Following the formal announcement by India’s Minister of Commerce and Industry, the India–Oman Comprehensive Economic Partnership Agreement (CEPA) will take effect on 1 June 2026. Market attention has largely focused on the surface-level benefit that “Oman will exempt an average 5% import tariff on 98% of Indian export goods.” However, looking beyond the appearance of tariff concessions, the export pricing dividend generated by the long-term depreciation of the rupee against the US dollar, combined with Oman’s strategic positioning as the re-export hub among the Gulf states, are the true core forces driving this wave of overseas expansion by India’s steel industry chain and the reshaping of Middle East supply–demand dynamics.

Macro Underlying Logic: Tariff Elimination × Rupee Depreciation Form a Dual Profit Safety Cushion

To understand this trade opportunity about to unfold in the Middle East, one must first grasp the compound effect of two independent variables.

- Systemic advantage of tariff elimination: Once CEPA takes effect, the 5% Import Weighted Tariff (IWT) generally applied by Oman to Indian steel products will be fully eliminated. This means Indian exporters will gain a systemic price-competitiveness advantage. Particularly in pricing battles against major competitors such as China (which faces an intermediate tariff of approximately 3.5%) and Turkey, this 5% price differential can be directly translated into more aggressive quotations or wider profit margins.

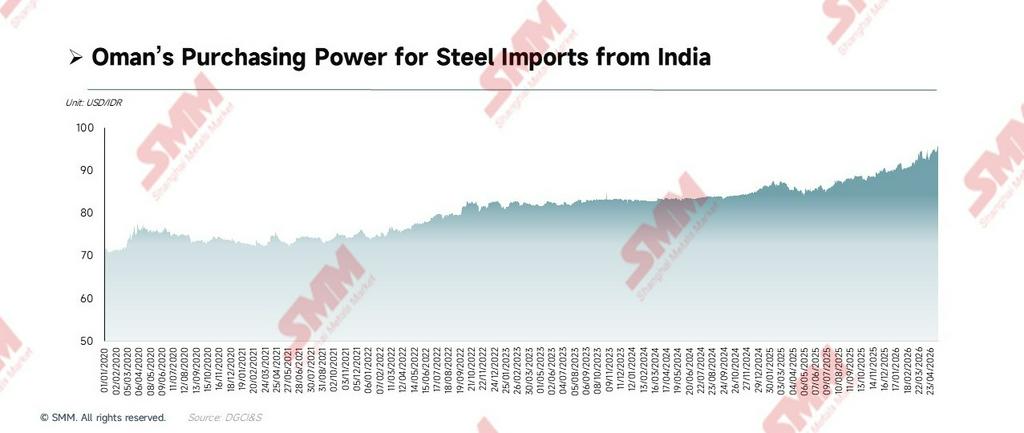

- Export pricing dividend from rupee depreciation: The Omani Rial (OMR) has long operated under a strict hard peg to the US dollar (1 OMR ≈ 2.6 USD). Over the past five years, the Indian rupee has shown a sustained depreciating trend against the US dollar—meaning that even if domestic Indian mills' ex-works rupee prices remain firm, USD-denominated quotations for Indian steel continue to drift lower. This essentially expands exporters' USD pricing room (i.e., an export sales dividend), rather than merely enhancing the importer's purchasing power.

When the “5% tariff elimination” and the “rupee-depreciation export dividend” converge historically in June 2026, the combined competitive advantage formed by these two superimposed forces will far exceed any simple tariff-cut calculation. This underlying advantage will not be confined to direct steel supply; it will propagate downstream along the industrial chain to automobiles, commercial vehicles, and machinery components, and in turn the prosperity of downstream exports will reflexively boost order expectations for high-end cold-rolled, automotive sheet, and coated products in the domestic market.

