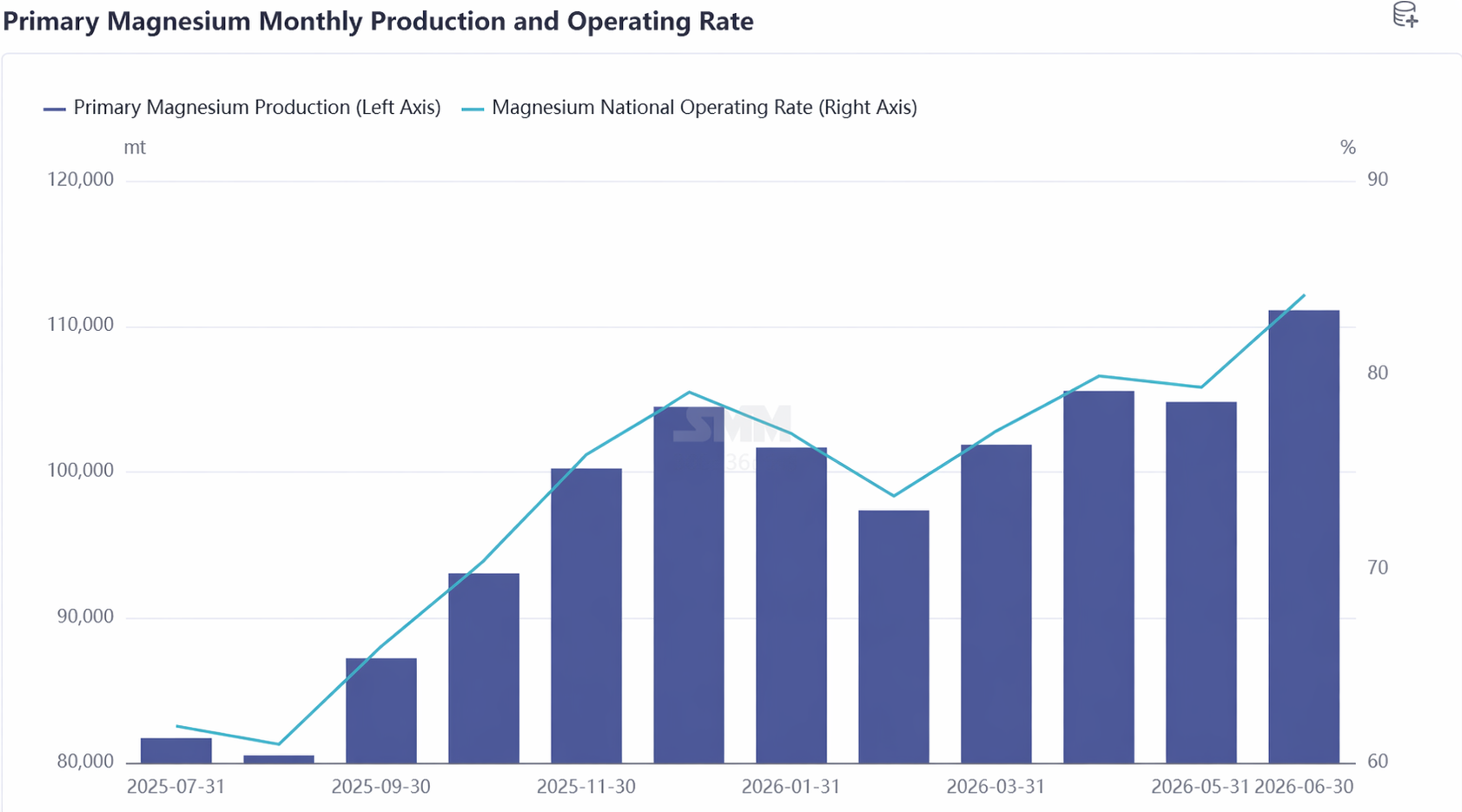

Looking back at China's magnesium market in H1 2026, the previous pattern of strong supply and weak demand quietly reversed due to concentrated production suspensions at magnesium plants earlier in the period. Tight spot supply and low inventory created solid foundations for a phased upward move in the magnesium ingot market, while news-driven factors such as surging magnesium alloy demand further stirred the market. Speculative demand emerged abruptly, with robust purchasing enthusiasm lifting magnesium prices in a stepwise fashion during Q1. Excessively high expectations fueled production zeal among magnesium plants, driving output steadily higher. By June 2026, China's primary magnesium production had climbed to 110,000 mt. The sustained rise in output intensified sales pressure on magnesium plants; with both inventory and production increasing, magnesium prices trended downward in a stepwise manner during Q2. Overall, magnesium prices traced an inverted V-shape in H1.

Review of Primary Magnesium Production in H1

Primary magnesium production in H1 2026 showed a consolidating upward trend, with output increases led by provinces such as Shaanxi, Anhui, and Xinjiang. The operating rate for primary magnesium production in Shaanxi stabilized above 85%. By June 2026, Shaanxi's primary magnesium production had climbed to around 70,000 mt.

