Highlights: On July 6, 2026, Samsung SDI disclosed regulatory documents on July 3, announcing an investment of approximately 16 trillion Korean won (approximately 88 billion yuan) in its Ulsan plant by 2040 to build a large-scale production site for all-solid-state batteries, LFP batteries for ESS, and sodium-ion batteries. A day earlier (July 2), the company had announced a 9 trillion won investment in its Cheonan plant to construct a next-generation battery technology verification mother production line and R&D facilities. The two investments total 25 trillion won, with an investment period of up to 14 years, extending to 2040.

,

[Seoul/Ulsan/Cheonan, July 6, 2026] On July 3, Samsung SDI disclosed regulatory documents, announcing an investment of approximately 16 trillion Korean won (approximately 88 billion yuan) in its Ulsan plant by 2040 to build a large-scale production site for all-solid-state batteries, LFP batteries for ESS, and sodium-ion batteries. A day earlier (July 2), the company had announced a 9 trillion won investment in its Cheonan plant to construct a next-generation battery technology verification mother production line and R&D facilities. The two investments total 25 trillion won, with an investment period of up to 14 years, extending to 2040.

The investment blueprint was officially unveiled on July 3 at the "National Report on the Vision for Advanced Industry Development in the Yeongnam Region" hosted by President Lee Jae-myung in Jinju, South Gyeongsang Province. Samsung Electronics President Roh Tae-moon, representing Samsung Group, announced that the group will invest 60 trillion won in the Yeongnam region to create a manufacturing ecosystem centered on physical AI and robotics, with Samsung SDI's 16 trillion won Ulsan investment as a core component.

1. Investment Details and Strategic Layout

1. Ulsan Site: Core Mass-Production Hub for Next-Generation Batteries

The Ulsan plant will undertake the mass production of Samsung SDI's next-generation batteries, focusing on three major product lines:

Chart-1: Samsung SDI's Three Major Product Lines

Samsung SDI emphasized that this investment will secure the company's position as a global manufacturing base for next-generation batteries. The company plans to achieve mass production of all-solid-state batteries in H2 2027. It has already built a 6,500 m² "S-Line" pilot production line at the Suwon SDI Research Center and is providing samples to five major global OEM clients for performance verification.

2. Cheonan Site: Next-Generation Battery R&D and Verification Center

The Cheonan plant will be positioned as Samsung SDI's global Mother Factory, with core functions including:

Mother Line: Used to validate next-generation battery technology, ensuring process reliability before mass production.

DryEV Pilot Line: Overcomes the cost bottleneck of traditional wet electrode manufacturing processes, enhancing production efficiency.

Supporting R&D Facilities: Support the continuous development of cutting-edge technologies such as all-solid-state batteries and 46-series large cylindrical batteries.

The Cheonan plant had previously undertaken the construction of the test production line for Samsung SDI's 4680 large cylindrical batteries, with a planned annual capacity of 1 GWh, and after successful testing will be mass-produced at the Malaysia plant (planned capacity of 8–12 GWh).

3. Dual-Track Strategy: R&D and Mass Production Separation

Chart-2: Samsung SDI Base

This layout embodies Samsung SDI's step-by-step advancement strategy of "R&D first, mass production later": Cheonan is responsible for technology maturity and process validation, while Ulsan handles mass production and cost optimization.

II. In-depth Analysis: Why Bet Now?

1. Investment Backdrop: From "EV Calm" to "AI Energy Revolution"

Samsung SDI's timing for this large-scale investment is highly strategic.

1.1 Near-term Pressures

From 2024 to 2025, the global EV market encountered a "cold spell" (EV Cacm), and Samsung SDI's performance came under pressure. In 2024, operating profit was only 363.3 billion won, a 76.5% YoY plunge; in 2025, the company even posted its first quarterly loss in seven years (Q4 operating loss of 256.7 billion won).

1.2 Long-term Opportunity

The surge in electricity demand from AI data centers is driving rapid growth in the ESS market. SNE Research forecasts that the global ESS market will grow from 235 GWh in 2025 to 618 GWh in 2035, a 163% increase. Samsung SDI's Q1 2026 results showed that demand for power-related batteries such as ESS, UPS, and BBU jumped 13% YoY, becoming the core driver of performance improvement.

1.3 Strategic Assessment

The company views 2026 as the "turnaround first year," achieving short-term performance recovery through the ESS business and medium- and long-term technological leadership through all-solid-state batteries.

2. Technology Route: The "All-In" Bet on Sulphide-Based All-Solid-State Batteries

Samsung SDI has chosen the sulphide-based (황화물계) solid electrolyte route, which is currently the most technically challenging but offers the highest performance potential:

2.1 Technical Advantages

Ionic conductivity closest to liquid electrolytes, supporting high-power output.

