Africa to China, this batch of intermediate products is expected to arrive at port in May-June, while intermediate products from other miners are not expected to arrive until around July.

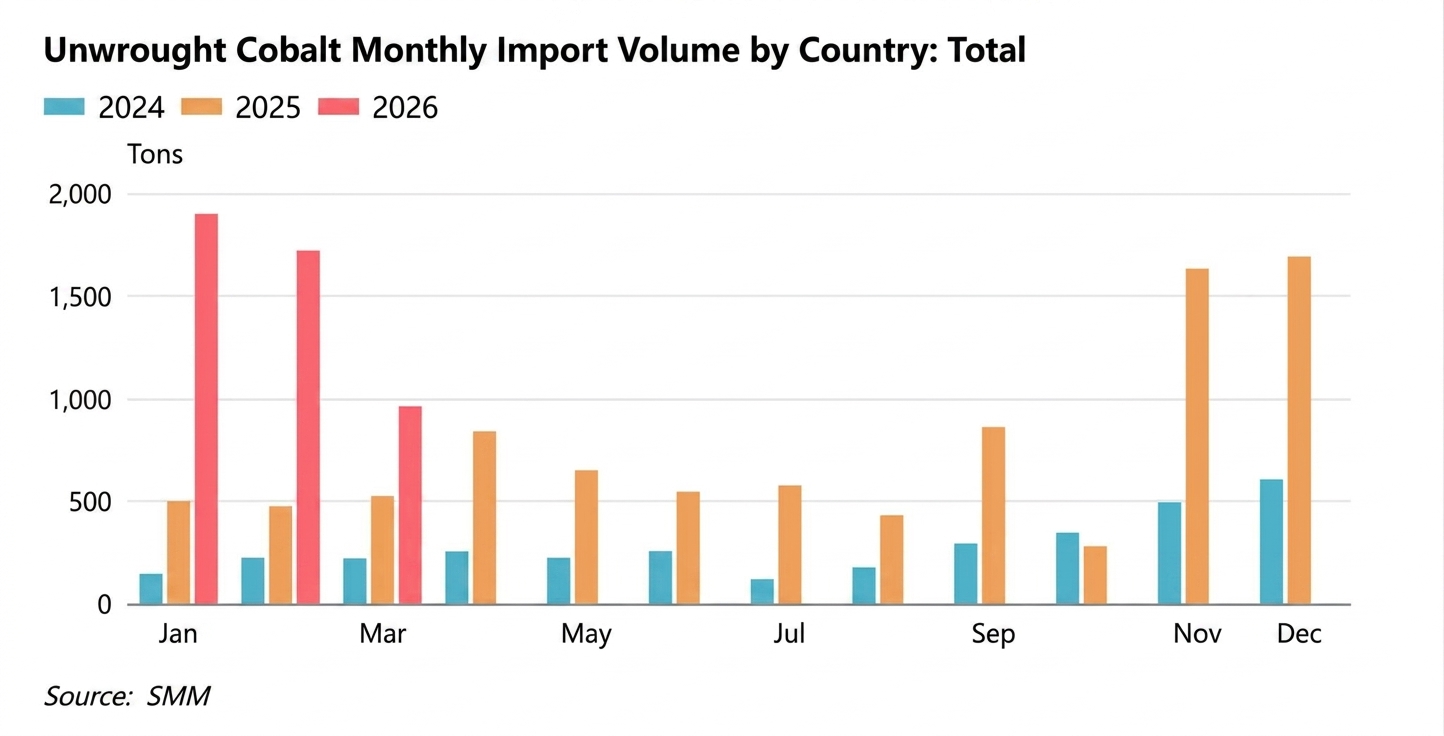

Unwrought Cobalt

In March 2026, China's unwrought cobalt imports were approximately 961 mt, down 44% MoM and up 83% YoY. March imports remained at a relatively high level, mainly because export orders placed during the import window opening from late December 2025 to mid-January 2026 continued to arrive at port. In terms of average import price, China's average import price of unwrought cobalt in March 2026 was $50,346/mt, up 10% MoM. Cumulative imports from January to March 2026 totaled 4,582 mt, up 206% YoY cumulatively. It was learned that as the import window gradually closed after mid-to-late January 2026, overseas traders' willingness to export weakened, and refined cobalt imports in April may continue to decline MoM.

Export side, China's unwrought cobalt exports in March 2026 were approximately 413 mt, up 32% MoM and down 69% YoY. By country, China's exports to the US edged up, with March exports to the US at 280 mt, up 13% MoM. In terms of average export price, China's average export price of unwrought cobalt in March 2026 was $51,596/mt, down 3% MoM. Cumulative exports from January to March 2026 totaled 1,574 mt, down 52% YoY cumulatively.