SHANGHAI, May 27 (SMM) - This is a roundup of China's metals weekly inventory as of May 27.

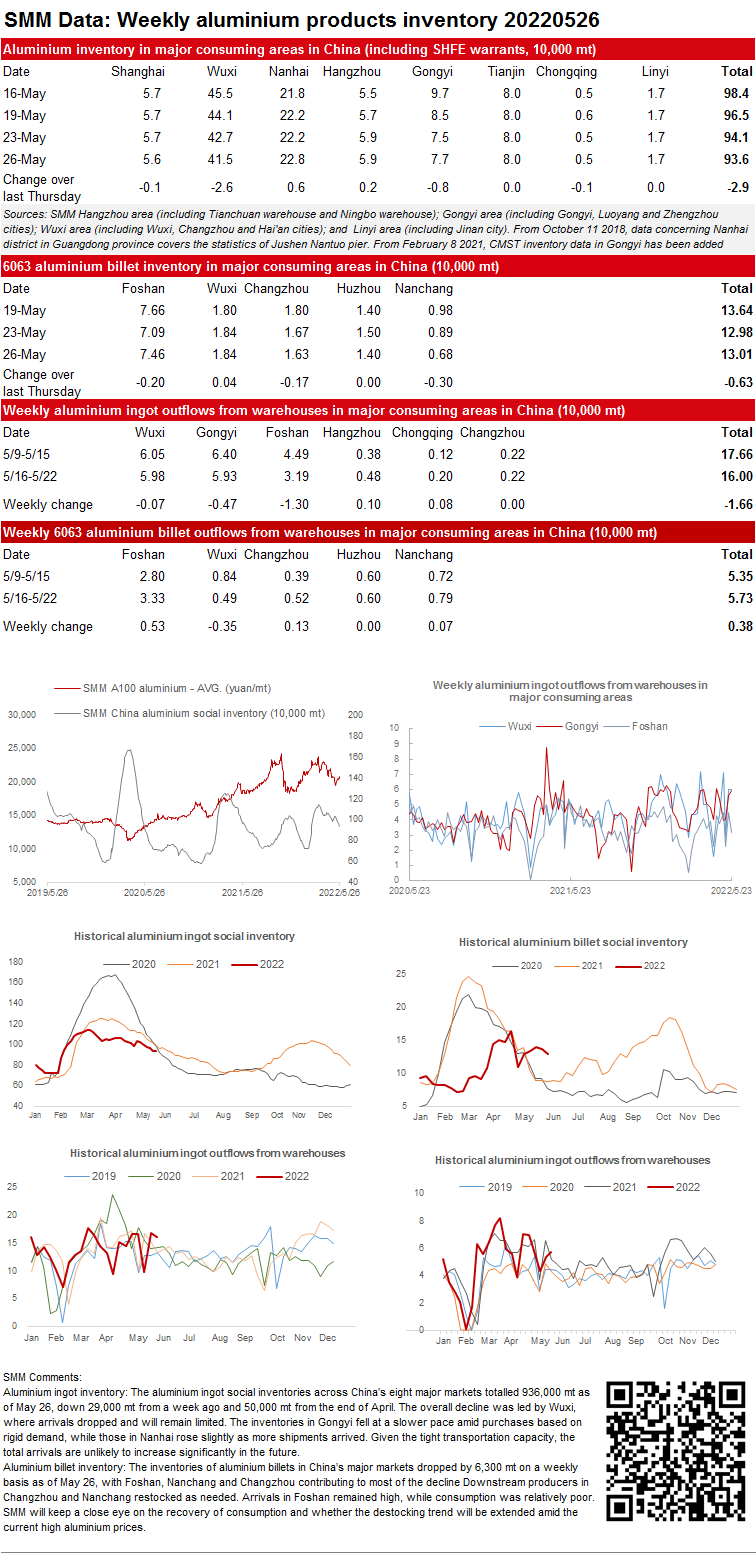

Aluminium ingot inventory: The aluminium ingot social inventories across China’s eight major markets totalled 936,000 mt as of May 26, down 29,000 mt from a week ago and 50,000 mt from the end of April. The overall decline was led by Wuxi, where arrivals dropped and will remain limited. The inventories in Gongyi fell at a slower pace amid purchases based on rigid demand, while those in Nanhai rose slightly as more shipments arrived. Given the tight transportation capacity, the total arrivals are unlikely to increase significantly in the future.

