I. DRC Export Quota Policy in H1 2026: Transition from Leniency to Standardization

|

Timeline |

Key Policies |

|

Jan 2026 |

ARECOMS allowed Q4 2025 cobalt export quotas to be extended to month-end March 2026 |

|

Mar 2026 |

The Ministry of Finance and the Ministry of Mines introduced controls to standardize deviations in cobalt hydroxide metal content detection |

|

Apr 2026 |

ARECOMS allowed Q4 2025 quotas to be extended to month-end April 2026, and Q1 2026 quotas to be extended to month-end June 2026 |

|

Jun 2026 |

ARECOMS revoked unused H1 2026 quotas |

In H1 2026, the DRC government steadily advanced the standardized operation of the cobalt export quota system. Initially, due to incomplete approval processes and standards, quota issuance efficiency was low, and the government allowed miners to extend unused quotas. As procedures matured, the government gradually shortened extension periods and officially announced the revocation of all unused H1 quotas at month-end June. The DRC government has not yet clarified the carryover rules for H2 quotas, leaving the market with two expected pathways: first, following the Q1 and Q2 approach with quarterly settlements where monthly quotas within a quarter can be flexibly transferred; second, reverting to the original 2025 quota document standards with monthly settlements that strictly prohibit inter-month carryover. This policy uncertainty remains a key supply variable for H2.

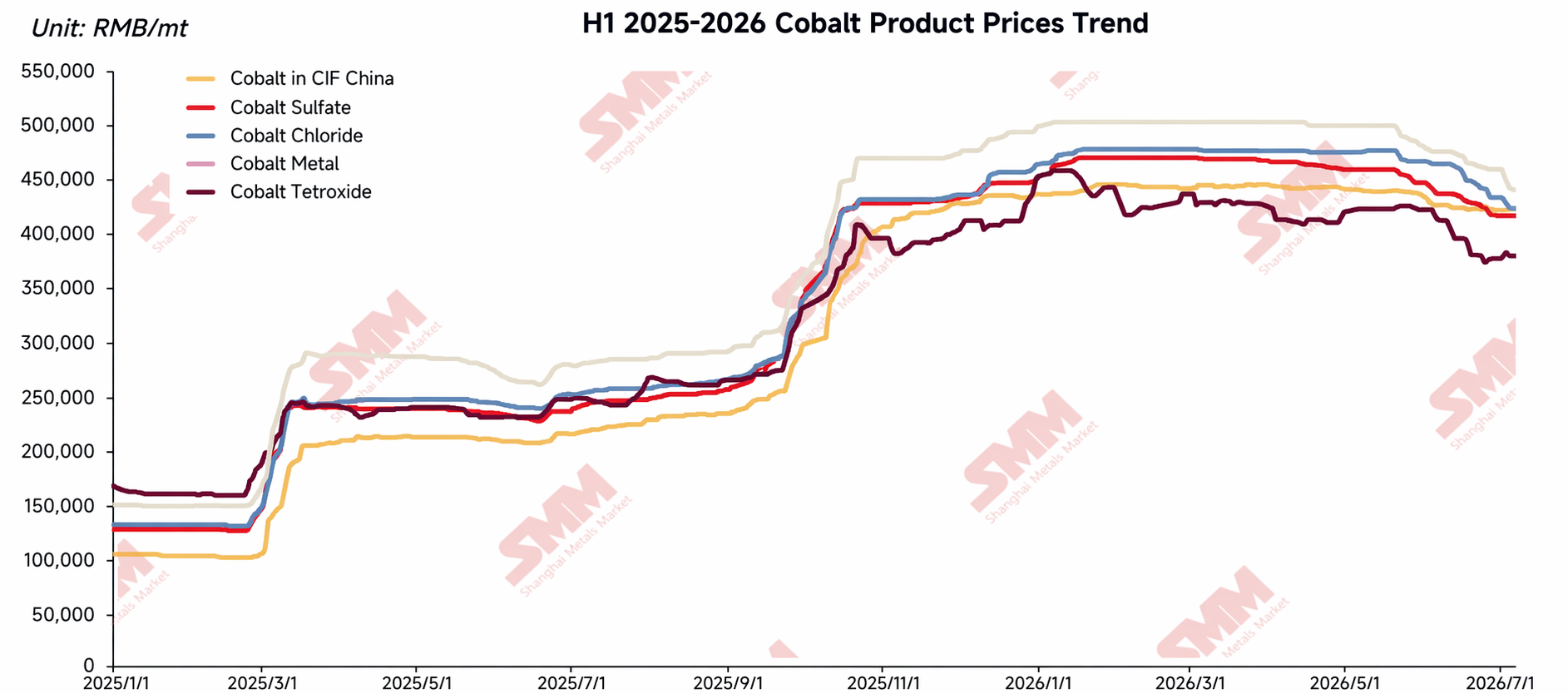

II. Cobalt Product Prices: Expectations Disappointed, Consolidation and Grinding Lower Through H1

At the start of 2026, the market widely anticipated that the quota system would tighten supply, providing a basis for higher cobalt prices. The actual trend proved the opposite, with overall mt in metal content prices for cobalt products drifting lower .

