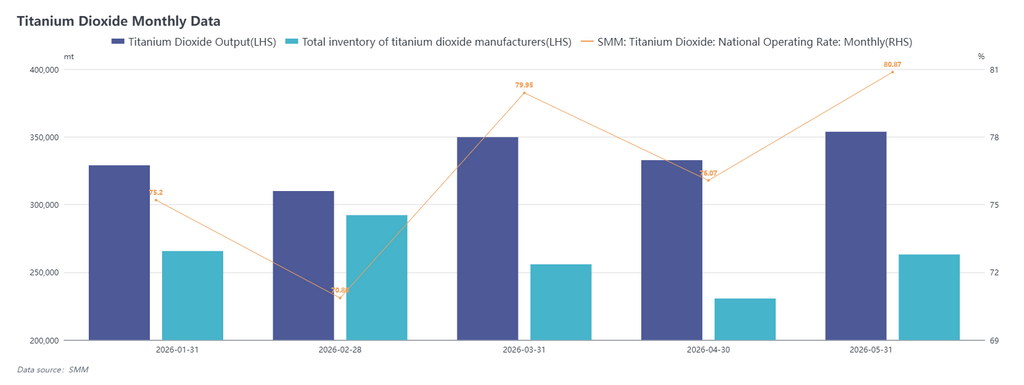

Titanium Dioxide Market Review for June: Price Divergence, High Cost Pressure, and Possible Supply-Demand Adjustment in July

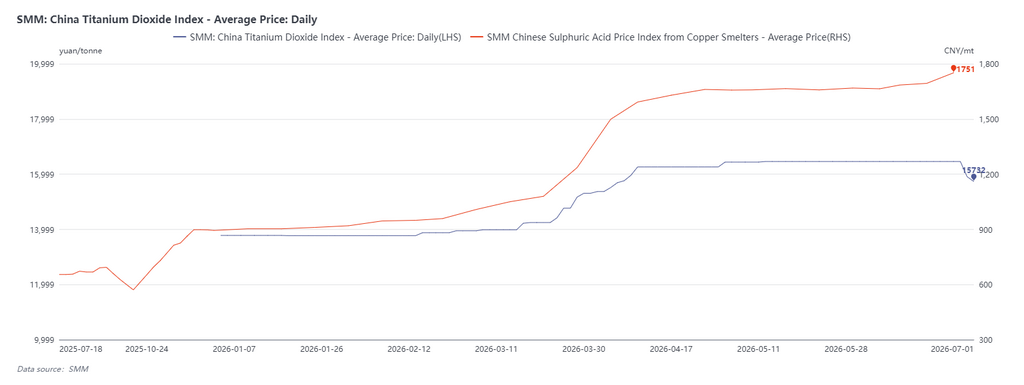

As of July 1, 2026, the SMM China titanium dioxide index closed at 15,732 yuan/mt, down 4.4% from early June. The titanium dioxide market operating rate remained high at 78.67% in June, with production down 2.72% MoM and producer inventory down 5.4% MoM. Customs data showed that titanium dioxide exports in May 2026 stood at 152,800 mt, down 21.05% MoM, while cumulative YoY growth was still up 12.55%.

Price trends for titanium dioxide diverged markedly in June. Early in the month, rutile titanium dioxide producers, mainly in the Panxi region, took the lead in cutting prices to 14,000–15,000 yuan/mt, while mainstream quotations from producers in east China were still maintained at 15,500–16,500 yuan/mt. Supply-demand wise, after high prices in Q1 2026, downstream end-users such as plastics and coatings had engaged in panic stockpiling earlier. With the arrival of the summer off-season, order demand began to weaken visibly from late May, market sentiment turned cautious, and some Panxi producers started to lower prices to secure order sales.

Cost side, sulphuric acid prices remained elevated in June, keeping raw material cost pressure unabated. Meanwhile, ferrous sulphate prices fell in late June, causing by-product losses for titanium dioxide. The cost burden on top-tier players increased, yet their willingness to hold prices firm actually strengthened. As cost pressure transmitted to producers that had cut prices, the market transaction center shifted slightly upward in late June.