Aluminium billet inventory: The inventories of aluminium billets in China’s major markets dropped by 6,300 mt on a weekly basis as of May 26, with Foshan, Nanchang and Changzhou contributing to most of the decline Downstream producers in Changzhou and Nanchang restocked as needed. Arrivals in Foshan remained high, while consumption was relatively poor. SMM will keep a close eye on the recovery of consumption and whether the destocking trend will be extended amid the current high aluminium prices.

Copper Inventory in Major Chinese Markets Fell 2,200 mt on Week

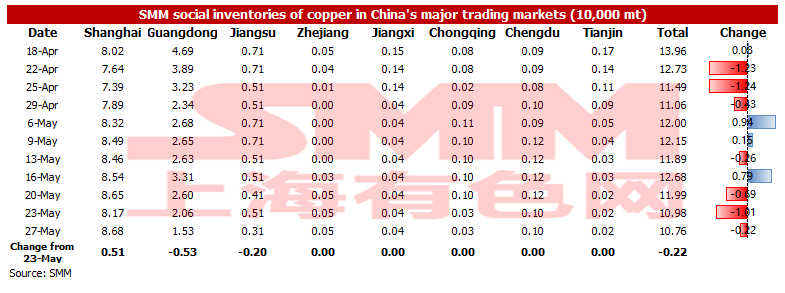

As of May 27, SMM copper inventory across major Chinese markets dropped by 2,200 mt to 107,600 mt from Monday to Friday, a decrease of 12,300 mt from last Friday. The inventory dropped sharply this week. The inventory in China showed a continuous decline after May 1 mainly because of the decrease in supply and the increase in demand. Compared with the data on Monday, the inventory in most regions of China this week fell, while the inventories in Shanghai rose. The total inventory fell 221,300 mt from the same period last year when the inventory was recorded at 328,900 mt. Because the arrival of imported copper in Shanghai increased, and the logistics of the city have not fully recovered, the inventory in Shanghai increased this week. In Guangdong, the inventory dropped sharply as the arrival of domestic copper increased slightly and some copper cathode was transported to regions where the downstream consumption is relatively good. The inventory in Jiangsu fell due to the increase in pick-up aroused by the recovered downstream consumption.

In detail, the inventory in Shanghai increased by 5,100 mt to 86,800 mt, the inventory in Guangdong dipped by 5,300 mt to 15,300 mt, and the inventory in Jiangsu dropped by 2,000 mt to 3,100 mt.

Looking forward, it is expected that the arrival of imported copper will increase next week, and the domestic supply will also rise, but the consumption may decrease due to the end of the month. SMM expects that the weekly inventory next week will increase slightly, while it dropped compared with the same period last year. The market shall pay attention to whether the downstream enterprises will restock actively during the Dragon Boat Festival.

