SMM April 21:

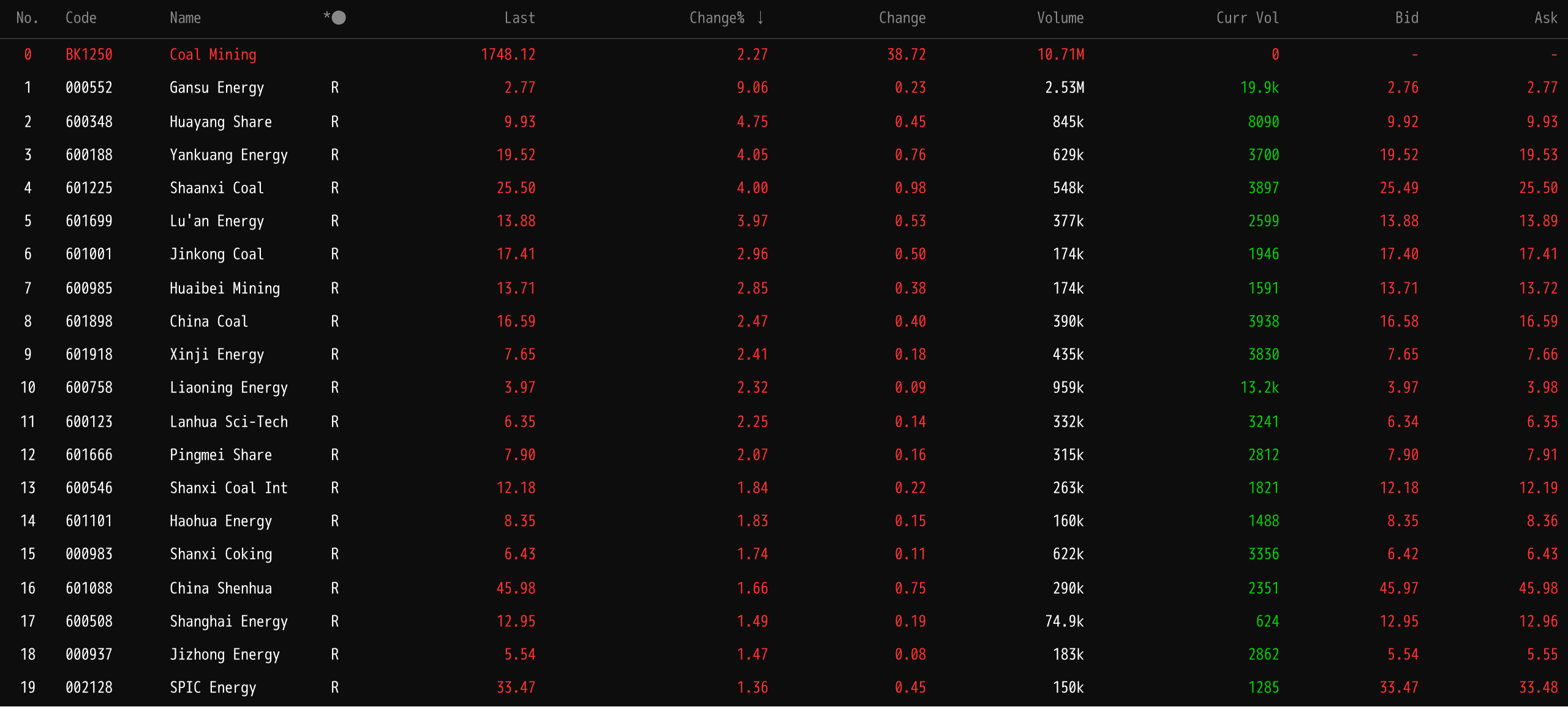

As the anti-involution policy continued to advance, the second round of coke price hikes was officially implemented. This, combined with persistently tight spot supply and demand, capacity constraints caused by Daqin Railway maintenance, the highlighted coal substitution advantage driven by high oil prices, and incremental demand from continued increases in hot metal production, created multiple positive factors that drove the coal mining sector to a two-day winning streak. Specifically, on the supply side, the Daqin Railway spring concentrated maintenance restricted north-to-south coal transportation capacity, inventories continued to decline, and the implementation of coke price hikes further transmitted cost support, pushing coal prices steadily upward. On the demand side, a stronger-than-usual off-season pattern emerged, with hot metal production continuing to edge up, coupled with significant YoY and MoM increases in daily consumption at coastal power plants. Restocking demand from the construction materials and other industries was released ahead of the Labour Day holiday, and with power plant inventories at low levels, seasonal restocking demand was activated early. In addition, tensions in the Middle East pushed up international oil prices, highlighting the economic advantage of coal-fired power, while the defensive attributes of the coal sector attracted some capital inflows, jointly driving the sector higher. As of the close on April 21, the sector gained 2.27%, with individual stocks performing actively. Gansu Energy Chemical, Huayang New Material Technology, Yankuang Energy, Shaanxi Coal Industry, and Lu'an Clean Energy led the gains.

Futures market: As of the daytime close on April 21, ferrous metals mostly rose, with coking coal up 1.53% and coke up 2.42%.

Spot market

Hot metal production is expected to continue edging up this week

On April 15, the blast furnace operating rate of the 242 steel mills tracked by SMM rose WoW. The sample steel mills' daily average hot metal production increased WoW. Last week, according to the latest SMM survey, no new blast furnace maintenance was reported, and a total of 2 blast furnaces resumed production, mainly concentrated in Shanxi. Currently, blast furnace profits were under pressure, and most steel mills produced normally as planned. The pace of maintenance and production resumptions remained generally stable, with hot metal production staying relatively steady. Looking ahead to this week, hot metal production is expected to continue edging up.

