ข่าว SMM, 6 มีนาคม,

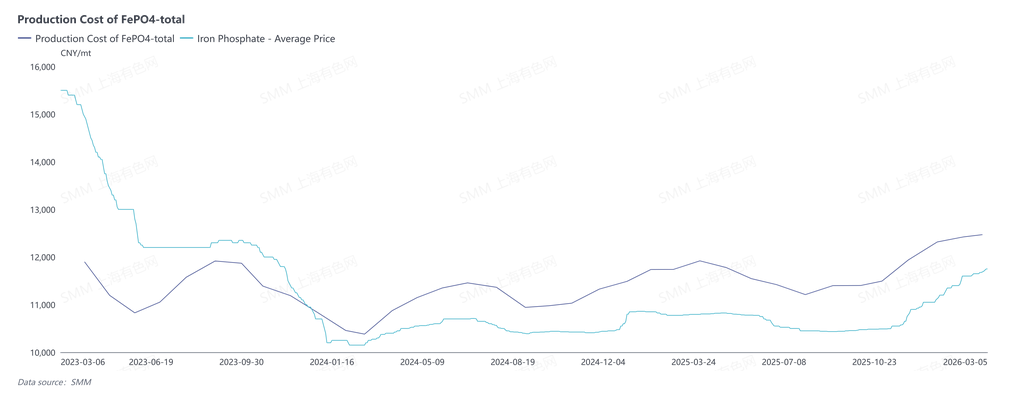

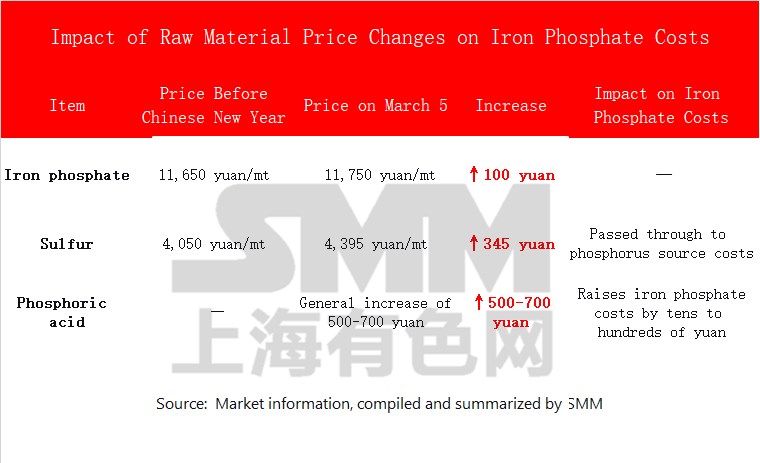

ประเด็นสำคัญ: หลังตรุษจีน ราคาฟอสเฟตเหล็กปรับขึ้น 100 หยวน/ตัน แต่ยังไม่ถูกนำไปใช้จริง ต้นน้ำ ราคากรดฟอสฟอริกพุ่งขึ้นฉับพลัน 500–700 หยวน/ตัน ลบล้างการปรับขึ้นทั้งหมดโดยตรง และถึงขั้นทำให้ส่วนต่างติดลบ ต้นตอของการขึ้นราคารอบนี้อยู่ที่กำมะถัน: อุปทานโลกตึงตัวประกอบกับความขัดแย้งภูมิรัฐศาสตร์สหรัฐฯ–อิหร่าน ทำให้ราคากำมะถันพุ่ง 345 หยวน/ตัน ดันต้นทุนแหล่งฟอสฟอรัสปรับขึ้นเป็นวงกว้าง ก่อนหน้านี้ การขึ้นราคากำมะถันเผชิญแรงต้านสูงในการส่งผ่านลงปลายน้ำจากภาคเกษตร แต่ครั้งนี้ถูกส่งผ่านลงปลายน้ำแบบครอบคลุมทั่วทั้งห่วงโซ่ ผู้ประกอบการฟอสเฟตเหล็กกลับมาเป็น “ชั้นกลาง” อีกครั้ง: การขึ้นราคาเป็นเพียงภาพลวงตาของการส่งผ่านต้นทุน และการฟื้นตัวของกำไรยังเป็นเรื่องไกลเกินเอื้อม หลังตรุษจีน ตลาดฟอสเฟตเหล็กในที่สุดก็เห็นสัญญาณฟื้นตัวที่รอคอยมานาน ณ วันที่ 5 มีนาคม 2026 ราคาโรงงานรวมภาษีต่อหนึ่งตันของฟอสเฟตเหล็กปรับขึ้นจาก 11,650 หยวนก่อนวันหยุดเป็น 11,750 หยวน เพิ่มขึ้นเล็กน้อย 100 หยวน/ตัน แม้การปรับขึ้นจะไม่มาก แต่อย่างน้อยก็ช่วยผ่อนคลายแรงกดดันด้านต้นทุนที่ตึงเครียดมานานได้ชั่วคราว