A Decade of Bilateral Trade Reviewed: Three Cycles Reveal the Supply–Demand Rhythm

A review of the past decade of India–Oman bilateral steel trade reveals three distinct cycles, each underpinned by its own macro-driving logic:

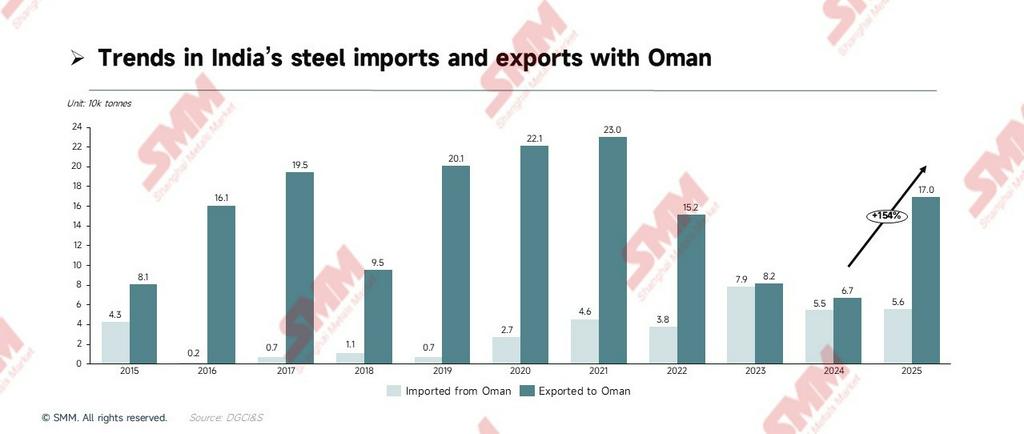

- Expansion phase (2015–2021): Indian exports climbed from 81,000 tonnes to a historical peak of 230,000 tonnes. The core driver was the infrastructure boom from the early implementation of Oman's “Vision 2040” strategy, with ports, roads, and industrial parks launched intensively, directly igniting demand for hot-rolled coil (HRC) and steel pipes. Even under the 2020 pandemic shock, the policy rigidity of Oman's infrastructure projects sustained robust procurement demand.

- Contraction phase (2022–2024): Exports declined steadily from 152,000 tonnes to a 2024 trough of 67,000 tonnes. Over the same period, Oman's billet exports to India hit a historical peak in 2023 (79,000 tonnes), and the bilateral trade surplus came close to zero. Behind this divergence: Oman's fiscal authorities tightened infrastructure investment under low oil-price pressure, while India's massive EAF short-process capacity kept lifting its rigid demand for low-cost Omani billets.

- Rebound phase (2025 to date): In 2025, Indian exports surged to 169,700 tonnes, a year-on-year jump of 153.95%, marking the largest single-year increase in the past eleven years. Notably, steel pipe exports alone broke through 116,000 tonnes—nearly 12 times the 2024 level. This is no coincidence; rather, it is the concentrated manifestation of “long-term contract lock-ins” completed early by Indian exporters and Omani buyers as CEPA expectations took hold.

Micro Product Breakdown: Steel Pipes Lead Finished-Product Exports, Billets Dominate Semi-Finished Backflow

Diving into the customs data by product category, we can clearly observe the deep upstream–downstream complementarity of bilateral trade along the industrial chain.

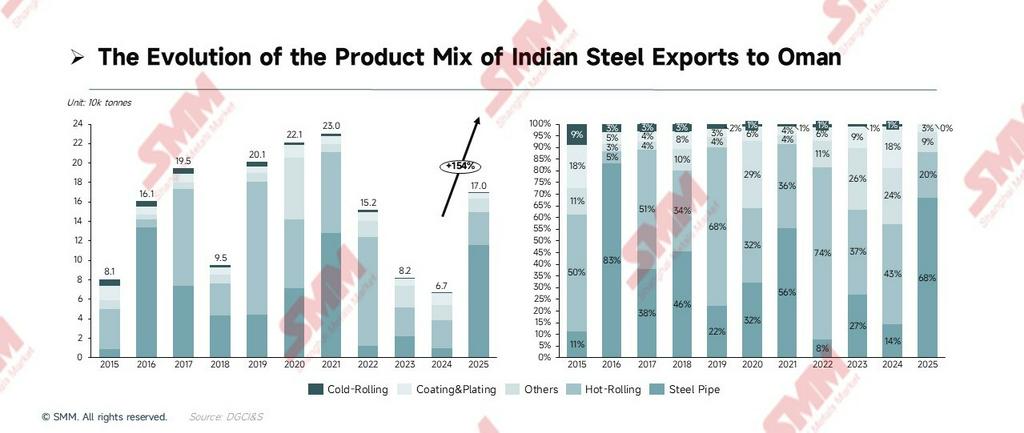

[Export side: expanding share of high value-added products]