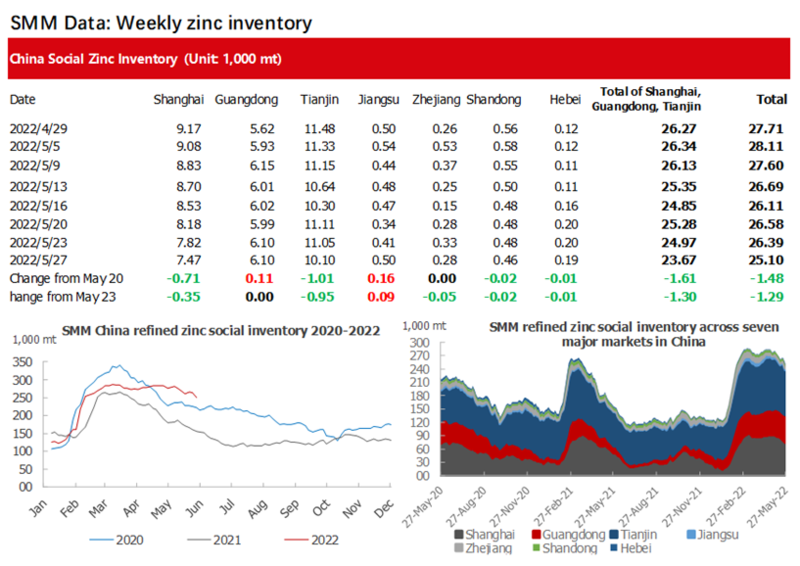

Inventories across seven major markets in China decreased 12,900 mt from May 23

Total zinc ingots inventories across seven major markets in China stood at 251,000 mt as of Friday May 27, down 12,900 mt from May 23, down 14,800 mt from May 20. Inventory of zinc continued to decrease sharply this week. In Shanghai, after the pandemic prevention and control measures loosened, pace of downstream delivery-taking remained stable. Market inventory continued to reduce amid tight arrivals. In Tianjin, the pandemic prevention measures loosened in Dongli where delivery-taking was limited before. Therefore, the downstream orders which were made before offered pricing and delivered cargoes this week, leading to reduction in inventory. On the other hand, some of the early arbitrage traders still tended to export. Stocks were shipped for exports this week, driving down the inventory in Tianjin. In Guangdong, the downstream consumption was weak and the shipping cargoes did not increase. With stable arrivals, inventory in Guangdong remained flat this week. Inventories in Shanghai, Guangdong and Tianjin dropped 13,000 mt and inventories across seven major markets decreased 12,900 mt.

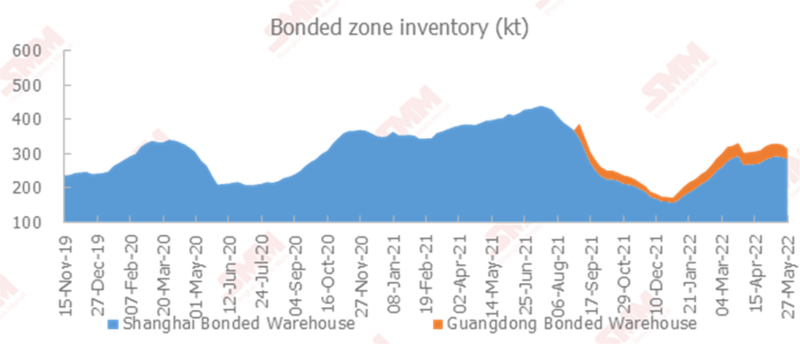

Copper Inventory in Bonded Zone Dipped 11,300 mt on Week

Copper inventories in the domestic bonded zone decreased by 11,300 mt to 303,400 mt from May 20 to May 27, according to the SMM survey. Inventory in the Shanghai bonded zone decreased by 9,300 mt to 275,000 mt, and inventory in the Guangdong bonded zone dropped by 2,000 mt to 28,400 mt. The import profits have driven customs clearance by traders, so the bonded zone inventory has continued to decline. However, with the close of the import window, the demand for customs declaration has cooled down. It is expected that the decrease in inventory will slow down.