อย่างไรก็ตาม ก่อนจะได้หายใจโล่ง วันที่ 5 มีนาคม ราคากรดฟอสฟอริกกลับปรับขึ้นพร้อมกัน 500–700 หยวน/ตัน—ก่อนที่ผู้ประกอบการฟอสเฟตเหล็กจะได้ฉลอง “มีดอีโต้” ฝั่งต้นทุนก็ฟันลงมาแล้ว

ขึ้น 100 หยวน แต่ถูก “เอาไป” มากกว่า ภายนอก การขึ้นราคาฟอสเฟตเหล็กดูเป็นบวก แต่เมื่อแยกโครงสร้างต้นทุน ความจริงกลับไม่น่ายินดีเลย

เมื่อวันที่ 5 มีนาคม 2026 ราคากรดฟอสฟอริกโดยทั่วไปถูกปรับขึ้น 500–700 หยวน/ตัน เมื่อพิจารณาสัดส่วนของกรดฟอสฟอริกในต้นทุนฟอสเฟตเหล็ก เพียงรายการนี้ก็จะดันต้นทุนการผลิตฟอสเฟตเหล็กเพิ่มขึ้นตั้งแต่หลักสิบถึงหลักหลายร้อยหยวน—หมายความว่า 100 หยวนที่เพิ่งได้มา ยังไม่ทันตั้งตัวก็ถูกฝั่งวัตถุดิบ “ดึงไป” เป็นส่วนใหญ่ และอาจถึงขั้นกลายเป็นส่วนต่างติดลบ โดยเฉพาะกระบวนการสายเหล็ก ซึ่งได้รับผลกระทบด้านต้นทุนมากกว่า

