News Release, May 27, 2026:

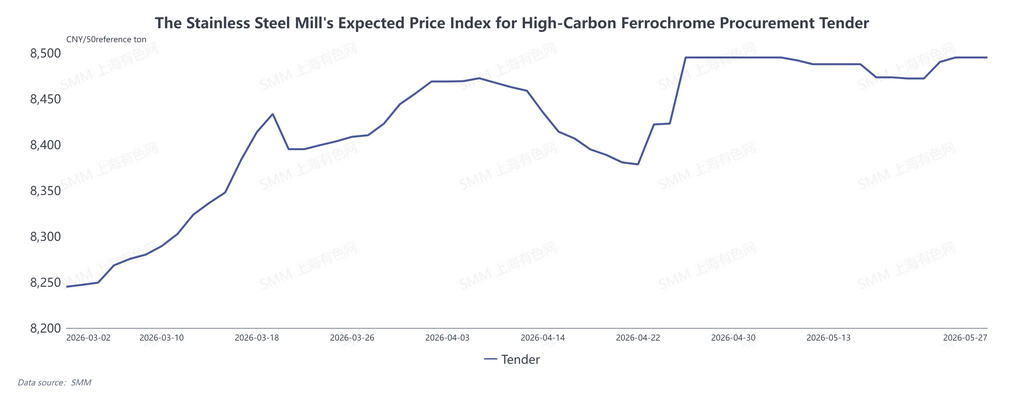

On May 22, TISCO announced its tender purchase price for high-carbon ferrochrome for June at 8,295 yuan per 50 metric base tons. Tsingshan Group set its price at 8,495 yuan per 50 metric base tons simultaneously. Both prices were unchanged month-on-month from May, largely in line with market expectations. Market sentiment has stabilized, and retail prices of ferrochrome have halted their decline and leveled off. Nevertheless, weighed down by three major factors — a slight surplus in supply, sluggish demand and continuously falling production costs — China’s ferrochrome market generally sees narrow price fluctuations and thin trading activity.

1. Steel mill tenders set price benchmark; spot prices fluctuate within a narrow range

The unchanged June tender prices by Tsingshan and TISCO matched market expectations, providing short-term bottom support for ferrochrome prices and putting an end to the previous prolonged gradual decline. As of May 27, mainstream spot quotations for domestic high-carbon ferrochrome stood at 8,250 to 8,450 yuan per 50 metric base tons, maintaining the pattern of lower prices in northern regions and higher prices in southern regions, while regional price gaps narrowed steadily. Specifically, quotations in Inner Mongolia ranged from 8,250 to 8,400 yuan per 50 metric base tons, and those in southern areas including Sichuan were quoted at 8,350 to 8,450 yuan per 50 metric base tons.

After the finalization of tender prices, price volatility in the retail ferrochrome market eased notably, yet trading activity remained sluggish and manufacturers’ market confidence improved only marginally. Downstream stainless steel producers posted decent overall profits and have no plans for equipment maintenance or production cuts, keeping output at a relatively high level. However, steel mills adopted a generally cautious purchasing stance and adhered to the principle of purchasing based on actual demand. Most transactions were for rigid demand, with large bulk orders scarce. Meanwhile, traders remained largely on the sidelines, resulting in a bleak retail trading atmosphere.

