H1 Market Review, January-June

In H1 2026, the manganese industry chain exhibited a pattern of “strong first, then weak, consolidating at highs,” with the market centering on a tug-of-war between high cost support and sluggish end-use demand.

Drifting Higher, Driven by Cost and Demand, January-February

In January-February, manganese product prices extended the year-end uptrend, steadily strengthening and drifting higher overall.

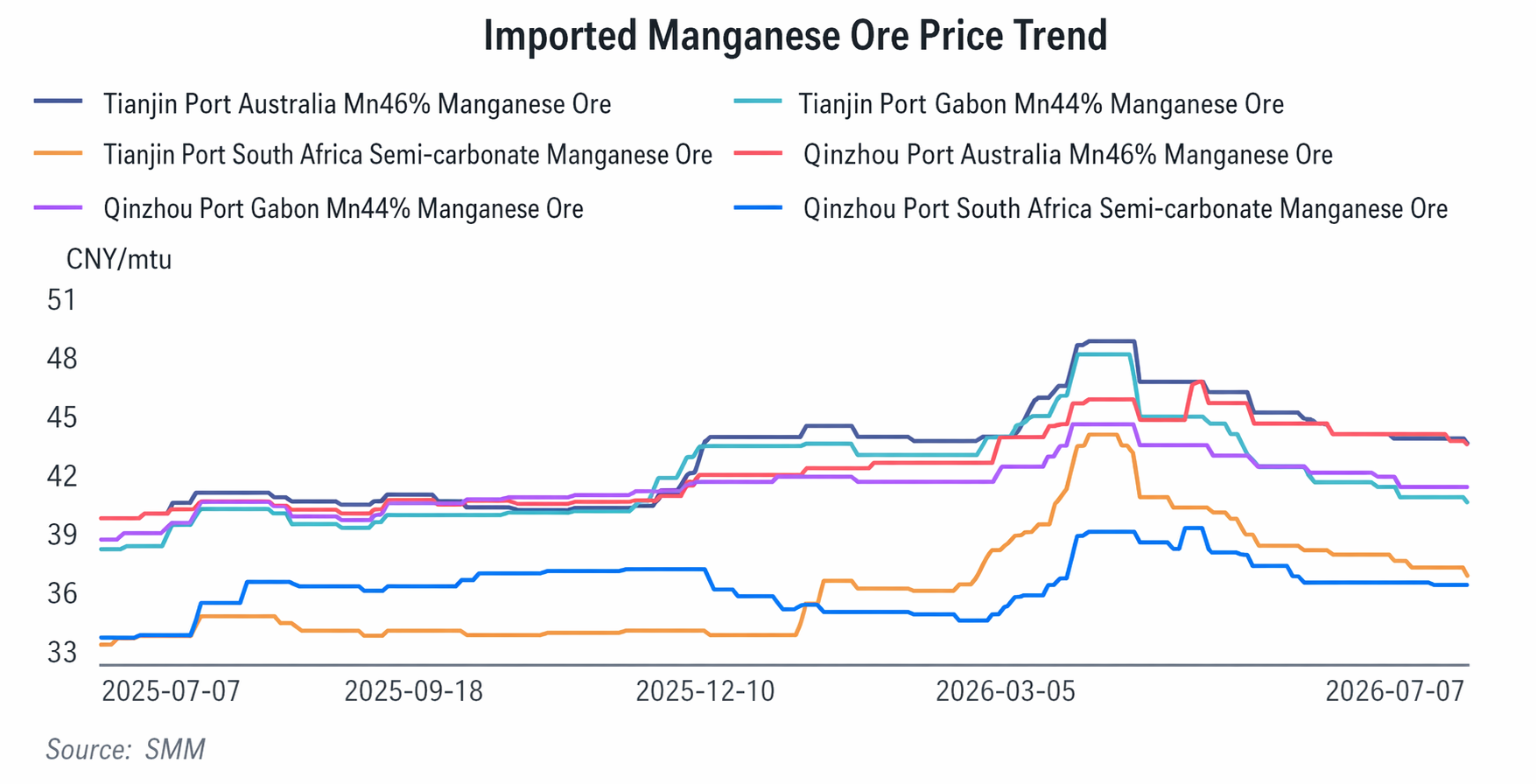

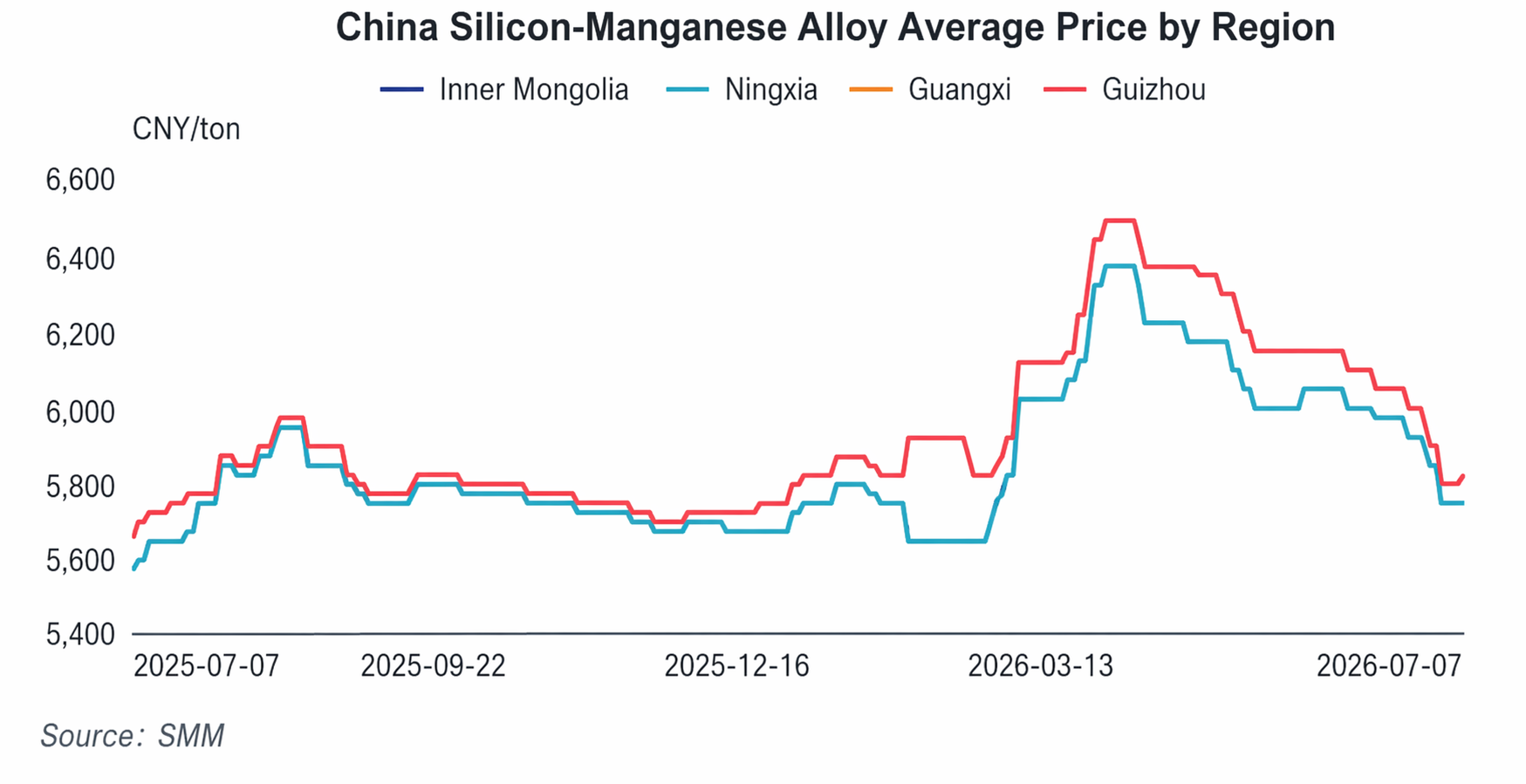

Specifically, the price of high-grade Australian lump manganese ore at Tianjin port gradually climbed from around 40 yuan/mtu to 43-44 yuan/mtu; the EXW price of SiMn 6517 rose from around 5,575 yuan/mt to 5,700 yuan/mt. This round of price increases was driven by a dual resonance of cost and demand.

Cost side, overseas manganese ore markets continued to hold prices firm, pushing up the landed cost of domestic manganese ore steadily. Traders, to hedge against the risk of high-priced future shipments, showed a strong willingness to keep prices firm. Meanwhile, ahead of the Chinese New Year, port manganese ore inventories were at a year-round low, further cementing the basis for ore price gains.

Supply side, northern blast furnace enterprises underwent concentrated maintenance during the Chinese New Year, while southern enterprises made limited production cuts, resulting in a temporary contraction in overall alloy supply.