- Steel pipes (the most prominent CEPA beneficiary): Steel pipe exports reached 115,000 tonnes in 2025—12.1 times the 2024 level. This aligns closely with the expansion of Oman's oil and gas pipeline network and the pipe-rack supporting construction in the Duqm Industrial Zone. With CEPA tariff elimination, the price advantage of Indian ERW/SSAW pipe products over both local Middle East and European-imported pipes will widen further.

- Hot-rolled coil (cyclical mainstay): Hot-rolled coil has long held the top position in cumulative export volume (peaking at 136,000 tonnes in 2019) and remains the bedrock for Oman's heavy-infrastructure steel demand. However, on a single-year basis in 2025 it was overtaken by steel pipes, confirming a product rotation within the export mix.

- Sections and coated products (marginal increments): Sections (structural steel) saw a historic leap in 2023–2024, in sync with steel-structure factory construction in the Duqm Industrial Zone. Coated sheet exports have held a stable range of 7,500–12,000 tonnes over the past three years. Objectively, the data does not yet support a judgment of a “continuously rising share,” but after CEPA's implementation, alongside Oman's light-manufacturing upgrade, meaningful marginal upside is in place.

[Import side: a closed-loop transoceanic industrial chain]

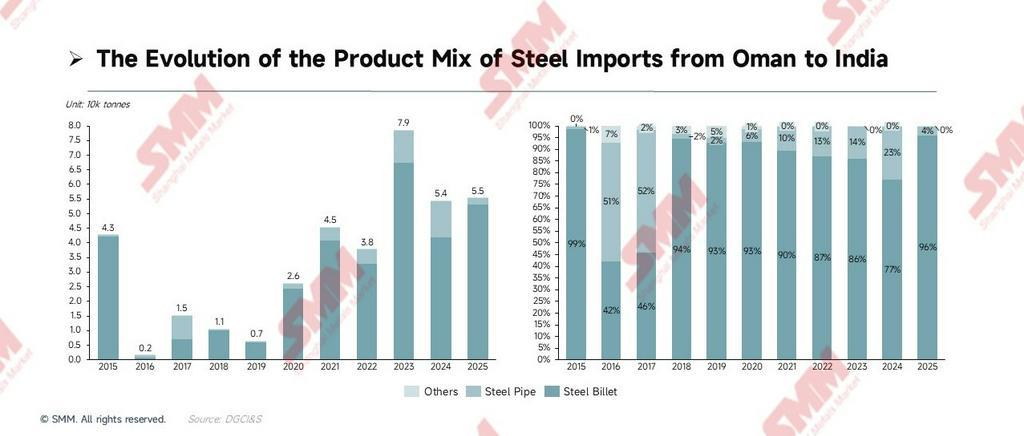

In stark contrast to the diversified export side, India's imports from Oman are highly concentrated in the semi-finished category of billets. In 2015, billets accounted for 98.4% of total imports; in 2023 they hit a historical peak of 68,000 tonnes; over the past three years (2023–2025), cumulative imports reached approximately 172,000 tonnes, sustaining high-level operation.

- Core industrial logic: India's vast EAF/induction-furnace short-process capacity has long faced a scrap-steel shortage, while Omani billets—produced using cheap natural gas (electricity costs roughly one-third of India's)—offer significant cost advantages. These billets flow back to India and into independent re-rolling mills, forming a closed-loop transoceanic industrial chain of “Oman billet-making—India re-rolling.” The Bilateral Investment Treaty (BIT) accompanying CEPA is expected to incentivize more Indian steel firms to invest directly in steelmaking operations in Oman.