Looking ahead to July, impacted by summer maintenance and cost pressure, titanium dioxide enterprises are expected to see widespread production cuts, leading to a tightening on the supply side. On the demand side, the market is still digesting earlier inventories. Wait-and-see sentiment may persist amid ongoing soft prices, but current coatings and plastics market inventory is less than two months’ worth, suggesting some restocking expectations. The titanium dioxide market is expected to enter an adjustment phase in July with both supply and demand weak; prices are likely to stay stagnant and gradually return to a cost-driven logic.

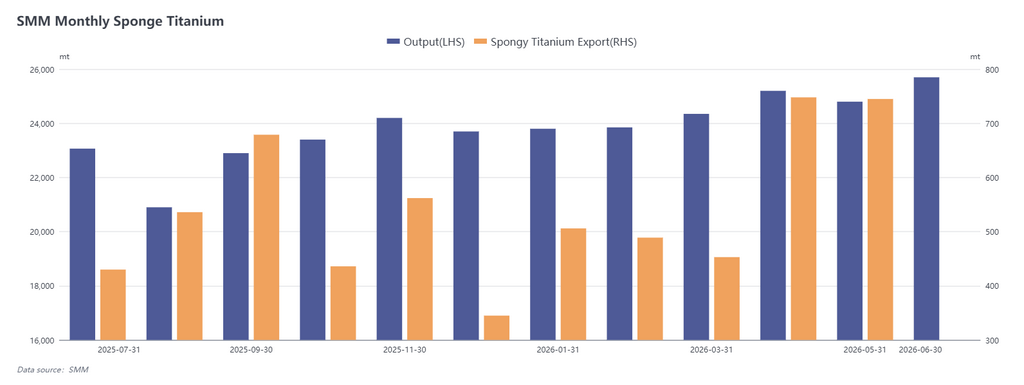

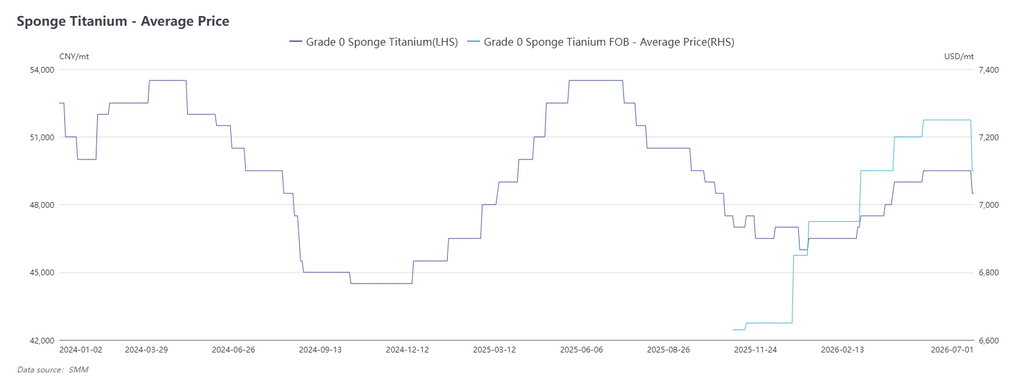

Titanium Sponge Market Review for June: Weakening Demand Pressures Prices, with Modest Recovery Possible in Q3

As of July 1, 2026, the SMM grade-0 titanium sponge price closed at 48,000–49,000 yuan/mt, down 2% from early June. Titanium sponge production in June 2026 was approximately 25,700 mt, with cumulative YoY growth of 11.04%. Customs data showed that titanium sponge exports in May reached 745 mt, down 7.52% YoY on a cumulative basis.

Titanium sponge prices declined somewhat in June, mainly affected by overall softening on the demand side. On exports, high oil prices continued to push ocean freight rates upward, and alongside stricter export controls to Japan, titanium material exports dropped notably, dragging on titanium sponge demand. In domestic trade, end-user projects remained in the construction phase, with no new incremental titanium applications materializing, and coupled with the traditional summer demand off-season from July to August, the market overall performed weakly.

Looking ahead to H2, titanium metal market is likely to move sideways. With demand gradually recovering in Q3, titanium sponge prices are expected to return to around 50,000 yuan/mt, but whether the uptrend can be sustained will depend on the boost from new demand.