SMM Apr 20 News:

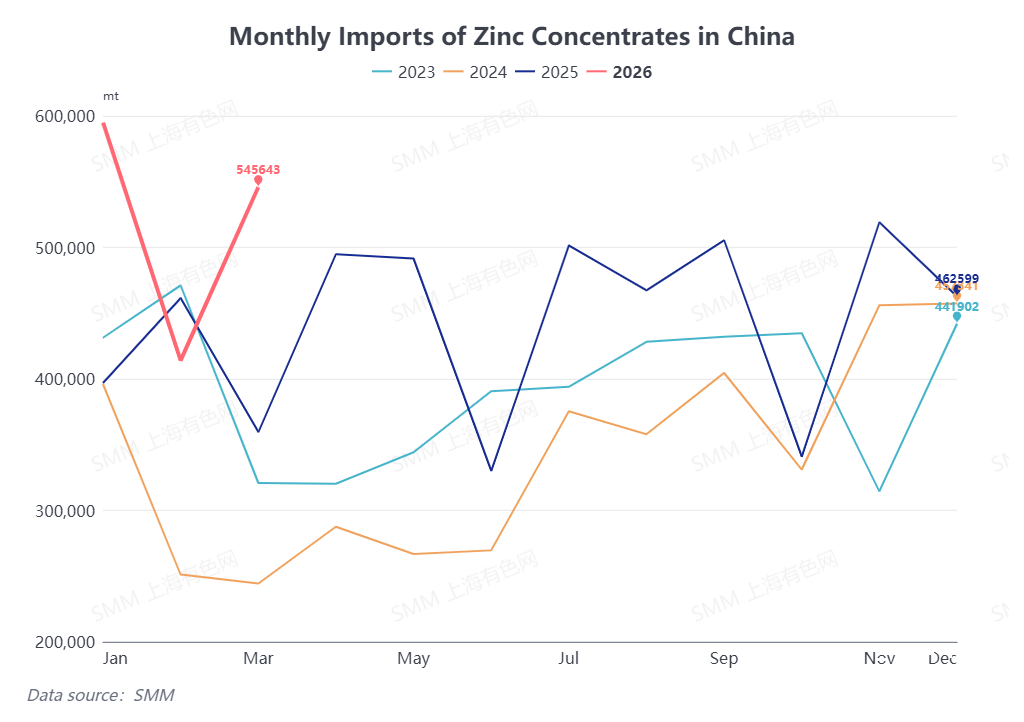

According to the latest customs data, China imported 545,600 mt in physical content of zinc concentrates in March 2026, up 31.8% MoM from February (131,700 mt in physical content) and up 51.78% YoY. Cumulative zinc concentrates imports from January to March totaled 1.5544 million mt in physical content, up 27.64% YoY cumulatively.

By country, in March 2026, the top 3 source countries were Peru (115,800 mt in physical content, accounting for 21.2%), Australia (87,000 mt in physical content, accounting for 16%), and South Africa (48,900 mt in physical content in December, accounting for 9%). On a MoM basis, arrivals from Peru, Bolivia, and Namibia saw notable increases in March, while flows from Australia, Iran, and other countries into China declined to varying degrees.

China's zinc concentrates imports in March increased significantly compared with February. SMM believed the reasons were as follows:

1. Demand side, as the Chinese New Year holiday ended, China's refined zinc production rose MoM in March from February, and overall domestic demand for zinc concentrates increased.

2. Supply side, Q1 was a regular production suspension season for some domestic mines, and domestic ore supply was relatively lower. To maintain normal production, smelters actively purchased imported zinc concentrates in the earlier period to supplement raw material stocking in March, resulting in large inflows of imported zinc concentrates.

Entering April, SMM expects China's zinc concentrates imports to face downside risks. On one hand, domestic mines that previously suspended production will gradually resume production in April, with domestic zinc concentrates production rising MoM and domestic ore supply increasing. On the other hand, floods and typhoons in Australia in March disrupted zinc concentrates transportation, and based on shipping cycle estimates, arrivals from Australia to China in April are expected to be affected. Considering multiple factors, China's zinc concentrates imports in April are expected to fall short of March levels.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)