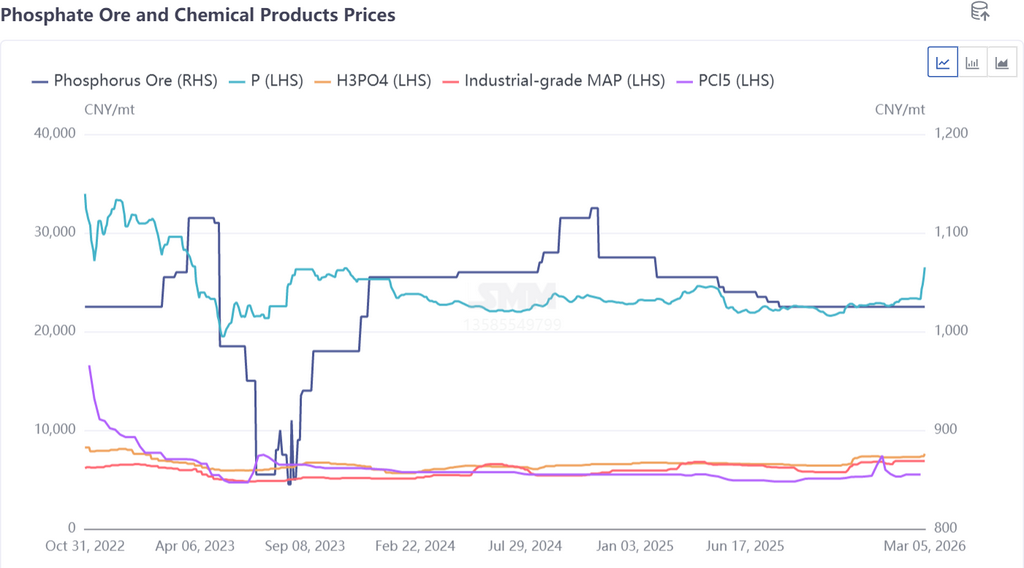

ทำไมกรดฟอสฟอริกถึงพุ่งขึ้นฉับพลัน? ก็เป็น “คนคุ้นเคย” เจ้าเดิม—กำมะถัน

ภูมิรัฐศาสตร์ “เติมเชื้อไฟ”

หากอุปสงค์–อุปทานที่ตึงตัวเป็น “ประเด็นเก่า” แล้ว ความขัดแย้งทางภูมิรัฐศาสตร์สหรัฐฯ–อิหร่านที่ปะทุเมื่อวันที่ 28 กุมภาพันธ์ 2026 ก็เหมือนสาดน้ำมันลงบนห่วงโซ่อุปทานกำมะถันที่ตึงอยู่แล้ว

จีนพึ่งพาการนำเข้ากำมะถันมากกว่า 50% โดยอุปทานจากตะวันออกกลางคิดเป็นสัดส่วนสูงถึง 56.2% และอิหร่านยังเป็นแหล่งนำเข้ากำมะถันจากตะวันออกกลางรายใหญ่อันดับ 2 ของจีน หลังความขัดแย้งทวีความรุนแรง การเดินเรือผ่านช่องแคบฮอร์มุซถูกรบกวน ทำให้อุปทานระยะสั้นจากอิหร่านแทบลดลงเป็นศูนย์ ประเทศผู้ผลิตกำมะถันอื่น ๆ ในตะวันออกกลางก็จำกัดการส่งมอบพร้อมกันและปรับขึ้นราคาอย่างรุนแรง ส่งผลให้ปริมาณหมุนเวียนที่แท้จริงของกำมะถันทั่วโลกลดฮวบลงมากกว่า 10% แม้ผู้ประกอบการกรดฟอสฟอริกจะปรับราคาแบบเข้มข้นในวันที่ 5 มีนาคมเท่านั้น (ธรรมเนียมของอุตสาหกรรมในหมู่ผู้ผลิตรายใหญ่ที่ปรับราคาในวันที่ 5) แต่ในความเป็นจริง ต้นทุนการผลิตกรดฟอสฟอริกเริ่มปรับขึ้นตั้งแต่วันที่ 28 กุมภาพันธ์แล้ว เพียงแต่ต้องใช้เวลาสักระยะกว่าการส่งผ่านต้นทุนจะไปถึงส่วนของเหล็กฟอสเฟต

เมื่อมองย้อนกลับไปที่ความผันผวนราคารอบนี้ ผู้ประกอบการเหล็กฟอสเฟตได้ตกอยู่ในภาวะกลืนไม่เข้าคายไม่ออกที่คุ้นเคยอีกครั้ง:

ปลายน้ำ: ราคาเหล็กฟอสเฟตในที่สุดก็ปรับขึ้น 100 หยวน/ตัน

ต้นน้ำ: ราคากรดฟอสฟอริกพุ่งขึ้น 500–700 หยวน/ตัน และแรงกดดันด้านต้นทุนถูกส่งผ่านอย่างรวดเร็ว

สาเหตุราก: กำมะถันเพิ่มขึ้น 345 หยวน/ตัน โดยความขัดแย้งทางภูมิรัฐศาสตร์ยิ่งทำให้อุปทานตึงตัว