In January, refined cobalt surged then pulled back sharply, weighed by profit-taking, weakening macro sentiment, and broad declines in base metals, before stabilizing at relatively low levels. Other cobalt products did not drop significantly due to stronger raw material cost support but lacked upward momentum and entered a sideways state.

From February to March, boosted by positive news, refined cobalt prices briefly rebounded but then re-entered a grind lower channel, pressured by overseas market arbitrage activity, sluggish end-user restocking demand, and financial constraints. Downstream enterprises maintained extremely low raw material inventory, purchasing only as needed. Divergence in the cobalt salt market intensified: upstream held prices firm on bullish expectations, with only some financially constrained enterprises selling at discounts; downstream rejected high-price purchases without order backing, resulting in sluggish transactions. Prices remained broadly steady but biased weaker.

From April to May, downstream production schedules and orders continued to underperform expectations. Coupled with relatively sufficient raw material inventories at most enterprises, purchase willingness remained sluggish, with only occasional small-volume deals at low prices. On the supply side, most smelters held prices firm due to high raw material costs, but some recycling smelters and traders cut prices to sell under financial pressure, causing prices to grind lower gradually.

In June, the market extended its downtrend, with the price center of all products moving lower. Refined cobalt saw weak end-use demand, while some enterprises faced pressure from mid-year financial reporting and cash collection, leading to persistent selling in spot cargo and futures markets, putting notable downward pressure on prices. Cobalt salts were impacted by weakening production schedules for downstream ternary cathode precursors and Co3O4, with procurement limited to immediate needs and aggressive price pushing, causing transaction centers to decline continuously. Cobalt intermediate products weakened slightly amid the standoff between miners’ firm pricing and sluggish purchasing by domestic smelters, with the decline milder than that of cobalt salts, further squeezing smelting margins.

