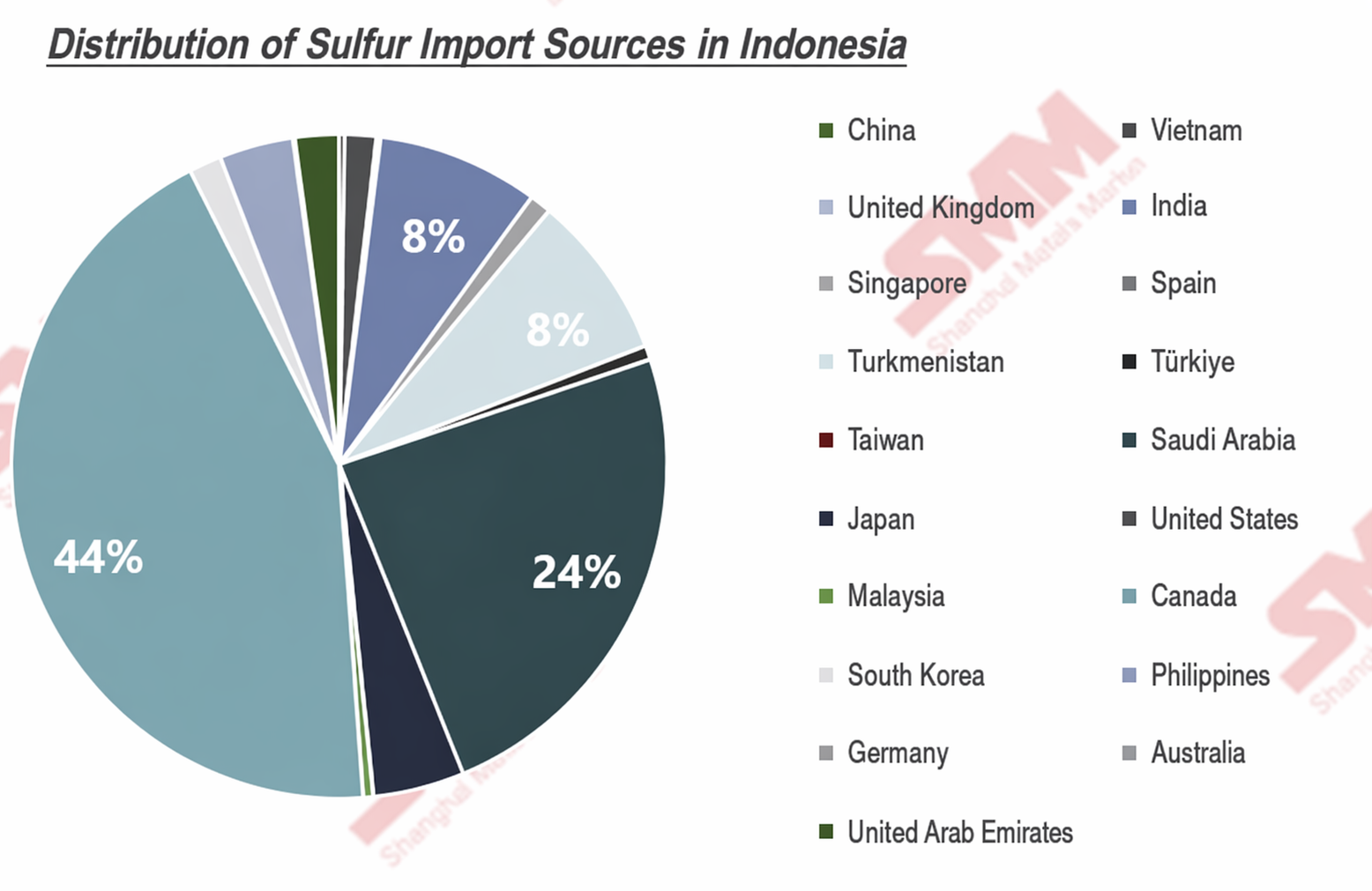

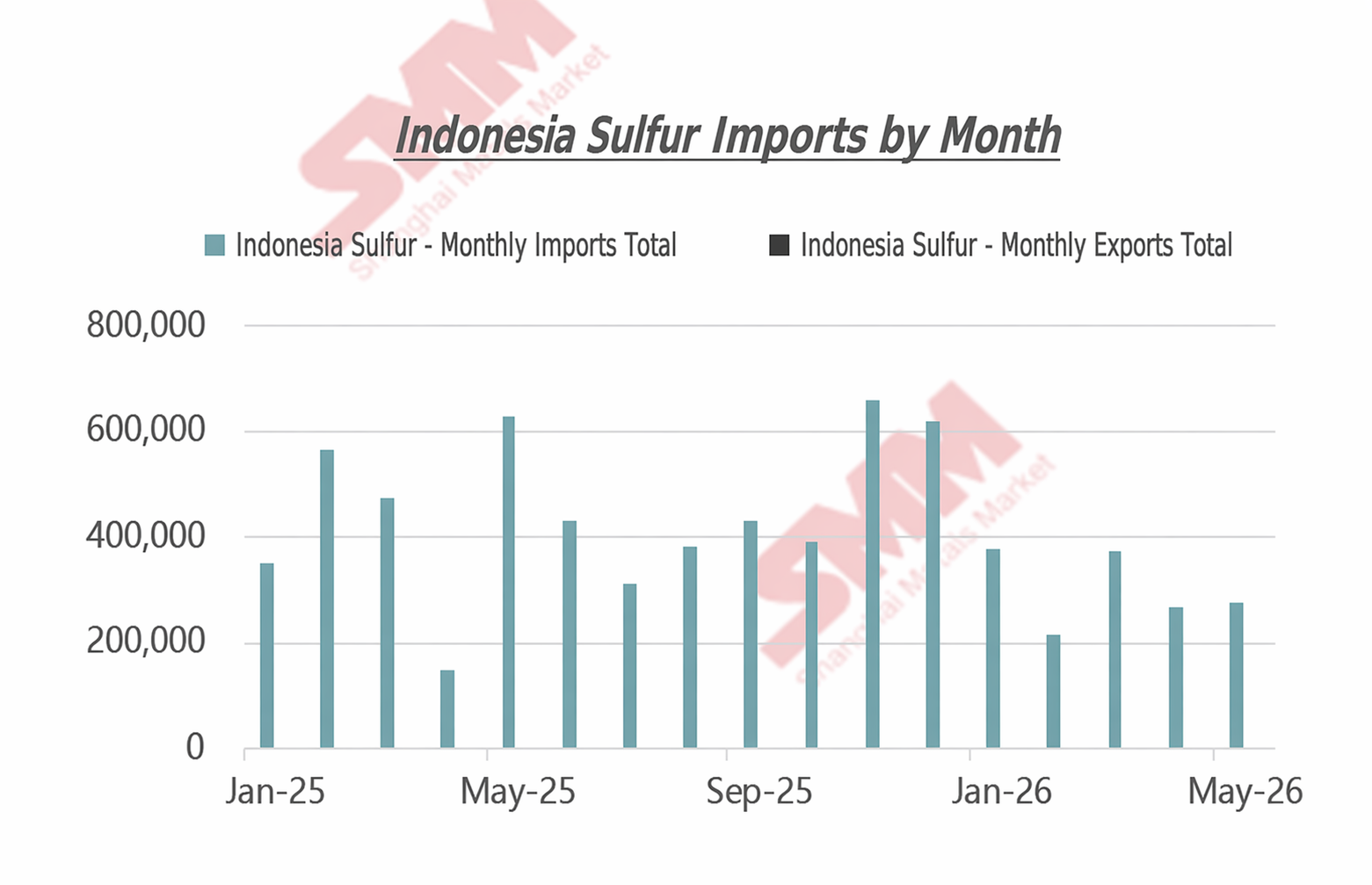

In May 2026, Indonesia's total monthly sulfur import volume was 277,834.30 mt in physical content, up 3.9% MoM and down 55.80% YoY, with major import sources including China, Vietnam, the UK, India, Singapore, Spain, Turkmenistan, Turkey, Saudi Arabia, and Japan, among others;

Indonesia's total monthly sulfur export volume was 24.08 mt in physical content, with major export destinations being Germany, Hong Kong (China), and the US;

Indonesia's total monthly sulfuric acid import volume was 55,296.994 mt in physical content, down 68.1% MoM and up 236.6% YoY, with major import sources being China, India, and South Korea;

Indonesia's total monthly sulfuric acid export volume was 0

![[SMM Analysis] VC Supply-Demand Tight Balance Persists in the Short Term, Huasheng's 60,000 mt Project Adjustment May Reshape the Industry's Long-Term Competitive Landscape](https://imgqn.smm.cn/usercenter/JmyWy20251217171729.png)

![[SMM Cobalt Morning Meeting Summary] Raw Material Prices Pulled Back, Ternary Cathode Material Fell Under Pressure](https://imgqn.smm.cn/usercenter/eGQFu20251217171723.jpeg)

![[SMM Cobalt Lithium Morning Meeting Summary] Raw Material Prices Under Pressure; Battery Production Schedules Continue to Grow](https://imgqn.smm.cn/usercenter/PPLUj20251217171727.jpg)