กำไร 100 หยวนที่ยังไม่ทันได้เข้ากระเป๋า ก็ถูก “เฉลี่ยออกไป” เป็นส่วนใหญ่—หากไม่ถึงกับทั้งหมด—ให้กับแหล่งวัตถุดิบฟอสฟอรัสต้นน้ำ ผู้ประกอบการเหล็กฟอสเฟตกลับมารับบท “ชั้นกลาง” อีกครั้ง: วัตถุดิบต้นน้ำขึ้นราคา การส่งผ่านไปปลายน้ำไม่ราบรื่น และอัตรากำไรถูกบีบซ้ำแล้วซ้ำเล่า

สรุป: สถานะเชิงรับยังไม่เปลี่ยน และการปรับดีขึ้นของกำไรยังเป็นเรื่องฟุ่มเฟือย

การปรับขึ้นราคาเหล็กฟอสเฟตรอบนี้โดยสาระสำคัญเป็นการปรับแบบเชิงรับที่ขับเคลื่อนด้วยต้นทุน ไม่ใช่แรงหนุนจากอุปสงค์ที่นำไปสู่การเพิ่มกำไร ห่วงโซ่การส่งผ่านต้นทุน “กำมะถัน–กรดฟอสฟอริก–เหล็กฟอสเฟต” ชัดเจนและโหดร้าย: กำมะถันขึ้น กรดฟอสฟอริกตาม ต้นทุนเหล็กฟอสเฟตถูกยกขึ้นตาม และการขึ้นราคาส่วนใหญ่ (หากไม่ถึงกับทั้งหมด) ถูกฝั่งวัตถุดิบกลืนไป

ท่ามกลางฉากหลังที่รูปแบบอุปทานกำมะถันโลกยังตึงตัวไม่เปลี่ยน และความเสี่ยงภูมิรัฐศาสตร์ยังดำเนินต่อไป ผู้ประกอบการเหล็กฟอสเฟตยังต้องเผชิญบททดสอบหนักจากต้นทุนสูงและกำไรบาง ผลของ “การปฏิวัติ” ขึ้นราคาได้ถูกกำมะถันและกรดฟอสฟอริก “ขโมยไป” อีกครั้ง

เหตุการณ์เฟอร์รัสซัลเฟตรอบก่อน: เหล็กฟอสเฟตขึ้น 500 หยวนแต่ “ทำกำไรไม่ได้”? กระแสคลั่งขึ้นราคาถูกต้นทุนกลืนกิน [บทวิเคราะห์ SMM]

https://t.smm.cn/c2S7z8oT

หมายเหตุ: หากคุณมีข้อมูลเพิ่มเติมหรือข้อแก้ไขเกี่ยวกับรายละเอียดที่กล่าวถึงในบทความนี้ โปรดติดต่อเราได้ตลอดเวลา ข้อมูลติดต่อมีดังนี้:

โทร: 021-20707860 (หรือเพิ่ม WeChat 13585549799) Yang Chaoxing ขอบคุณ!

![[SMM PV News] รัฐเมนกลายเป็นรัฐที่สองของสหรัฐฯ ที่ผ่านกฎหมายโซลาร์เซลล์แบบเสียบปลั๊กสำหรับระเบียง](https://imgqn.smm.cn/usercenter/vwTDJ20251217171728.jpg)

![[SMM PV News] บอตสวานาจับมือโอมานพัฒนาโครงการโซลาร์พร้อมระบบกักเก็บพลังงานขนาด 500 เมกะวัตต์](https://imgqn.smm.cn/usercenter/JmyWy20251217171729.png)

![[SMM PV News] สาธารณรัฐโดมินิกันเปิดซองประมูลโครงการพลังงานหมุนเวียน 600 MW พร้อมข้อกำหนดระบบกักเก็บพลังงาน 4 ชั่วโมง](https://imgqn.smm.cn/usercenter/jZvMC20251217171729.jpg)