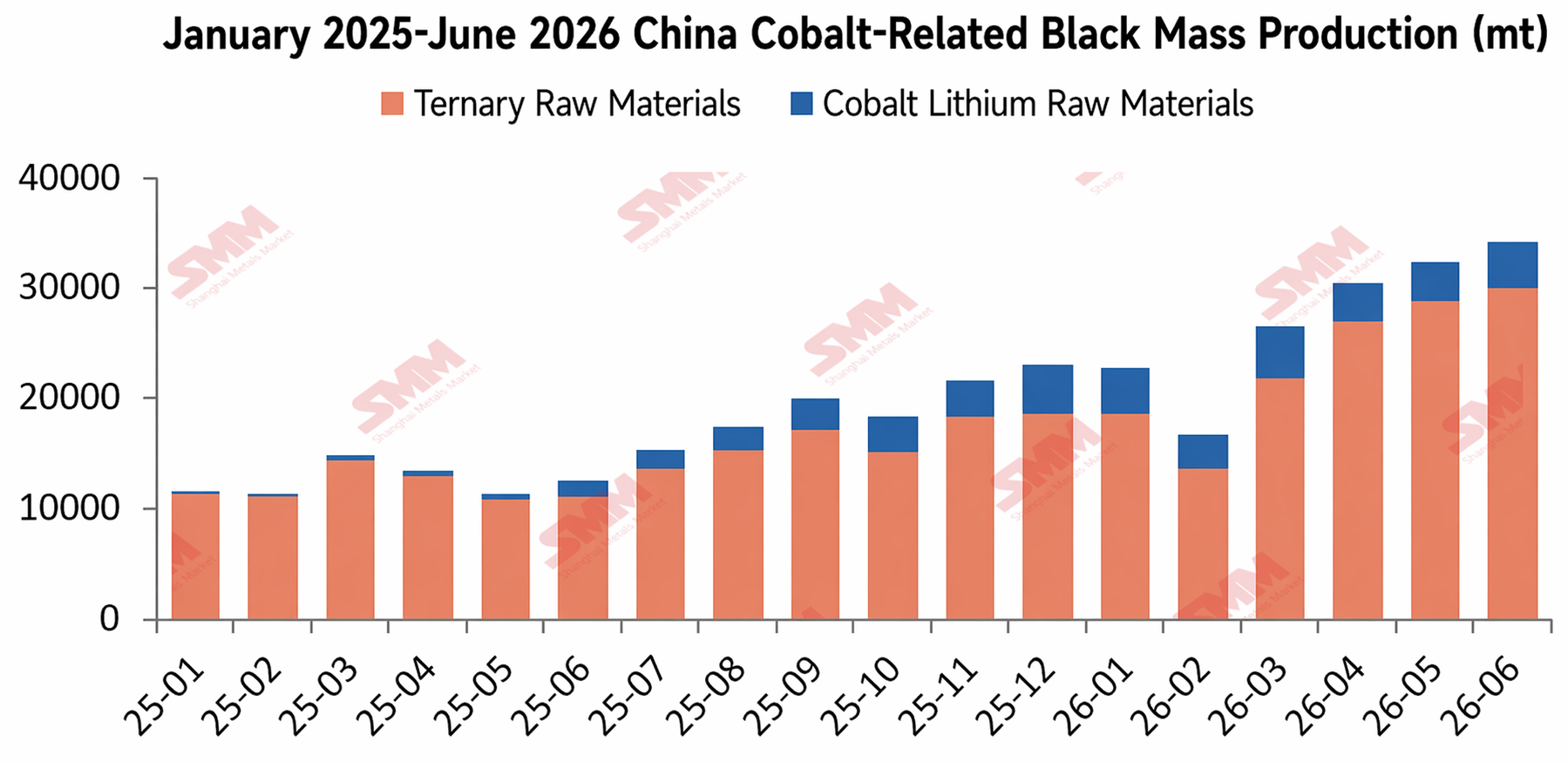

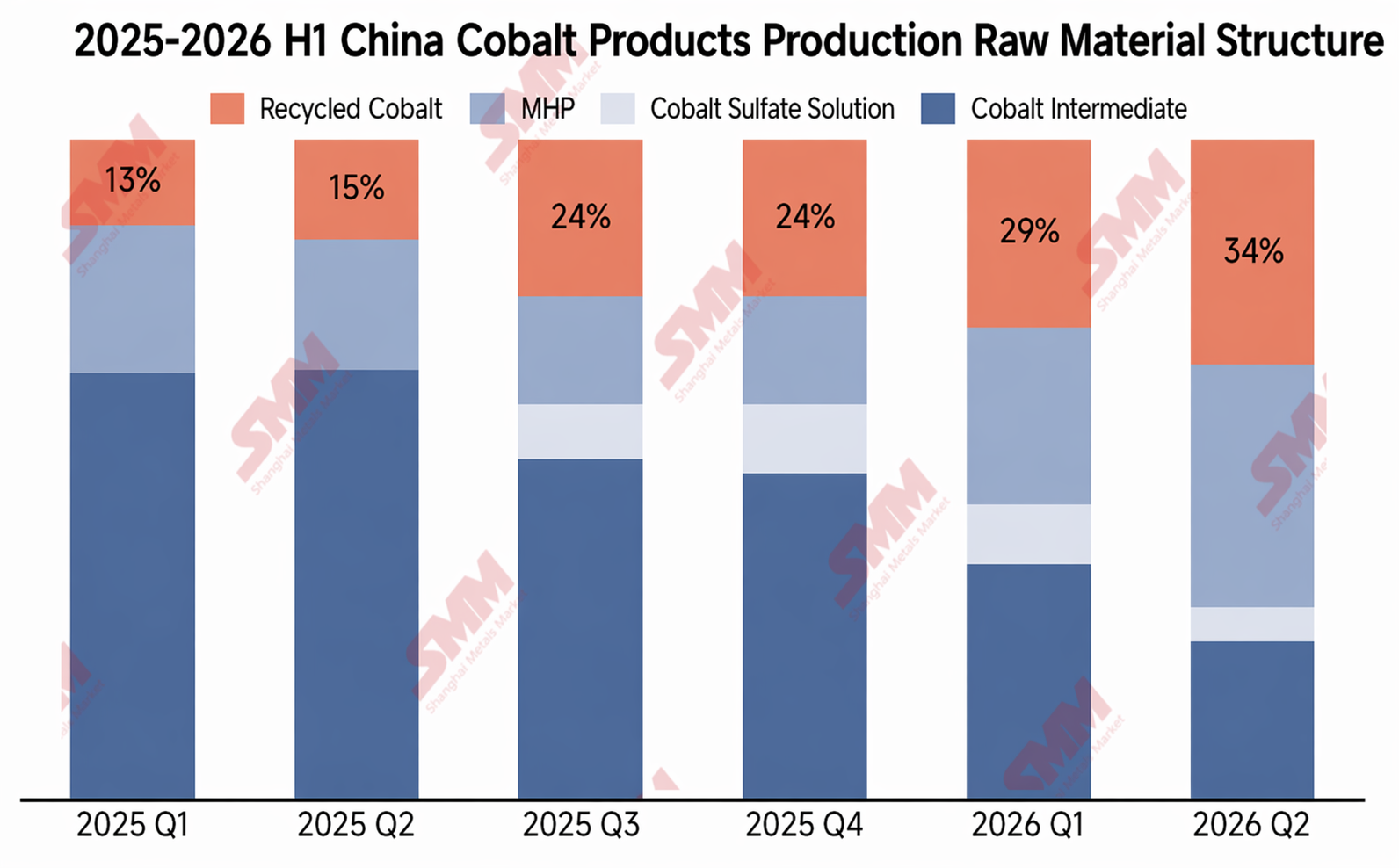

The core logic behind the price decline was a supply-demand mismatch: On one hand, while primary raw materials remained tight, supply from recycling increased substantially. SMM data shows that China’s recycled cobalt salt production (including in-house recycling by battery cell manufacturers) was only approximately 2,000–2,500 mt in metal content in June 2025, surging to around 4,000–4,500 mt in metal content by June 2026, effectively filling the gap in intermediate products. The share of recycling in the cobalt raw material production structure rose from approximately 13% in Q1 2025 to around 34% in Q2 2026. On the other hand, demand was sluggish. SMM estimates that LCO production in 2026 is expected to decline 22% MoM, with downstream purchasing as needed and destocking proceeding slowly. The restocking rally the market had been anticipating never materialized. Against this supply-demand mismatch, the cobalt market remained buyer-dominated over the long term, with prices weakening gradually.