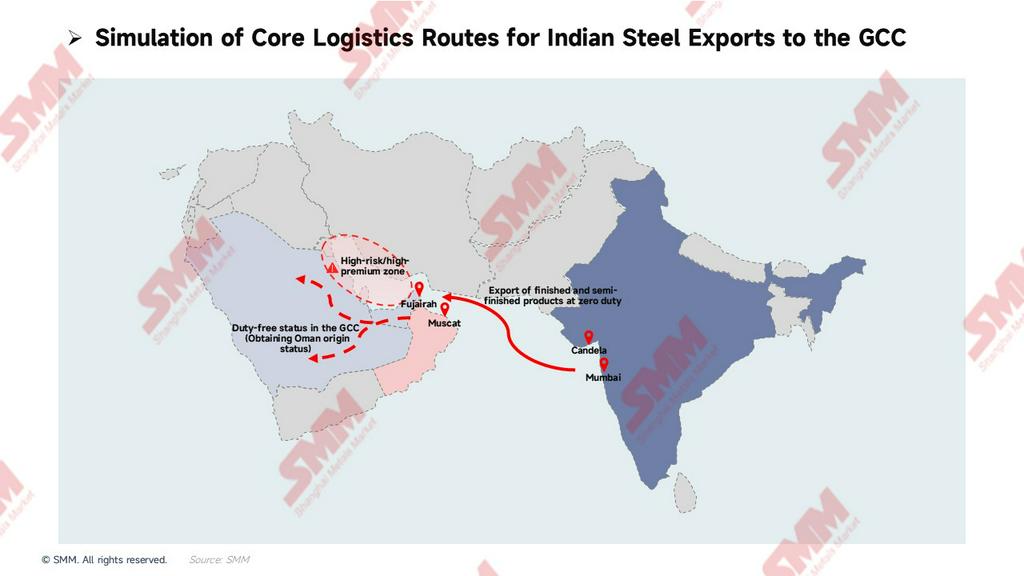

Core Alpha: Oman—the GCC’s “Rules-of-Origin Arbitrage” and Re-export Hub

Focusing solely on bilateral consumption is insufficient to see through this larger game. Oman's true strategic value lies in being the launching pad and legal channel through which Indian steel can penetrate the GCC heartland (Saudi Arabia, UAE).

- Geopolitical hedging and the “sea-to-land” multimodal logistics advantage: In recent years, to avoid potential political friction around the Strait of Hormuz, military risks, and the elevated war-risk insurance premiums inside the Persian Gulf, an increasing volume of bulk steel cargo has departed from traditional shipping routes, decisively choosing to discharge at deep-water ports outside the Strait. Against this backdrop, the UAE's Port of Fujairah and Oman's Port of Muscat—superbly positioned on the Arabian Sea—have firmly established their strategic role as the core receiving nodes for westward-bound South Asian steel. After Indian steel ships directly from Mumbai or Kandla and discharges at these outside-the-Strait ports, the cargo is broken into smaller consignments and efficiently transshipped overland by heavy-truck fleets into Saudi Arabia, the UAE interior, and Qatar. This “sea-to-land” logistics restructuring not only severs the uncontrollable risk of entering the Persian Gulf but also substantially compresses total lead times, providing end customers with exceptionally strong supply-chain certainty.

- Semi-finished value-added arbitrage under rules of origin (the core mechanism): In recent years, GCC countries such as Saudi Arabia and the UAE—to protect domestic capacity—have erected tariff and non-tariff barriers against directly imported finished steel. CEPA opens a legal and compliant bypass: India ships low-cost billets into Oman’s Sohar Free Zone, where standalone re-rolling mills perform secondary hot rolling; as long as value addition exceeds 30%, the steel can legitimately acquire “Made in Oman” origin status. The material can then enter Saudi Arabia and the UAE heartland as a GCC member-state product at zero tariff, neatly circumventing trade remedy measures.

