Entering July, the tungsten industry chain prices remained in the doldrums. A large tungsten enterprise lowered its long-term contract purchase quotes for the first half of July, while the Ganzhou Tungsten Association simultaneously lowered its monthly forecast average prices for all tungsten product categories, with prices across all categories down MoM. The spot market also followed suit and was under pressure. According to SMM quotes, wolframite concentrates (≥65%) have been on a weak decline since mid-to-late June. Looking back at the market trend this year, tungsten prices experienced wild swings. Comparing the two downward cycles, the overall decline in this round of adjustment that started in mid-June has narrowed compared with the first correction from March to May. Currently, the traditional off-season effect is prominent. Factors such as weak downstream demand and raw material inventory awaiting digestion continue to weigh on tungsten price performance; however, the scarcity of low-priced high-grade ore supplies will provide some support for tungsten prices.

Industry Long-term Contract Quotes and Association Monthly Forecast Prices All Lowered

A tungsten enterprise lowered its long-term contract quotes for the first half of July, as follows:

According to Chongyi Zhangyuan Tungsten Co., Ltd. on July 6, its long-term contract purchase quotes for the first half of July are: 1. 55% wolframite concentrates: 448,000 yuan/standard tonne (65%WO3 basis), down 72,000 yuan/standard tonne from the previous round of quotes; 2. 55% scheelite concentrates: 447,000 yuan/standard tonne, down 72,000 yuan/standard tonne from the previous round of quotes; 3. APT (GB Grade 0): 660,000 yuan/mt, down 120,000 yuan/mt from the previous round of quotes.

The Ganzhou Tungsten Association released its forecast average prices of tungsten products for July 2026, with 55% wolframite concentrates at 448,000 yuan/standard tonne, down 57,000 yuan/mt from June; APT at 660,000 yuan/mt, down 100,000 yuan/mt from June; and medium-grain tungsten powder at 1,100 yuan/kg, down 200 yuan/kg from June.