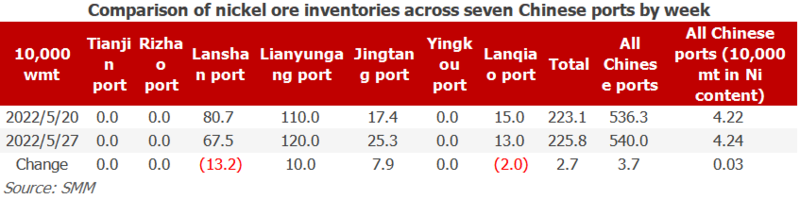

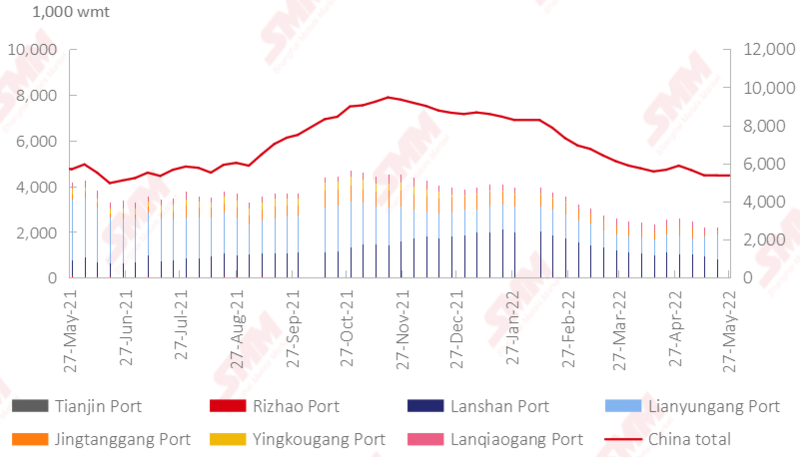

Nickel Ore Inventories at Chinese Ports up 37,000 wmt on Week

On May 27, the inventory of nickel ore across Chinese ports increased by 37,000 wmt to 5.4 million wmt compared with last week. The total Ni content increased by 300 mt to 42,400 mt. The total inventory at seven major ports across China stood at 2.258 million wmt, 27,000 wmt higher than the previous week. The port inventory of nickel ore stopped falling and increased slightly, but it was still at a historically low level. On the supply side, when the poor weather conditions in the Philippines in April and May ended, shipment from mines and goods transportation returned to normal, so the supply of nickel ore increased. On the demand side, due to the dropping NPI prices, NPI plants could get some profits to maintain their normal production and demand for raw materials.Besides, the previous nickel ore supply could not meet the demand due to the prolonged rainy season in the Philippines, hence some goods produced in June will be delivered according to the previous orders. The increase in nickel ore inventory will be limited in the future market. In the short term, the port inventory of nickel ore will keep increasing slightly, and the market shall pay attention to the shipment from the Philippines and the domestic NPI plants’ demand for raw materials.

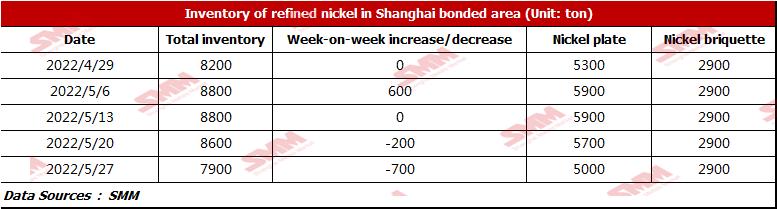

Bonded Zone Inventory of Pure Nickel Dropped Sharply due to the Import Profits

The spot imports of pure nickel remained profitable this week. The dropping of pure nickel premiums significantly increased the customs clearance. At present, traders bear huge pressure from the large spread between the front-month and next-month contracts, so the premiums are expected to be further lowered. Nickel inventory in Shanghai bonded zone totalled 7,900 mt this week, a decrease of 700 mt from last week. The inventory of nickel briquettes and nickel plates was 2,900 mt and 5,000 mt respectively.

![Manufacturers' Daily Output Increase Covered Maintenance Reductions, Yet Transaction Recovery Failed to Reverse Plant Inventory Accumulation [SMM Magnesium Weekly Data]](https://imgqn.smm.cn/usercenter/xLlnY20251217171724.jpeg)