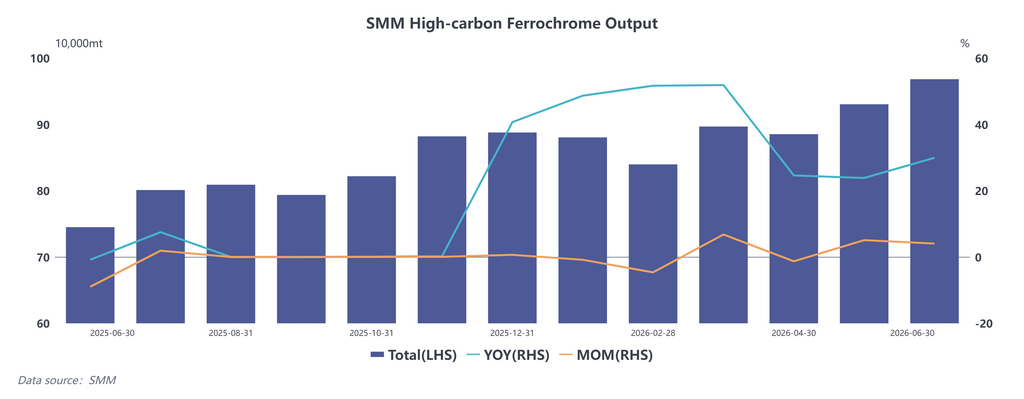

News Release, June 30, 2026:

According to SMM statistics, China's high-carbon ferrochrome output in June 2026 rose 4.06% month-on-month and 29.96% year-on-year.

Domestic ferrochrome output stayed elevated throughout the month, with production growth recorded in both northern and southern regions. In Inner Mongolia in the north, power supply constraints exerted limited impact. The June tender price for ferrochrome from steel mills stood at RMB 8,495 per 50-base-tonne. Meanwhile, chrome ore prices trended down moderately, lowering production costs for ferrochrome producers who maintained decent margins and mostly operated at normal run rates. In addition, newly launched capacity at several smelters further lifted regional output. Statistics show Inner Mongolia’s high-carbon ferrochrome output climbed 3.83% month-on-month in June, accounting for 77.82% of the national total.

The southern regions officially entered the wet season, with power tariffs falling notably in Sichuan, Yunnan and other provinces, prompting successive restarts and production resumptions. Combined high-carbon ferrochrome output across southern provinces including Sichuan, Guizhou, Guangxi and Hunan rose 10% month-on-month in June, representing 11.59% of national volume.

Ferrochrome output is expected to stay at high levels with little room for sharp further gains.

For one thing, major stainless steel mills including Tsingshan and TIS cut their July high-carbon ferrochrome tender prices by RMB 200 per 50-base-tonne month-on-month, matching the market’s earlier bearish sentiment. The sector is in the traditional off-season for consumption, with news of production cuts emerging among downstream stainless steel manufacturers. Market participants hold subdued confidence over the outlook, keeping ferrochrome prices under persistent downward pressure. Meanwhile, the decline in chrome ore prices has slowed, leaving limited room for further cost reductions and squeezing profit margins of ferrochrome producers, which dampens production willingness.

For another, southern smelters have mostly ramped up output to full capacity amid the wet season, leaving little upside for additional production growth. Besides, nearly all newly added domestic capacity has been commissioned. Therefore, ferrochrome output is projected to remain steady at current high levels in the near term.

![[SMM Analysis] Long-term contracts fail to change the loose supply pattern, and the price center of manganese sulphate is expected to be in the doldrums in the future market.](https://imgqn.smm.cn/usercenter/CIcRv20251217171725.jpg)

![[SMM Analysis] China's Ferrochrome Imports to Stay Low in the Short Term after Falling in May](https://imgqn.smm.cn/usercenter/jMeFI20251217171722.jpeg)