SMM February 6th:

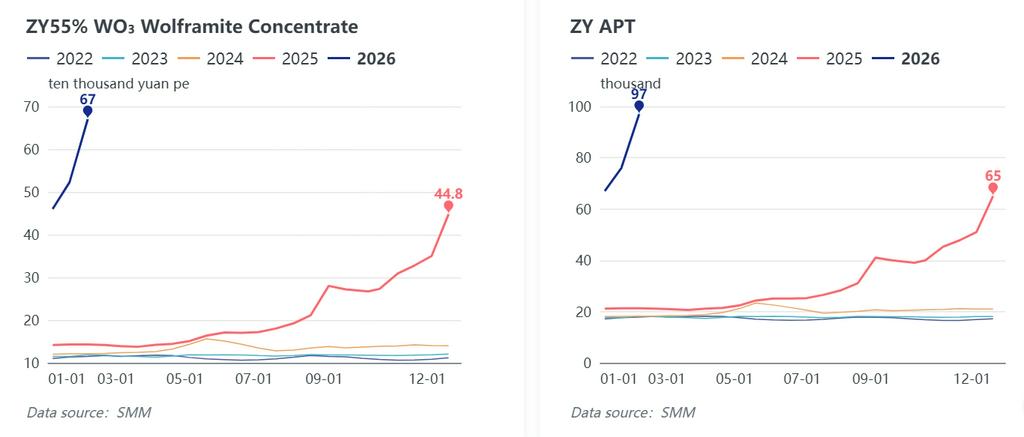

This week, the tungsten market continued its strong upward trend, with the tight spot supply pattern at the raw material end becoming increasingly pronounced and prices of products across the industrial chain rising collectively. Coupled with the festive effect ahead of the Spring Festival, the market exhibited the operational characteristic of "price hikes on shrinking trading volumes". Today, tungsten enterprises including those in Chongyi released a new round of long-term contract prices: a major tungsten enterprise in Chongyi raised the long-term purchase price of 55% tungsten concentrate for the first half of February by RMB 147,000 per standard ton month-on-month to RMB 669,000-670,000 per standard ton, and the price of APT (Ammonium Paratungstate) was raised by RMB 300,000 to RMB 970,000 per standard ton. The sharp increase in long-term contract prices has reignited the market, and the overseas international market has moved upward in tandem. The strong market pattern is expected to continue in the short term.

Domestic Spot Prices Surge Across the Board, Tightness at Raw Material End Intensifies

Domestic prices of tungsten raw materials and deep-processed products have climbed continuously this week. As of February 5, quoted prices of all product lines rose significantly from the previous day and the start of the week, with the highest quotes of core products hitting new recent highs: the transaction price of 65% black tungsten concentrate has surged above RMB 650,000 per standard ton, with a cumulative increase of RMB 200,000 per ton year-to-date. High-grade ore supply is scarce in the market, which is tilted toward a seller's market, and downstream players have mainly followed the price hikes passively. The highest quote of 70 ferro-tungsten reached RMB 905,000 per base ton, with a cumulative year-to-date increase of RMB 259,000 per ton. Domestic special steel enterprises are stocking up ahead of the Spring Festival, leading to a slight increase in transactions compared with the previous period. Driven by costs, most transactions are negotiated on a one order, one price basis. SMM's quoted price of APT closed at RMB 970,000 per ton, up RMB 300,000 per ton year-to-date, and some holders quoted near RMB 1,000,000 per ton in the afternoon trading session. The highest quote of tungsten powder has broken through RMB 1.6 million per ton, with a cumulative year-to-date rise of RMB 500,000 per ton. Based on the current APT price, the powder segment enjoys considerable profit margins, but there is limited room for price concessions in the industry. Holders maintain firm quoting attitudes, forcing some cemented carbide enterprises to switch to purchasing APT raw materials and outsource powder processing to contract manufacturers.

Sluggish Market Trading Activity, Distinct Supply-Demand Game Characteristics

Despite the continuous price hikes, overall market activity failed to rise in tandem this week, constrained by multiple factors: first, ahead of the Spring Festival, traders have adopted a cautious operational approach, with purchases driven only by rigid demand and only a small amount of pre-holiday stocking, without large-scale hoarding; second, capital pressure and bullish sentiment coexist—some downstream enterprises have suspended procurement plans and adopted a wait-and-see stance due to high price levels; third, the festive effect has gradually emerged, with some enterprises entering pre-holiday shutdowns, leading to a decline in market trading frequency.

The cemented carbide industry has been particularly affected in this regard. As the core demand sector for tungsten (accounting for 58% of total tungsten demand), its procurement demand for tungsten raw materials directly drives market trends. This week, surging prices of raw materials such as tungsten powder have pushed up the production costs of cemented carbide sharply—tungsten materials such as tungsten carbide account for more than 80% of the production costs of cemented carbide cutting tools. Most cemented carbide enterprises have been forced to reduce procurement scales and only maintain production to meet rigid demand, further curbing market trading activity.

In the scrap tungsten market, the overall tight supply pattern persisted this week. Driven by the expanding supply gap of primary tungsten raw materials, regenerated tungsten, as an important supplementary source, has seen robust market demand. However, ahead of the Spring Festival, the recovery volume of scrap tungsten has declined, and some holders have increased their demand for cash realization before the holiday, leading to a slowdown in the price rise of scrap tungsten this week. As of today, the quoted price of scrap tungsten bars stands at RMB 835 per kilogram, up RMB 235 per kilogram from the start of the year. SMM estimates that China's tungsten regeneration and recovery rate in 2025 was about 33%, far lower than the level of over 50% in developed countries. Against the backdrop of the persistent tight supply pattern in the mining raw material market in the future, China's scrap tungsten market capacity is expected to continue expanding. Meanwhile, continuous attention will be paid to the potential adjustment of China's scrap tungsten import policies.

International Market Trends

As of today, the international tungsten market has seen a partial price rise, moving in tandem with the domestic market. APT transactions in Europe have risen to USD 1,500 per ton unit, with the price gap between Europe and China narrowing further. The tight supply in the European market remains unchanged, and prices are expected to continue catching up in the near future.

In the short term, the tight spot supply pattern at the raw material end cannot be alleviated quickly, and holders' reluctance to sell will persist, meaning the tungsten market is expected to maintain its strong upward trend. Key attention should be paid to the potential impacts brought by the approaching Spring Festival: on the one hand, market trading will halt during the holiday, and whether the concentrated release of pre-holiday stocking demand from some enterprises will affect short-term price trends; on the other hand, the post-holiday market resumption pace, the recovery of raw material supply, and the strength of downstream demand release will determine whether prices can remain at high levels in the follow-up.

Specifically, the post-holiday resumption of production in the cemented carbide industry warrants key attention—if the recovery of downstream manufacturing drives the release of cemented carbide demand, it will further boost the procurement demand for tungsten raw materials and support the continued strong trend of tungsten prices. For the scrap tungsten market, focus should be placed on the post-holiday resumption progress of regeneration enterprises, changes in scrap tungsten recovery volumes, and the improvement of regeneration utilization rates. If the supply of regenerated tungsten increases, it may alleviate the tight raw material pressure to a certain extent and curb the excessive rise of tungsten prices.

In addition, continuous tracking is required for international market price changes, enterprise long-term contract transaction conditions, industry policy trends, as well as cost pass-through in the cemented carbide industry and supply-demand changes in the scrap tungsten market, with vigilance against market risks brought by high-level price fluctuations.