Energy density up to 900 Wh/L (over 40% higher than existing products)

9 minutes to complete fast charging from 8% to 80%

Supporting a driving range of 1,000 km

2.2 Technical Challenges

Sulphides readily react with moisture in the air to form hydrogen sulphide gas, requiring a strictly dry environment

High solid-solid interface impedance necessitates ultra-high pressure pressing processes

Manufacturing cost is estimated to be over 400 times higher than that of conventional lithium batteries

Samsung SDI has overcome some bottlenecks through anode-less technology and roll press process conversion, and in 2025 converted the pressing process from the traditional WIP (isostatic pressing) to roll pressing, which is more suitable for mass production.

3. Application Scenarios: Stride from EVs to Physical AI

Samsung SDI is expanding the application of all-solid-state batteries from conventional EVs to the field of Physical AI:

Humanoid robots: In March 2026, it first unveiled pouch-type all-solid-state battery samples, targeting mass production in H2 2027

Mobile robots/industrial robots: High energy density supports long-term autonomous operation

Urban Air Mobility (UAM): High safety satisfies aviation-grade requirements

High-Altitude Platform Stations (HAPS): Stable power supply under extreme environments

This strategic shift reflects the Samsung Group's full commitment to the "AI+Robotics" ecosystem. The Group plans to invest 60 trillion KRW in the Yeongnam region, of which Samsung Electronics and SDS will invest 19 trillion KRW to build robotics and AI data centres, and Samsung SDI's 16 trillion KRW battery investment serves as the hardware foundation.

III. South Korea Solid-State Battery Industry Competitive Landscape Comparison

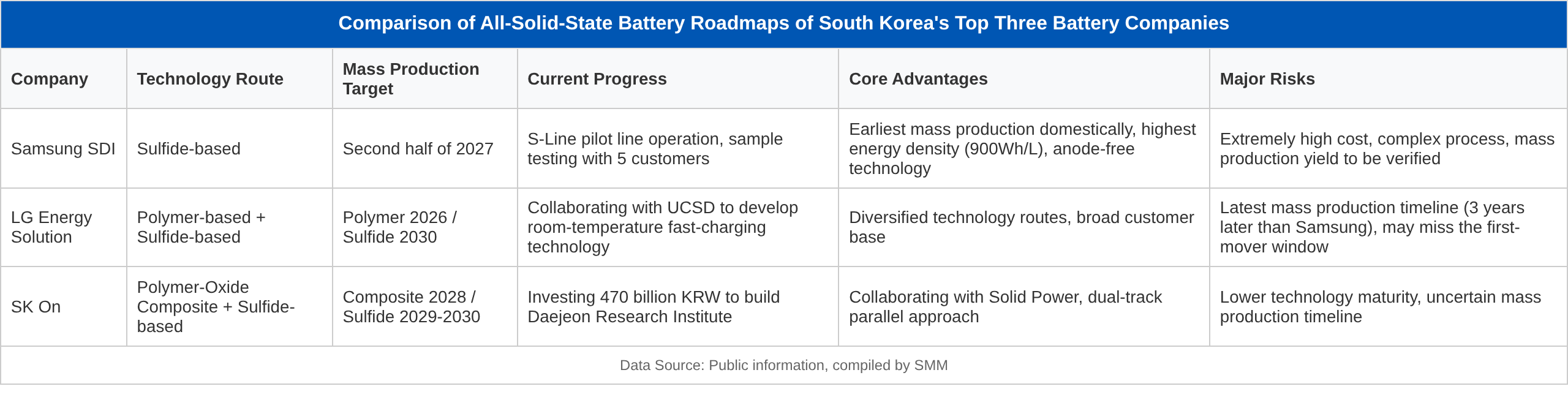

Chart-3: Comparison of All-Solid-State Battery Roadmaps among Three Major South Korean Battery Companies

Chart-4: Global Competitive Landscape

IV. Analysis of Key Competitive Factors

1. Mass Production Time Window

Samsung SDI's H2 2027 target holds a clear global lead

If successfully realised, it will gain a 3–5 year technology monopoly period, potentially defining industry standards

However, the risk is that the penetration rate of all-solid-state batteries is expected to be only 4% by 2030 and exceed 2% only by 2032

2. Cost Reduction Curve

Currently, the raw material cost of sulphide solid electrolytes is 50–60 times that of liquid electrolytes

Samsung SDI expects that mass production can reduce this to 10–20 times

Even so, initial products can only be equipped in high-end EVs and robots, and mass market penetration will require a longer time