Primary magnesium production in June rose 5.97% MoM, a notable increase in China's monthly output. On the supply side, production at smelters across major producing regions rose in tandem, driven by two main factors: first, enterprises sought to lower per-mt comprehensive costs for magnesium ingot by operating at full capacity to spread fixed production costs; second, integrated enterprises along the entire industry chain maintained production scale to secure internal raw material supply. As a result, the industry's overall operating rate edged up.

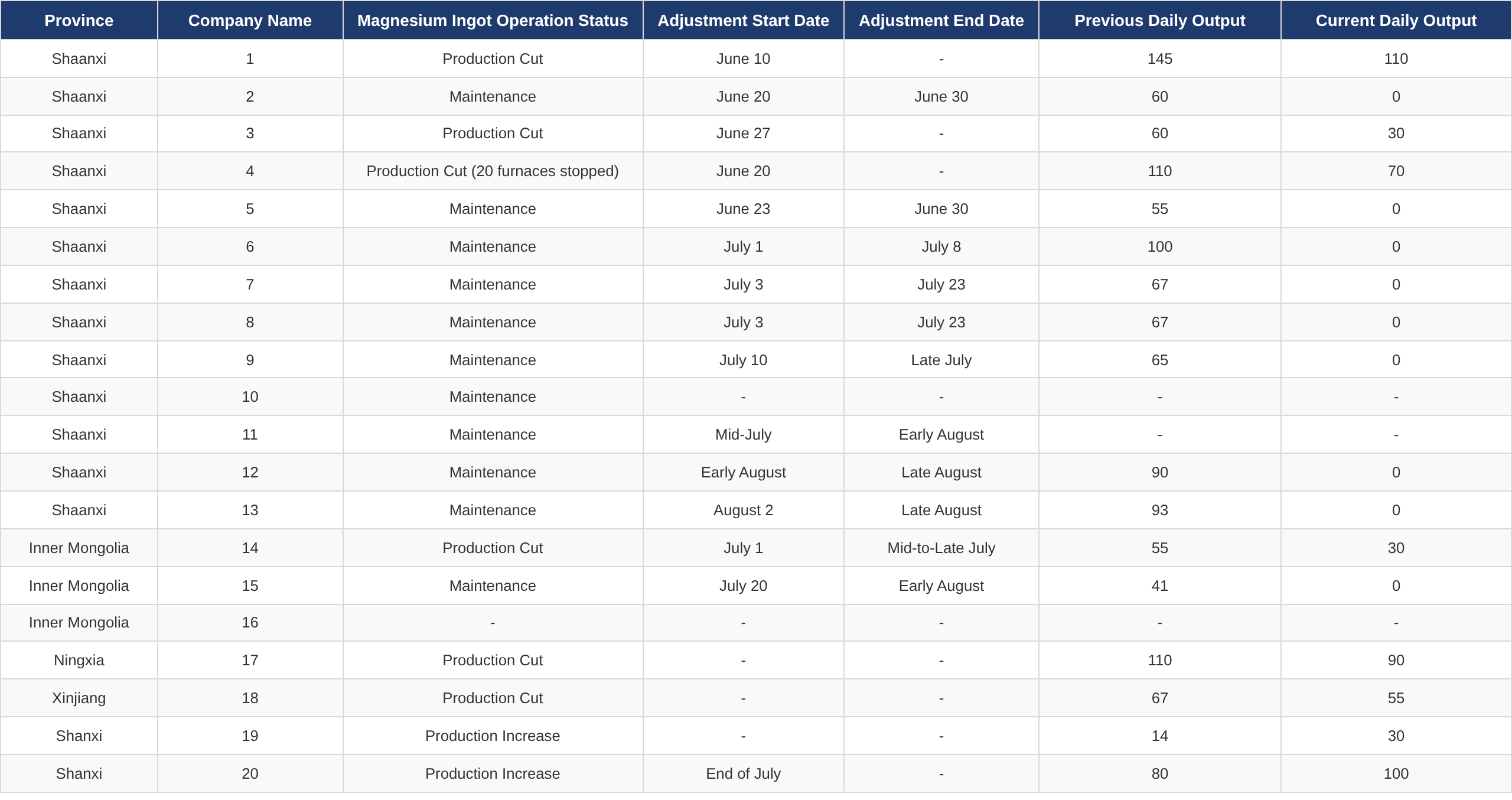

As the high-temperature summer sets in, maintenance plans at primary magnesium smelters are being implemented successively, gradually shifting market focus to expectations of supply contraction due to production cuts. The market is currently in a delicate equilibrium of ample supply and weak demand. The core battleground for future magnesium prices will be a race against time between the supply contraction window from summer maintenance-related production cuts and the period of weakening external demand caused by summer breaks outside China.