Demand side, at the start of the year, downstream steel mills began concentrated raw material restocking for the Chinese New Year, releasing significant procurement demand that effectively absorbed market supply, driving manganese ore and manganese alloy prices to continuously drift higher.

Rapid Surge, Ore Prices and Alloys Hit Year Highs Simultaneously, March-April

In March-April, the manganese market trended upward unilaterally, with raw material and alloy prices surging in tandem, posting gains of over 10% and hitting H1 price peaks.

The core logic behind this round of price increases was the superimposition of three bullish factors: supply disruption expectations, market sentiment premiums, and rigid production cost increases. Specifically, Australian lump manganese ore (46% grade) at Tianjin port peaked at around 48 yuan/mtu, up 9.97% from early March; semi-carbonate ore peaked at 43.75 yuan/mtu, up 16.8%; and SiMn 6517 reached a peak of around 6,300 yuan/mt, up 10.5%.

Cost side: ① Manganese ore: Typhoon disturbance in Australia disrupted shipments, South Africa’s power supply tightened, and ocean freight rates rose amid the US-Iran war, driving ore prices up rapidly on funds and sentiment; ② Coke: The first round of price increases was implemented in March, further lifting costs and passively pushing up alloy smelting costs; ③ Electricity prices: The cancellation of peak-flat-off-peak pricing in south China limited production resumptions there, strengthening cost support.

Supply side, in the northern industry, high-capacity enterprises took the lead in initiating industry self-discipline and voluntarily cutting production, tightening supply and supporting price increases. Demand side, although steel mills had expectations of “production caps,” short-term rigid demand persisted. Tender prices were passively raised along with ore prices, and alloy transactions remained moderate.

May-June: Retreat after rapid rise, intensifying tug-of-war between cost and demand, prices drifted lower.

From May onward, the manganese market showed a turning point, entering a phase of retreat after rapid rise and being in the doldrums. The supply strong, demand weak pattern intensified, with the cost-demand game becoming the dominant force in the market.

The cost side still provided rigid support. Frequent domestic coal mine accidents in May led to multiple rounds of price raises for chemical coke, with a cumulative increase exceeding 250 yuan/mt. Additionally, the arrival of summer heat drove regional electricity loads higher, with industrial electricity prices edging up, leaving the high-cost structure of alloy smelting unchanged. However, demand-side headwinds were concentrated, with steel mills slowing their procurement pace and persistently pushing for lower prices, leading to successive downward revisions of tenders.

End-use demand weakness continued to squeeze alloy producer profits, forcing them to actively push down manganese ore purchase prices, which in turn pulled back ore and alloy prices simultaneously. The supply strong, demand weak pattern remained unimproved, with some enterprises starting to cut production.

H2 (July-December) Market Forecast

In H2, the manganese market is expected to see “cost-supported, weak demand recovery, prices drifting higher with limited upside”: overseas manganese ore prices are more likely to rise than fall, but high port inventories will limit gains; the SiMn alloy price center is expected to move higher, supported by production cuts, destocking, and cost factors, though the rebound height is constrained by downstream demand recovery strength and the extent of supply reduction.

July-August will be dominated by consolidating at lows. The current headwinds of high alloy inventories and weak demand are gradually being absorbed, coupled with clear bottom support from coke and electricity prices, as the industry continues active production cuts, with supply-side contraction easing supply-demand pressure. Declines in manganese ore, SiMn, and FeMn prices will narrow, entering a consolidate at lows phase with no further deep correction space, laying a solid foundation for a subsequent rebound.

September-October’s traditional peak season is expected to drive the price center higher. Concentrated restocking by steel mills will drive a recovery in end-use demand, while port manganese ore and mill alloy inventories are gradually destocked. Combined with firm overseas ore prices, cost and demand will form a dual tailwind, with manganese industry chain prices poised for a phased rebound, representing the core profit window for H2.

November-December will shift to consolidating at highs. Winter stockpiling demand provides support, but year-end crude steel output-control policies may cap demand upside as the market rebounds.

![ADC12 prices generally stable with slight rise, domestic-overseas inversion continues to repair [ADC12 Price Daily Review]](https://imgqn.smm.cn/usercenter/znXdm20251217171724.jpeg)

![[SMM Analysis] South Africa's Chrome Ore and High-Carbon Ferrochrome Exports](https://imgqn.smm.cn/usercenter/FHiZE20251217171722.jpeg)