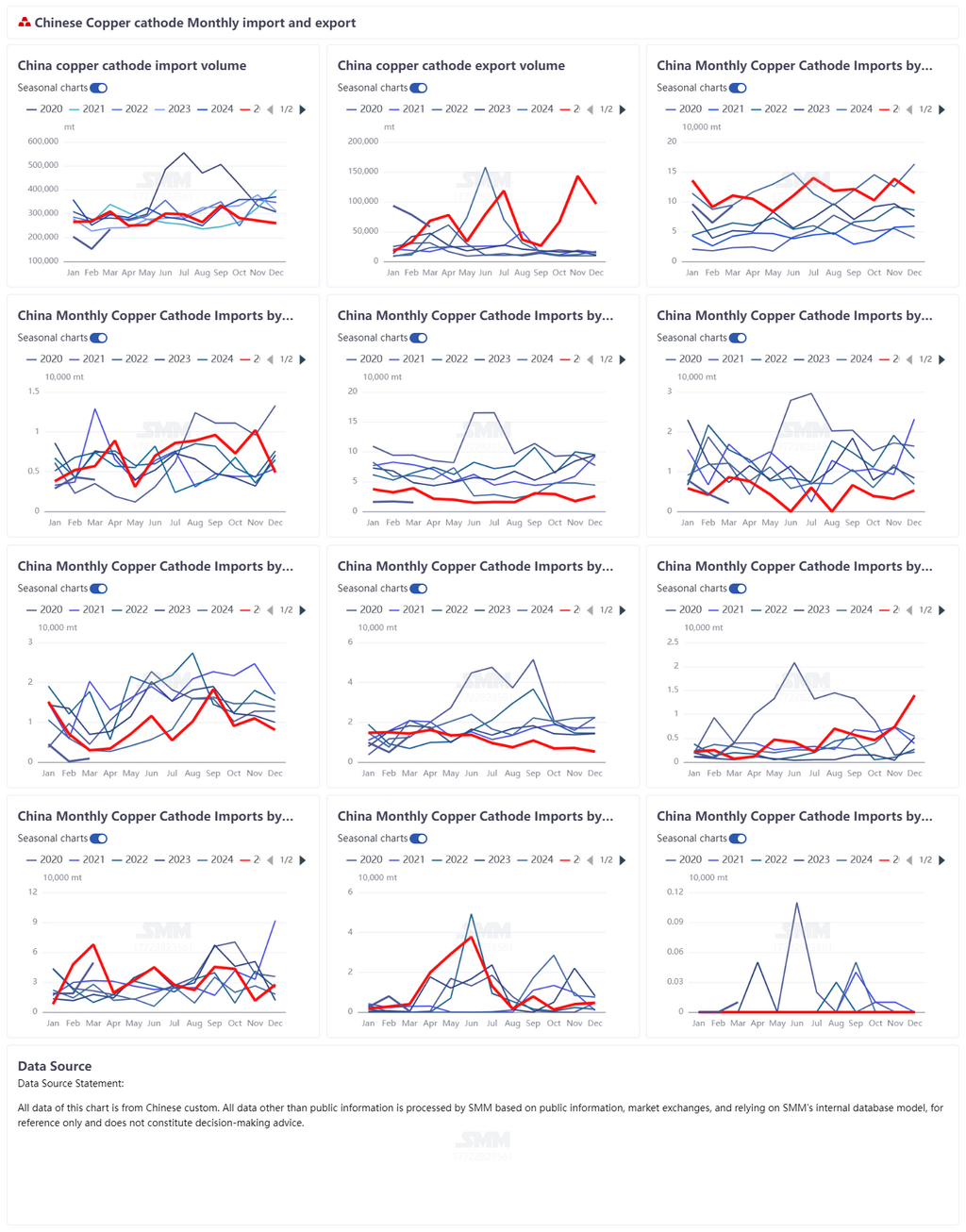

ในเดือนมีนาคม 2569 การนำเข้าทองแดงบริสุทธิ์ของจีนอยู่ที่ 234,600 ตัน เพิ่มขึ้น 53.33% เมื่อเทียบรายเดือน แต่ลดลง 24.03% เมื่อเทียบรายปี ด้านการส่งออกอยู่ที่ 58,200 ตัน ลดลง 25.60% เมื่อเทียบรายเดือน และ 14.40% เมื่อเทียบรายปี จากตัวเลขดังกล่าว การนำเข้าทองแดงบริสุทธิ์สุทธิของจีนในเดือนมีนาคมอยู่ที่ประมาณ 176,400 ตัน แม้การนำเข้าจะฟื้นตัวอย่างเห็นได้ชัดเมื่อเทียบรายเดือนในเดือนมีนาคม แต่การนำเข้าสุทธิยังคงอยู่ในระดับค่อนข้างต่ำเมื่อเทียบรายปี บ่งชี้ว่าการเสริมอุปทานทองแดงบริสุทธิ์จากต่างประเทศเข้าสู่จีนยังคงไม่เพียงพอ และความคาดหวังเรื่องอุปทานตึงตัวยังไม่ได้คลี่คลายอย่างมีนัยสำคัญ