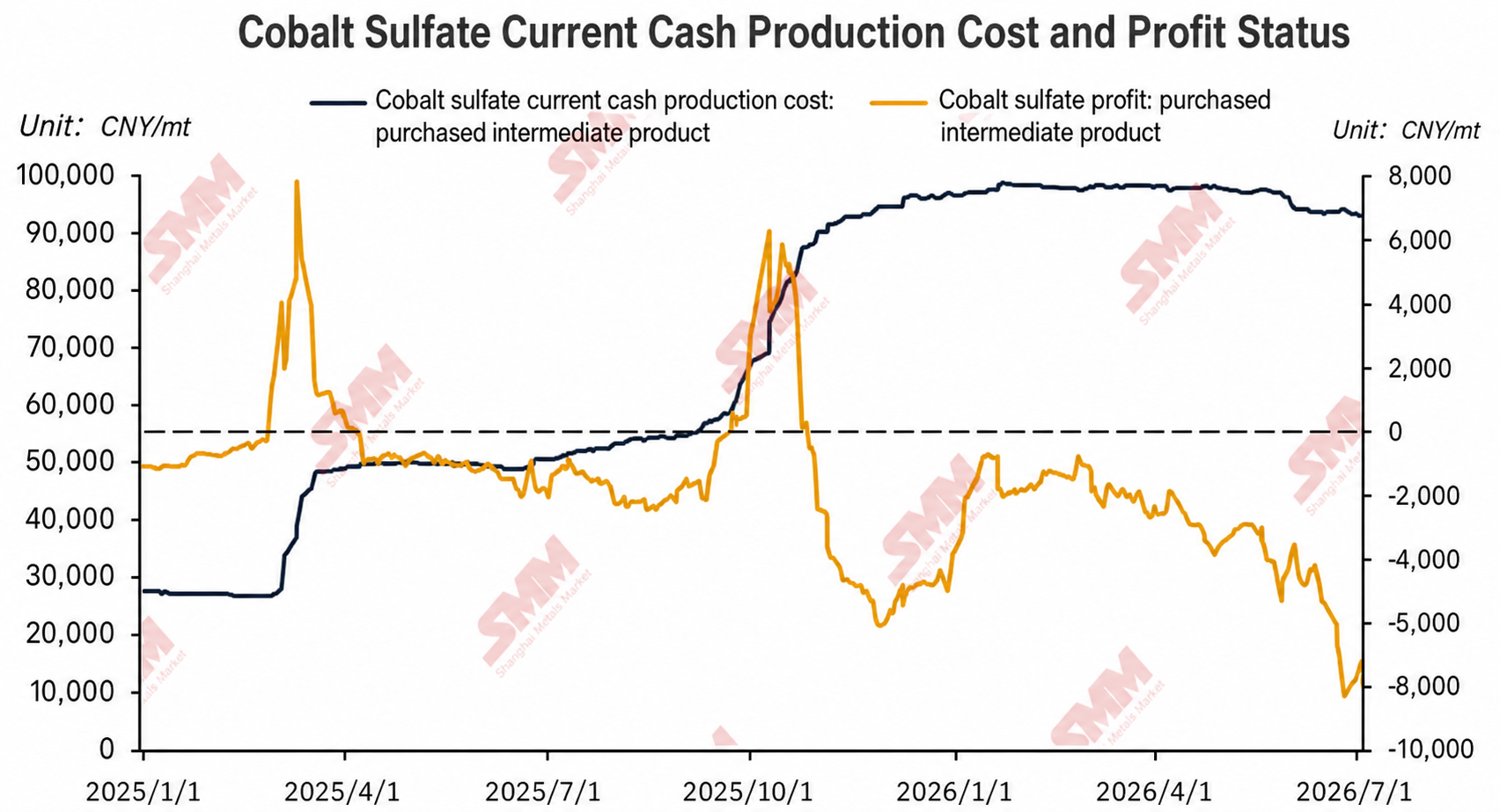

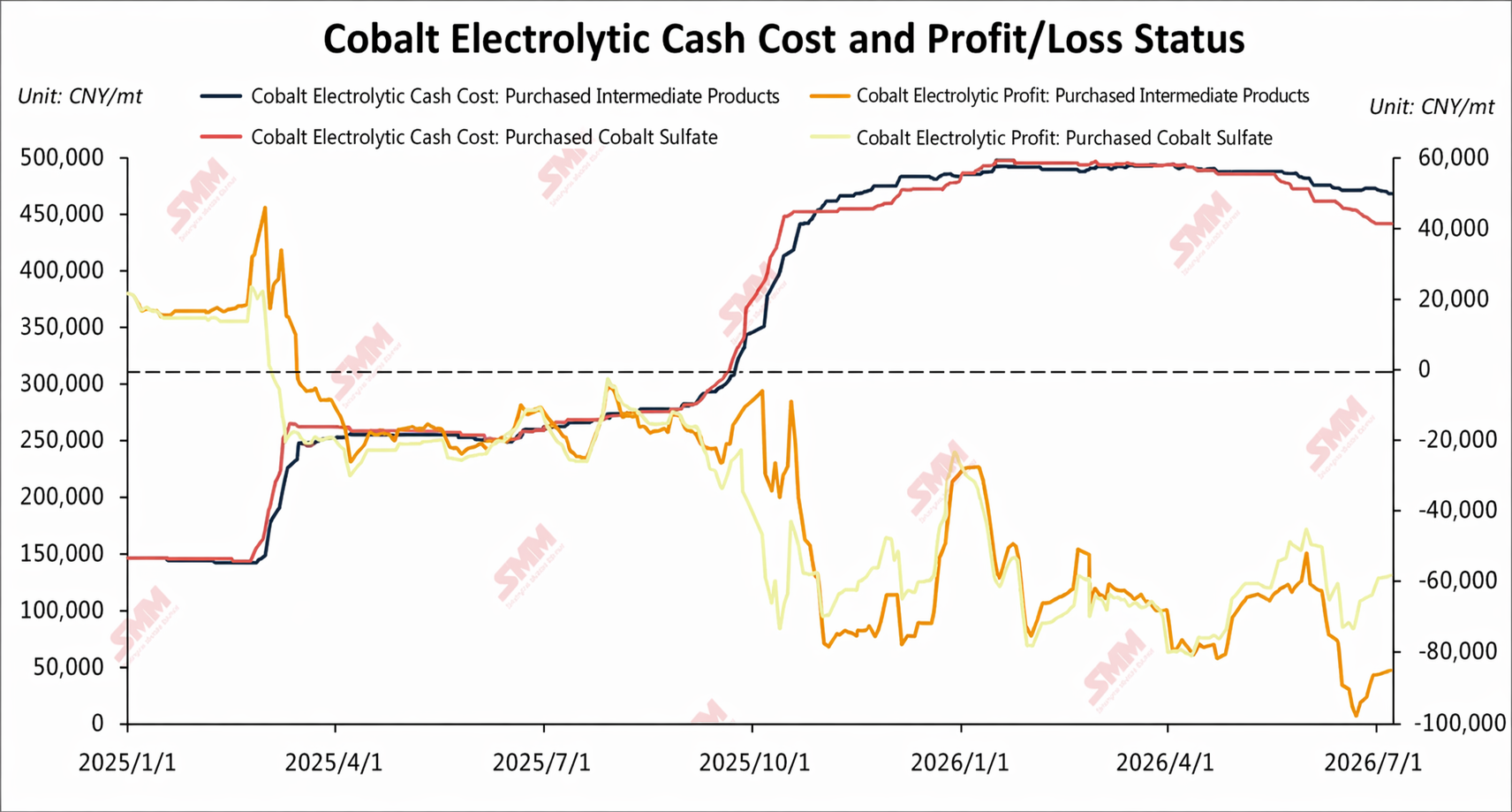

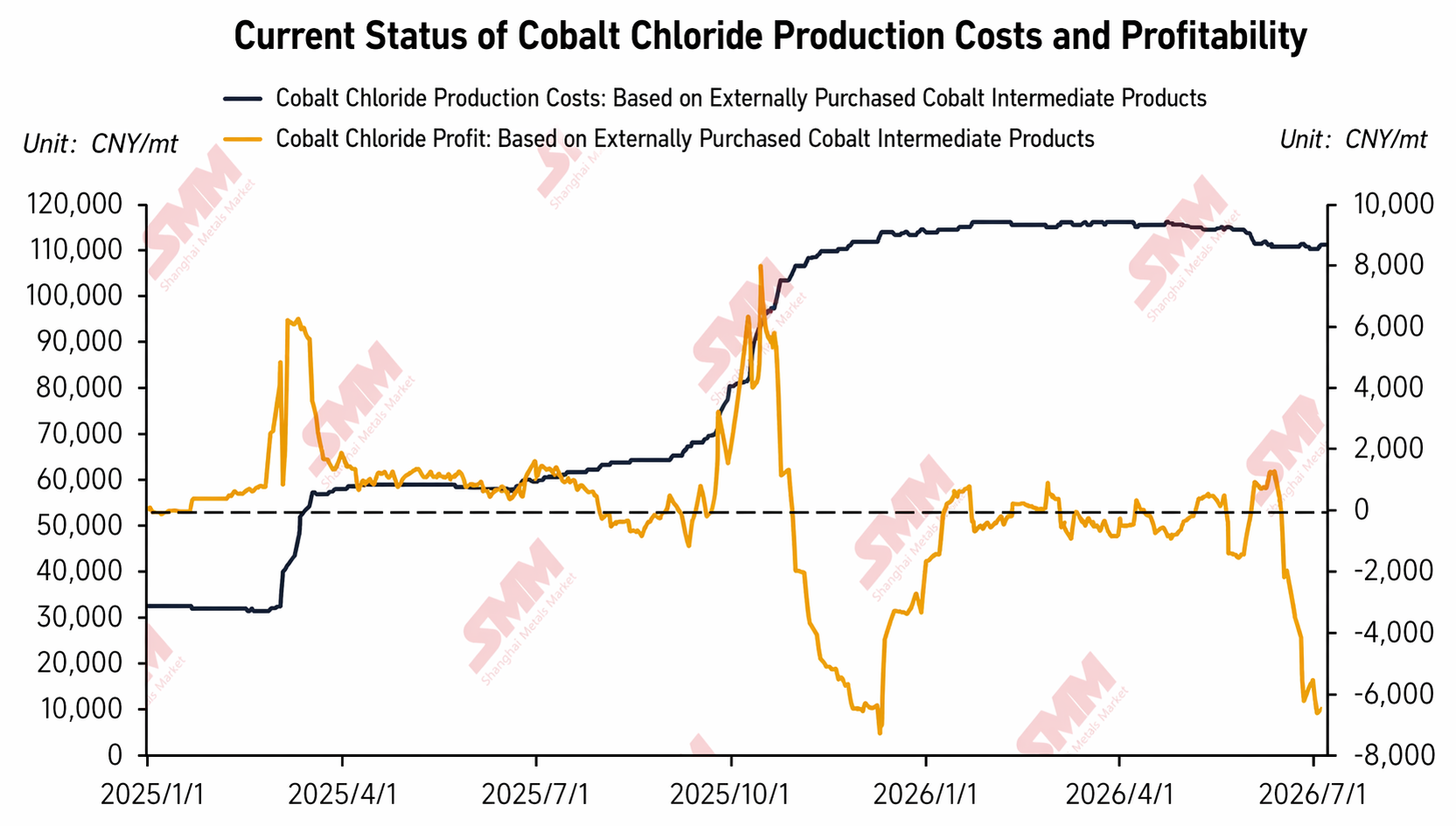

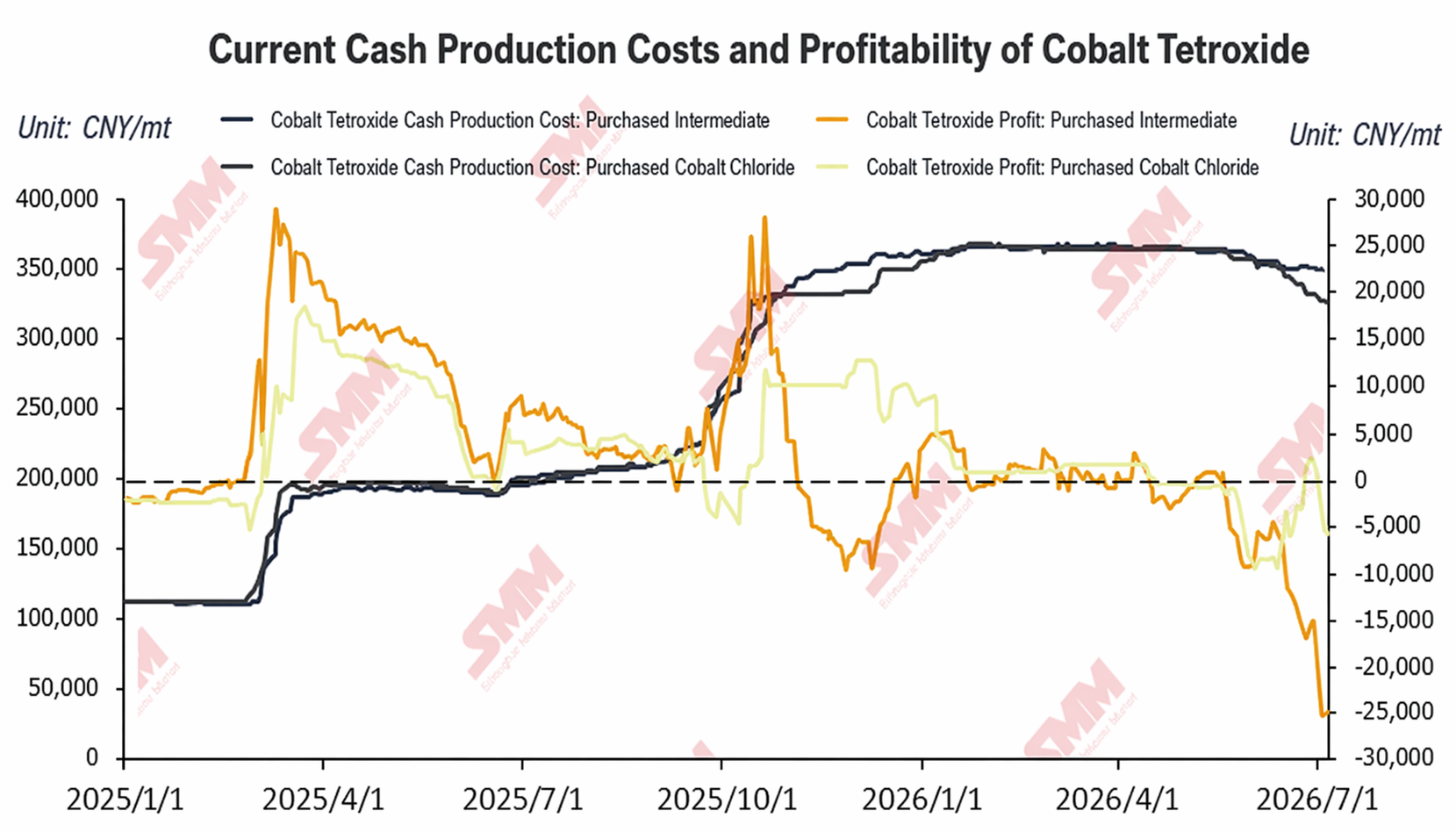

III. China Cobalt Product Smelting Margins: Growing Divergence, All Routes Slipping into Loss-Making Territory

In H1 2026, margins across cobalt products diverged significantly after a brief spike in January 2026, with most routes subsequently falling into deep losses:

Cobalt Sulphate: From late January to March, after downstream restocking ended, purchase willingness weakened and the market entered a stalemate with limited transactions. Cobalt sulphate and intermediate product prices were relatively stable, with margins only affected by exchange rate fluctuations and sentiment, consolidating within a narrow loss range. From April to June, financial pressure intensified on some smelters and traders, who sold at concessions, pushing cobalt sulphate into a grinding downtrend and further compressing production margins. By month-end June, losses for the externally purchased intermediate product route for cobalt sulphate widened to approximately 8,000 yuan/mt. Smelters, aside from executing long-term contracts, showed extremely low willingness to produce for spot orders, with some enterprises maintaining production cuts or suspensions.