3. Customer Validation Progress

Samsung SDI has provided samples to BMW, Hyundai Motor, and others, and plans to conduct vehicle mounting tests at the end of 2026

LG Energy Solution maintains technical ties with the Volkswagen Group (collaborating through QuantumScape)

SK On is partnering with Solid Power, but its client validation progress is relatively slow

4. Supply Chain Independence

Samsung SDI is committed to producing core materials in-house to reduce external reliance

In March 2025, it raised approximately 2 trillion won through a rights offering, specifically for the construction of all-solid-state battery production lines

V. Market Outlook

1. Financial Impact on Samsung SDI

Short-term pressure: Large-scale CAPEX will exacerbate the financial burden from 2026 to 2027. The company has suspended cash dividends for two consecutive years (2025-2027) to concentrate resources on future investments

Mid-term turning point: The securities industry expects to turn a quarterly profit in H2 2026. Performance is anticipated to significantly improve in 2027 with the launch of US Stellantis/GM joint venture plants and the mass production of all-solid-state batteries

Long-term value: If mass production of all-solid-state batteries is successful in 2027, the company could transition from a "traditional battery manufacturer" to a "next-generation energy solution provider," leading to a restructuring of its valuation system

2. Impact on the South Korean Battery Industry

Regional balance: Investments in Ulsan (Yeongnam) and Cheonan (Chungcheong) will drive the development of battery industry clusters in southeastern and central South Korea, reducing dependence on the capital region

Technological sovereignty: Establishing a complete all-solid-state battery industry chain in South Korea reduces reliance on Chinese raw materials and equipment

Job creation: Samsung Group expects to create 200,000 high-quality jobs in the Yeongnam region alone

3. Impact on the Global Battery Landscape

Standard-setting power: If Samsung SDI is the first to commercialize all-solid-state batteries, South Korea is poised to gain a dominant role in setting global battery technology standards

China challenge: The Chinese government has invested over 1 trillion won to support all-solid-state battery R&D. Companies like CATL and BYD are accelerating their catch-up efforts, though their technical approach is becoming more pragmatic (semi-solid transition)

Japan counterattack: Although Toyota and Panasonic have deep technological expertise, their conservative approach to commercialization could cause them to miss critical market opportunities

VI. Risks and Challenges

Technical risks: Core technical bottlenecks for all-solid-state batteries, such as solid-solid interface issues and cycle life (currently around 1,000 cycles, while EVs require over 2,000 cycles), have yet to be fully resolved

Cost risks: Extremely high initial manufacturing costs may limit these products to the high-end market, with economies of scale forming slowly

Competition risks: Chinese companies have already achieved mass production in the semi-solid-state battery sector (e.g., NIO models equipped with semi-solid-state batteries) and may capture market share through "incremental innovation"

Policy Risk: Changes in US IRA policy, EU battery regulations, and other trade policies may affect the global supply chain layout.

Performance Risk: In 2026, the company is expected to still have about 967 billion won in operating losses, and if ESS business growth falls short of expectations or all-solid-state battery mass production is delayed, financial pressure will further intensify.

Conclusion

Samsung SDI's 25 trillion won investment plan is the largest forward-looking layout in the history of South Korea's battery industry, reflecting the company's determination to transform from a "follower" to a "leader." Against the backdrop of a short-term downturn in the EV market and immature all-solid-state battery technology, this "contrarian gamble" is fraught with risks but also holds immense opportunities.

7. Key Periods

End of 2026: BMW all-solid-state battery vehicle integration test results.

H2 2027: Whether the Ulsan all-solid-state battery mass production line will start production as scheduled.

2028: Actual installations of all-solid-state batteries in the robotics and EV fields.

2030: Whether the all-solid-state battery market penetration rate reaches the industry's expected 4%, with SMM expecting less than 1%.

If Samsung SDI is able to achieve the 2027 mass production target as planned, it will not only reshape the global competitiveness of the South Korean battery industry but also potentially redefine the energy standards for the entire NEV and robotics industries. Conversely, if technological bottlenecks cannot be overcome or cost reductions fall short of expectations, this investment could become a heavy burden that drags down the company's long-term development.

Tel: 021-20707860 (or add WeChat: 13585549799) Yang Chaoxing, thank you!

Related Information

![Highly Likely Fake News: Rumor of Major Manufacturer’s 15 GWh Sulphide All-Solid-State Battery Production Launch [SMM Analysis]](https://imgqn.smm.cn/usercenter/gcOsy20251217171726.jpg)

![[SMM Analysis] Indonesia's May Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/BdFZr20251217171712.jpg)