เมื่อพิจารณาตามแหล่งนำเข้า การนำเข้าทองแดงบริสุทธิ์ของจีนในเดือนมีนาคมยังคงกระจุกตัวอยู่ในสาธารณรัฐประชาธิปไตยคองโก รัสเซีย ญี่ปุ่น ชิลี และคาซัคสถาน โดยการนำเข้าจากสาธารณรัฐประชาธิปไตยคองโกอยู่ที่ 93,100 ตัน คิดเป็น 39.69% ของทั้งหมด และยังคงเป็นแหล่งนำเข้าทองแดงบริสุทธิ์ที่สำคัญที่สุดของจีน ปัญหาด้านโลจิสติกส์ในแอฟริกายังคงดำเนินอยู่ โดยเฉพาะอย่างยิ่ง ประสิทธิภาพการขนส่ง การผ่านพิธีการศุลกากรข้ามแดน และตารางการขนส่งทางท่าเรือในสาธารณรัฐประชาธิปไตยคองโกและพื้นที่โดยรอบยังคงไม่มีเสถียรภาพ ตลาดยังคงกังวลเกี่ยวกับจังหวะการมาถึงของสินค้าจากแอฟริกา หากปัญหาด้านโลจิสติกส์เหล่านี้ยังคงทวีความรุนแรงขึ้น ผลกระทบต่ออุปทานทองแดงบริสุทธิ์ของจีนอาจยืดเยื้อไปจนถึงเดือนพฤษภาคม และความคาดหวังเรื่องอุปทานตึงตัวอาจแข็งแกร่งขึ้นอีก

ในด้านการส่งออก การส่งออกทองแดงบริสุทธิ์ของจีนในเดือนมีนาคมอยู่ที่ 58,200 ตัน ในแง่ของปลายทาง ไต้หวัน เวียดนาม และไทยยังคงเป็นตลาดส่งออกหลัก เป็นที่น่าสังเกตว่า เนื่องจากหน้าต่างการส่งออกค่อยๆ ปิดลงเมื่อเร็วๆ นี้ ตลาดคาดการณ์โดยทั่วไปว่าการส่งออกทองแดงบริสุทธิ์จะลดลงในช่วงเดือนเมษายนถึงมิถุนายน โดยปริมาณที่เคยไหลเข้าสู่ตลาดต่างประเทศคาดว่าจะหดตัวลงอย่างมาก ในทำนองเดียวกัน ปริมาณส่งมอบใน LME อาจลดลงเช่นกัน ทำให้ความคาดหวังต่อการเติบโตของสต็อกที่มองเห็นได้ในต่างประเทศอ่อนแอลง อย่างไรก็ตาม ยังคงต้องจับตาการเปลี่ยนแปลงของส่วนต่างราคา LME-COMEX อย่างใกล้ชิด หากส่วนต่างขยายกว้างขึ้นอีกครั้ง อาจเปลี่ยนแปลงกระแสการไหลเวียนและรูปแบบการส่งมอบทองแดงทั่วโลกอีกครั้ง สร้างความปั่นป่วนใหม่ต่อพฤติกรรมการส่งออก

นอกจากนี้ ความตึงเครียดที่ทวีความรุนแรงขึ้นในตะวันออกกลางเมื่อเร็วๆ นี้กำลังส่งผลกระทบต่อห่วงโซ่อุปทานทองแดงผ่านตลาดการขนส่งทางเรือระหว่างประเทศ ในด้านหนึ่ง ต้นทุนค่าระวางเรือระหว่างประเทศปรับตัวสูงขึ้น ผลักดันอัตราค่าขนส่งทางไกลโดยรวมให้เพิ่มขึ้น อีกด้านหนึ่ง การเปลี่ยนเส้นทางเดินเรือ ความล่าช้าในการขนส่ง และต้นทุนประกันภัยในภูมิภาคที่สูงขึ้น ยังทำให้โลจิสติกส์การค้าทองแดงทั่วโลกขาดเสถียรภาพมากขึ้น สำหรับตลาดจีนซึ่งพึ่งพาการเสริมอุปทานจากต่างประเทศ ปัญหาโลจิสติกส์ในแอฟริกาที่ยังคงดำเนินอยู่ ประกอบกับการหยุดชะงักทางทะเลจากความตึงเครียดในตะวันออกกลาง อาจยังคงสร้างความผันผวนซ้ำแล้วซ้ำเล่าต่อจังหวะการมาถึงของทองแดงบริสุทธิ์นำเข้า ตลาดจึงจำเป็นต้องติดตามผลกระทบที่แท้จริงของโลจิสติกส์ต่อการส่งมอบอุปทานอย่างใกล้ชิด

โดยรวมแล้ว แม้การนำเข้าทองแดงบริสุทธิ์ของจีนจะฟื้นตัวเมื่อเทียบรายเดือนในเดือนมีนาคม แต่การนำเข้าสุทธิยังคงต่ำกว่าเมื่อเทียบรายปี แสดงให้เห็นว่าการเสริมอุปทานในประเทศจากต่างประเทศยังคงจำกัด ในขณะเดียวกัน ความคาดหวังเรื่องการส่งออกที่อ่อนแอลงในช่วงเดือนเมษายนถึงมิถุนายน การหยุดชะงักของการขนส่งทางเรือจากความตึงเครียดในตะวันออกกลาง และปัญหาโลจิสติกส์ในแอฟริกาที่ยังคงดำเนินอยู่ ล้วนเสริมความไม่แน่นอนต่ออุปทานทองแดงบริสุทธิ์ในช่วงหลายเดือนข้างหน้า

![ข้อจำกัดด้านราคาและการซ่อมบำรุงฉุดการนำเข้าอโนดทองแดงของจีน [SMM Analysis]](https://imgqn.smm.cn/usercenter/mpocQ20251217171712.jpg)