Refined Cobalt: From mid-January, due to factors such as profit-taking and a weakening macro environment, refined cobalt prices retreated after a rapid rise, with profit margins continuously shrinking. In February–March, despite a brief rebound, prices resumed their decline under pressure from arbitrage and demand falling short of expectations. From April, some enterprises went long on China’s refined cobalt futures, which were perceived as undervalued, leading to some recovery in spot prices, but the smelting sector remained in deep losses. In May–June, cash production costs for both the externally purchased intermediate product route and the externally purchased cobalt sulphate route stabilized in the range of 450,000–500,000 yuan/mt, while spot prices lacked upward momentum due to weak end-user demand and continued position liquidation by traders, with maximum losses approaching 100,000 yuan/mt and significant industry operating pressure.

Cobalt Chloride and Co3O4: Before May, downstream acceptance of high prices was low, the market was relatively calm, prices held steady, and profits were only slightly affected by exchange rate fluctuations. In May–June, intermediate product raw material prices remained firm, but some cobalt chloride and Co3O4 enterprises, under pressure from cash flow and performance, sold at lower prices, causing profits to fall sharply. Among these, downstream demand for Co3O4 was weaker, and the price cuts were larger than those for upstream cobalt chloride, resulting in a significant narrowing of profits for the route that purchases cobalt chloride externally.

IV. China’s Cobalt Resource Supply-Demand Balance: Destocking Continues but Pace Slows

In H1 2026, China’s cobalt resource market remained in a destocking channel, but the destocking speed gradually slowed.

Intermediate Product Imports: The DRC announced a quota export policy in mid-October 2025, but due to delays in the approval process, actual imports of intermediate products into China in H1 2026 are expected to be only about 5,000 mt in metal content (with about 2,000 mt in June).

MHP Imports: In February this year, a Middle East geopolitical conflict triggered a sulphur supply crisis, delaying the commissioning of new Indonesian MHP hydrometallurgical projects and reducing output from existing projects. China’s MHP imports for full-year 2026 are expected to be only about 15,000 mt in metal content.

Domestic Production: Against the backdrop of raw material shortages, enterprises had a strong willingness to utilize recycled materials; China’s domestic production (including domestic ore and recycling) in H1 was about 21,000 mt in metal content.

Smelting Demand: Affected by raw material shortages and losses for most products, a large number of smelters cut production or suspended operations, with cobalt smelting demand in H1 at about 65,000 mt in metal content.

Overall, the H1 supply-demand gap was about 23,000 mt in metal content. The destocking trend remained intact, but the marginal intensity had weakened significantly compared to H2 2025.

V. H2 Outlook: Supply recovery expectations are strong, but uncertainties remain

Supply side, multiple sources of incremental growth are expected in H2: high production schedules at battery cell enterprises will generate large volumes of production waste, leaving room for further increases in recycled output; while the Strait of Hormuz crisis has not been fully resolved, sulfur transportation has slowly recovered and MHP output from Indonesia hydrometallurgy plants is expected to rebound, which will drive a corresponding increase in China’s imports; moreover, quotas accumulated in Q4 2025 and H1 2026 will gradually arrive at ports, and intermediate product imports will also slowly recover.

Demand side, as raw material supply improves, cobalt salt smelters will gradually resume production, and even some idled refined cobalt smelters that have been out of operation for an extended period could be restarted. However, against a backdrop of generally weak end-use demand, the incremental demand is expected to struggle to absorb the new supply, and the market may return to an inventory buildup pattern.

Two major uncertainties require close attention:

Sustainability of recycled output growth:The high recycled output in H1 was largely driven by strong economics, with many smelters increasing imports of overseas black mass and drawing down domestic scrap inventories. Recently, however, cobalt salt prices across grades have fallen faster than raw material prices, eroding recycling and smelting margins. If black mass imports pull back, recycled supply could fall short of expectations.

Miners holding prices firm and controlling circulation volumes:Miners currently remain strongly inclined to keep prices firm. If they restrict circulation volumes to maintain prices, actual intermediate product port arrivals into China could come in below current market expectations, thereby slowing the pace of inventory buildup or even tightening the supply-demand balance again.

Overall, the tug-of-war between sellers and buyers in the cobalt market will become more complex in H2 2026. The direction of supply recovery is largely certain, but the extent and pace will be heavily disrupted by policies, geopolitics, and corporate behaviors, while any demand recovery will hinge on a tangible recovery in end-use orders.

Xiao Wenhao 16621140365

![[SMM Analysis] In June, the high comprehensive cost of anode materials supported the upward shift of the price center.](https://imgqn.smm.cn/usercenter/jZvMC20251217171729.jpg)

![[SMM Mid-Year Market Analysis] 2026 H1 LFP Cathode Material Market Review](https://imgqn.smm.cn/usercenter/mzgdV20251217171729.png)

![[SMM Analysis] Raw Material Side Under Pressure and Pulled Back, Graphitisation Costs Rose Sharply, June Anode Material Costs Stayed High](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)