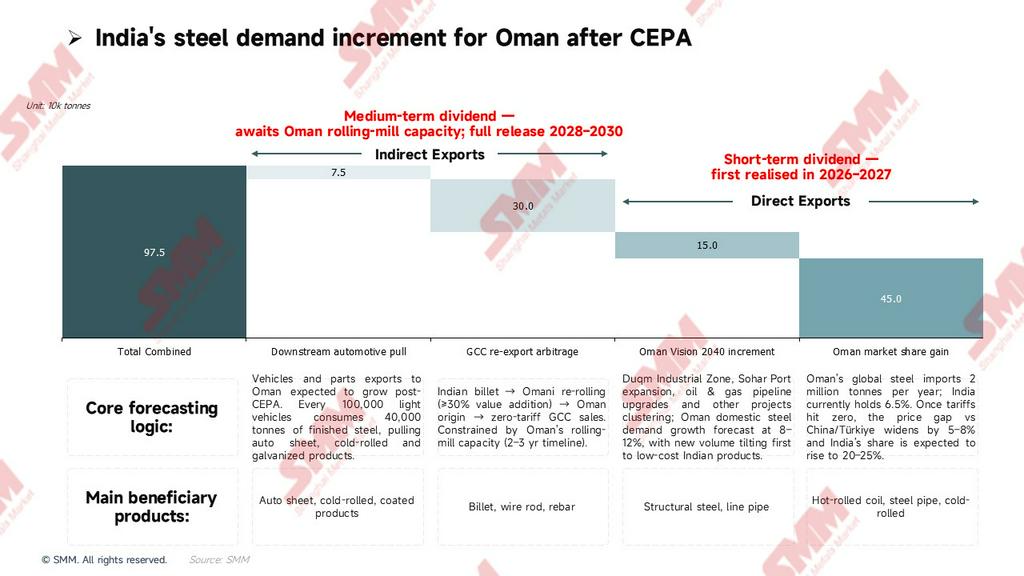

Demand Increment Forecasting: A Two-Layer Quantitative Framework of Direct + Indirect Exports

Building on the dual profit safety cushion of “tariff + exchange rate” and the “rules-of-origin re-export arbitrage” logic outlined above, we have constructed a two-layer quantitative forecasting model. To be clear, this model estimates the “incremental” pure new volume space brought by CEPA's implementation.

- Direct export increment (market-share gains + new infrastructure): Based on 2025 figures, India already accounts for approximately 6.5% (170,000 tonnes) of Oman's roughly 2.6-million-tonne total import basket. As CEPA's zero tariff widens the price advantage further—extending the price gap against competing Chinese/Turkish products by 5%–8%—India’s market share is expected to climb rapidly into the 20%–25% range in the medium term. Combined with incremental demand released by Oman's “Vision 2040,” this is projected to create an additional approximately 600,000 tonnes of direct export increment, driven primarily by hot-rolled coil, steel pipes, and cold-rolled products.

- Indirect export increment (re-export arbitrage + downstream pull): Leveraging “Made in Oman” origin status to tap into Saudi Arabia's USD 600-billion-scale infrastructure demand, combined with auto parts exports pulling demand for high-end supporting sheet products, this deeper-water dividend is expected to contribute an additional approximately 375,000 tonnes of indirect increment.

Taken together, on top of the existing historical base of 170,000 tonnes, a total increment as high as 975,000 tonnes—once fully released—will systematically lift the overall volume of India–Oman bilateral steel trade.

SMM forecasting notes and release timeline:

- Phase 1 (2026–2027) – Direct exports first: A combined 600,000 tonnes from “Oman market-share gains” and “Vision 2040 increments” rests on the direct price advantage from zero tariffs; this short-term dividend will be realized first and rapidly within 1–2 years after CEPA takes effect.

- Phase 2 (2028–2030) – Indirect exports awaited: A combined 375,000 tonnes from “GCC re-export arbitrage” and “downstream automotive pull”—constrained by the physical lead time for capacity build-out at Oman's standalone re-rolling mills (secondary processing)—belongs to medium-term logic. This dividend is expected to enter its full-release period only after capacity comes online progressively in 2028–2029.