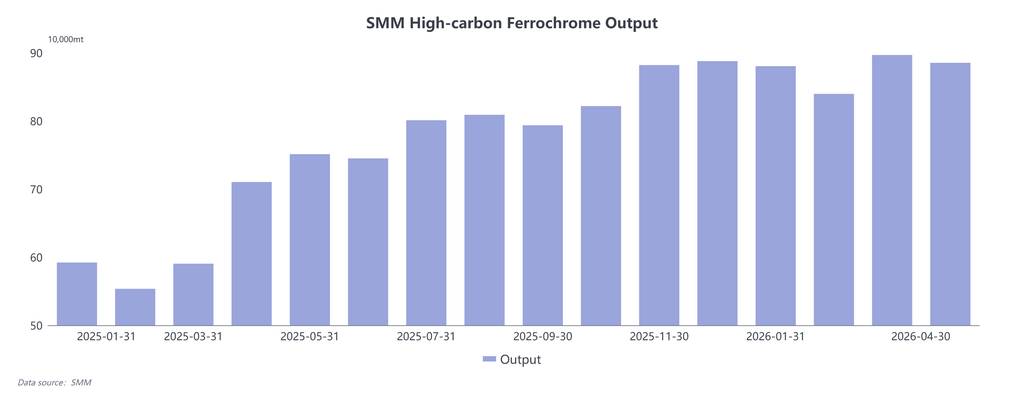

2. Gradual supply surplus emerges; production resumptions in the wet season add pressure

The ferrochrome market faces ample supply, with rising domestic output and steady import volumes. The growing supply surplus is expected to cap price gains. On one hand, falling chrome ore prices have reduced production costs for ferrochrome and mitigated the risk of price inversion. Supported by the stable tender prices, manufacturers maintained active production and overall output stayed at a high level with minor fluctuations. On the other hand, as regions such as Sichuan entered the wet season, electricity tariffs dropped markedly. Most ferrochrome producers plan to restart idle capacity, which will further lift domestic output.

In terms of imports, China Customs data showed that China imported 145,100 metric tons of high-carbon ferrochrome in April 2026, up 6.2% month-on-month but down 42.78% year-on-year. Although the total volume was lower than the same period in previous years, imports have seen a steady recovery. South Africa has rolled out temporary preferential electricity tariffs. Major chrome producers Glencore and Samancor have restarted part of their production facilities, driving up South Africa’s ferrochrome output. If the electricity tariff of 62 South African rand per kilowatt-hour takes effect, China will face growing import pressure, further exacerbating the supply surplus.

3. Chrome ore prices keep falling, weakening cost support at the bottom

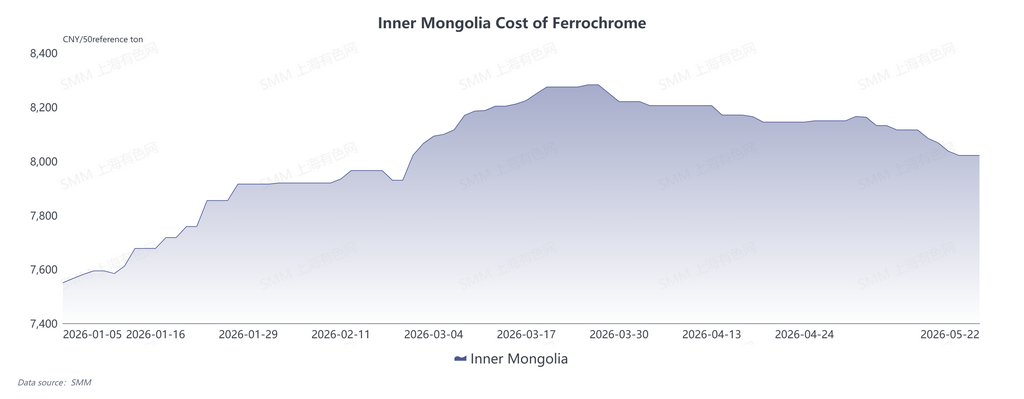

Continuous declines in upstream chrome ore prices have eroded the production cost base of ferrochrome. As of May 27, the spot price of 40-42% South African chrome ore fines at domestic ports stood at 56.5–58 yuan per unit of chromium content per metric ton, down 2 yuan month-on-month. Quotations for 48-50% Zimbabwean chrome ore fines were 58–60 yuan per unit of chromium content per metric ton, a month-on-month drop of 1.5 yuan. Overseas mainstream mine offer prices have fallen for three consecutive rounds to 300 US dollars per metric ton, with other types of chrome ore also sliding.

According to SMM data, the current spot smelting cost of high-carbon ferrochrome in Inner Mongolia fell by 2.6% month-on-month. The underlying cost support has weakened, leaving manufacturers reluctant to prop up prices. Coupled with weak downstream demand, ferrochrome prices trended downward moderately over the month.

4. Intensified market games; weak and stable trend to persist in the short term

The ferrochrome market currently maintains a loose supply-demand balance, with buyers and sellers locked in a standoff. The steady tender prices offered by major steel mills have delivered phased support to the market. Alongside the halted decline of chrome ore and stabilized costs, ferrochrome prices face limited risks of sharp drops in the near term. That said, the core issue of excess supply remains unresolved. As the market enters the traditional off-season for consumption, downstream stainless steel mills may cut production. Weakened demand will leave no effective driving force for ferrochrome price hikes, and the market will continue to see a weak and stable pattern.

![[SMM Analysis] Tantalum Prices Rebound on Positive News & Drained Low-Cost Inventory](https://imgqn.smm.cn/usercenter/eThpo20251217171723.jpeg)