Spot market:On April 21, the Linfen low-sulphur coking coal price was quoted at 1,530 yuan/mt. The Tangshan low-sulphur coking coal price was quoted at 1,550 yuan/mt. The nationwide average price of first-grade metallurgical coke (dry quenching) was 1,845 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (dry quenching) was 1,705 yuan/mt. The nationwide average price of first-grade metallurgical coke (wet quenching) was 1,490 yuan/mt. The nationwide average price of quasi-first-grade metallurgical coke (wet quenching) was 1,400 yuan/mt.

Coking coal market:Production at some mines that had previously cut production recovered somewhat, but major mines were still affected by safety inspections, and the incremental supply of coking coal remained limited. Moreover, futures rallied, market sentiment warmed notably, stimulating some coal grades to stabilize and rebound. In the short term, coking coal prices may hold up well.

Coke market:In terms of supply, coke enterprises' per-mt profitability has recovered, production enthusiasm was moderate, shipments were relatively smooth, and in-plant coke inventory remained at low levels. Demand side, steel mills maintained strong production enthusiasm, hot metal production edged up, providing solid just-in-time procurement support for coke. Additionally, with the Labour Day holiday approaching, some steel mills released pre-holiday restocking demand. Overall, the coke supply-demand structure remained tight, and the coke market may hold up well in the short term.

Institutional Views

A Datong Securities research report showed: on coking coal, driven by downstream restocking and coke price hike expectations, port coking coal prices rose, while mine-mouth coal prices showed some divergence. At ports, Shanxi-origin coking coal warehouse-pickup prices at Jingtang Port rose WoW, while mine-mouth prices generally showed a stable-to-declining trend. Internationally, Australian Peak Downs hard coking coal CFR China prices were flat WoW. In the short term, with continued growth in hot metal production, sentiment boost from coke price hikes being implemented, and downstream restocking demand release, the coking coal market may see slight upward momentum.

A Shanxi Securities research report noted: currently, Daqin Line maintenance-related destocking and high landed costs of imported coal supported coal prices. Power plant daily consumption was at seasonal lows, while chemicals, steel mills, and other industries drove coal demand. Attention should be paid to the sustainability of just-in-time procurement from non-power industries and the summer electricity consumption peak after May. Investment recommendation: high uncertainty from US-Iran conflicts corresponds to high volatility, but oil prices are unlikely to decline significantly in the short term. Recovery signals have been confirmed, coal PPI is about to turn positive, coal prices are expected to rise, and coal stocks are poised for a Davis Double Play.

A Guohai Securities research report suggested that, from a broader perspective, the supply-side constraint logic for the coal mining industry remains unchanged, while demand may experience periodic fluctuations, with prices also showing certain oscillations and dynamic rebalancing. From the long-term industry development trend, the aforementioned driving factors still exist, and coal prices still have upward momentum over the long term. The process may be tortuous, but the direction should be clear. Leading coal enterprises have high asset quality, abundant cash flows on their books, exhibiting "five highs" — high profitability, high cash flow, high barriers, high dividends, and high margin of safety. Since 2025, multiple central and state-owned coal enterprises have initiated share buyback and asset injection plans for their publicly listed firms, also releasing positive signals, demonstrating confidence in coal enterprise development, and enhancing corporate growth potential and stability.

A Guangda Futures research report analyzed: Coking coal: supply side, most mines at production areas operated largely normally. There were reports that Mongolian coal throughput decreased due to factors such as fuel shortages. Recently, downstream buyers moderately restocked raw material coal, and overall inventory continued destocking. Demand side, steel mills maintained high hot metal production, with a preference for coke procurement. The second round of coke price increases was implemented, and coking enterprises restocked some coal grades with higher cost-effectiveness. Coking coal futures are expected to hold up well in the short term. Coke: Supply side, coking enterprises in some regions were constrained in operations due to government ultra-low emission retrofit requirements. Coking enterprises saw good shipments, and coke inventory mostly remained at low levels. Demand side, steel mills had a relatively strong willingness to produce, and mainstream steel mills accepted the second round of coke price increases. Transportation restrictions emerged in some regions, and steel mills experienced continuous destocking, with high procurement enthusiasm. Coke futures are expected to fluctuate upward in the short term.

Southwest Futures stated: In the short term, changes in the Middle East situation may still have sentiment impact on futures prices, but the impact on the actual supply-demand pattern of coking coal and coke is relatively small. Coking coal side, production at some mines in major producing areas was affected, but the impact on production was limited. Demand side, the online auction atmosphere improved recently, and quotes for some coal grades were raised. Coke side, some coking enterprises currently cut production, but the change in supply was relatively small; demand side, national daily hot metal production may continue to rebound, and demand expansion provides support for coke prices; the second round of spot coke price increases is being implemented. From a technical perspective, coking coal and coke futures may continue to move sideways in the medium term. Strategy-wise, investors may watch for buying opportunities at low levels and pay attention to position management.

Recommended reading:

![[SMM HRC Arrivals] Arrivals in the South China Market Increased WoW This Week](https://imgqn.smm.cn/usercenter/bkAyC20251217171720.jpg)

![[SMM Daily HRC Trading] Spot Cargo Trading Down WoW](https://imgqn.smm.cn/usercenter/tgoYV20251217171715.jpg)