Market Movements, Risk Warnings, and SMM End-Game Projection

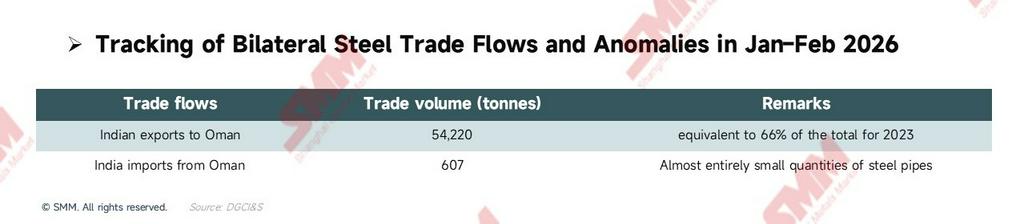

[Market movements: a “long-term contract lock-in” front-running wave in Q1]

Policy expectations always run ahead of fundamentals. In January–February 2026, customs-declared steel exports from India to Oman reached 54,220 tonnes (equivalent to 66% of the full-year 2023 volume). This sharply counter-seasonal “front-running” signal indicates that astute multinational traders have already begun practical positioning around the June zero-tariff milestone—pre-stocking at overseas warehouses and frequently signing longer-tenor supply long-term contracts with end customers.

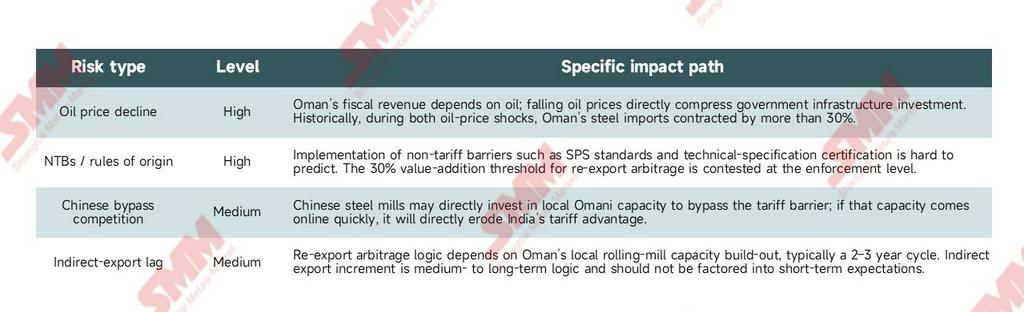

[Risk warnings: four constraints not to be overlooked]

Objectively, this trade dividend reshaping the Middle East landscape must still overcome four constraints:

[Conclusion: SMM end-game projection]

The India–Oman CEPA taking effect in June 2026 is by no means a paper-only bilateral concession; it is a critical springboard for India's steel and automotive manufacturing industries to reconstruct their market footprint across the Middle East and North Africa.

- Short term (2026–2027) – Capturing the direct-supply market: Acceleration of direct export orders (hot-rolled coil, steel pipes, cold-rolled) is the most certain outcome. On top of the 2025 base of 170,000 tonnes, as the direct export dividend is progressively realized, annualized total exports in 2026–2027 are expected to leap first into the 400,000–500,000-tonne tier.

- Medium term (2028–2030) – Full release of re-export arbitrage: As standalone rolling-mill capacity at Oman's Sohar/Duqm free zones is built out progressively, approximately 375,000 tonnes of “indirect re-export increment” will be fully activated. At that point, the triple stack of “170,000-tonne historical base + 600,000-tonne direct new increment + 375,000-tonne indirect new increment” will systematically elevate bilateral trade volumes, pushing India's annual exports to Oman historically past the 1-million-tonne threshold.

Under this triple-driver resonance of [rupee depreciation + tariff elimination + rules-of-origin arbitrage], enterprises that position themselves early at Oman's logistics and processing nodes will capture the most lucrative excess returns of this era in the contest to reshape regional pricing power.

![[SMM Steel] Brazil Steel Import Quota Utilization Reaches 60% Average Rate](https://imgqn.smm.cn/usercenter/ocJKj20251217171717.jpg)

![[SMM Steel] Nucor Opens Lexington Rebar Micro Mill in North Carolina](https://imgqn.smm.cn/usercenter/SEwWP20251217171716.jpg)

![[SMM Steel] SSAB Supplies Decarbonized Steel for Vattenfall Solar Project in Germany](https://imgqn.smm.cn/usercenter/CrEsY20251217171716.jpg)