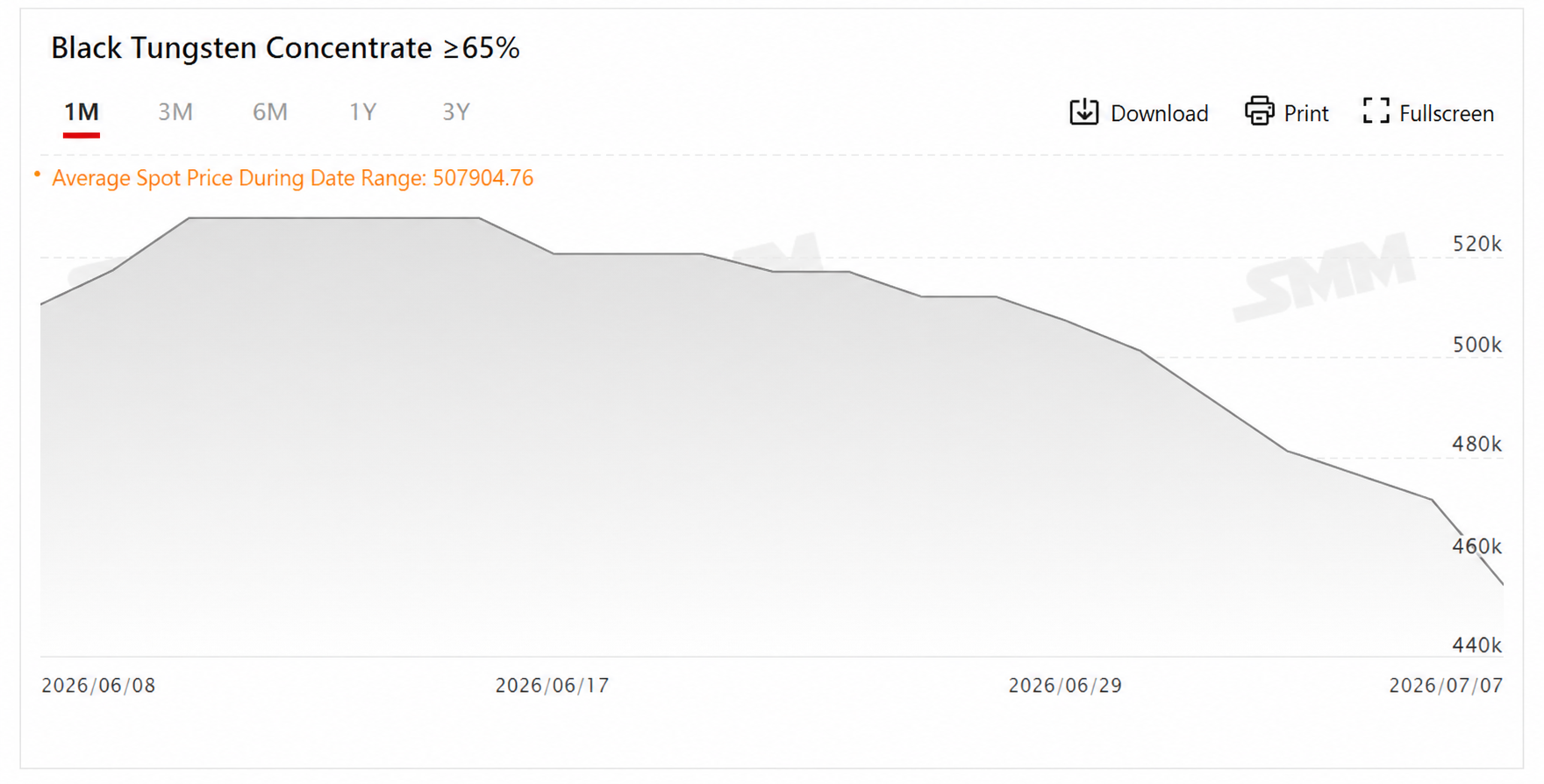

Wolframite Concentrates Fall 13.93% in Less Than a Month

According to SMM quotes, the price of wolframite concentrates (≥65%) on July 7 was 453,000-455,000 yuan/standard tonne, with an average price of 454,000 yuan/standard tonne, down 3.61% from the previous trading day.

Looking back at the short-term trend, after the average price of wolframite concentrates rebounded to a previous high of 527,500 yuan/standard tonne in early-to-mid June, weak downstream demand, together with the fact that raw material inventory accumulated from earlier concentrated enterprise stockpiling was still in the digestion cycle, weakened market support, and tungsten prices began a general weak downward adjustment from June 17. Compared with the average price of 527,500 yuan/standard tonne on June 16, the average price of 454,000 yuan/standard tonne on July 7 represents a decline of 73,500 yuan/standard tonne in less than a month, a drop of 13.93%.

Taking a longer-term perspective, entering July, the average price trend of wolframite concentrates (≥65%) so far this year has been a dramatic roller coaster. Supported by tight raw material supply at the start of the year, wolframite concentrates (≥65%) began at 453,500 yuan/standard tonne on January 5, before surging to a historic high of 1,050,500 yuan/standard tonne on March 13. At such high prices, market caution and fear of high prices gradually intensified, and coupled with limited acceptance from end-use demand, tungsten prices embarked on an overall downward trajectory, ultimately falling to an intra-year low of 400,500 yuan/standard tonne on May 25. After a deep correction in the preceding period, the market had a demand for an oversold recovery. This, combined with the concentrated release of phased restocking demand, saw tungsten prices start a rebound recovery from May 27, rising to 527,500 yuan/standard tonne on June 10.

A comparison of two complete downward cycles so far this year reveals that the first round of correction after the initial-year surge featured a wider range of fluctuation, while the current correction, which began in mid-June, has seen a narrower overall downward magnitude relative to the previous correction. Synthesizing key price periods, it is clear that the wolframite concentrates market has experienced a large magnitude of fluctuations and prominent volatile characteristics this year.

Outlook

Looking ahead, in the short term, July marks the entry into the traditional off-season for downstream consumption. Purchasing willingness from cemented carbide and mechanical processing enterprises is weak, and market demand is performing mediocrely. However, circulating supply of high-grade tungsten ore is relatively scarce. With bullish and bearish factors checking each other, tungsten prices are expected to maintain narrow sideways consolidation. The pace of improvement on the downstream demand side remains a key focus going forward.

In the medium and long term, domestic regulation on primary tungsten mining is continuously tightening, rigid demand support exists from the cemented carbide sector, and the scale of net tungsten product exports is growing steadily, leaving a supply-demand gap for the element tungsten throughout the year. In Q3, the insufficient alignment of mining indicators will create expectations of tightening on the raw material supply side, while the traditional "September-October peak season" is expected to drive a recovery in enterprise restocking demand. Simultaneously, rigid demand in military, high-end equipment, and new energy sectors continues to expand, and the price spread between Chinese and overseas markets is also expected to continuously boost export orders. Multiple favorable factors provide strong support for the medium and long-term central price range of tungsten. However, vigilance is needed regarding the risk of rapid market rises squeezing downstream processing enterprises' profits, which could force end-user production cuts and create negative feedback. Overall, the tungsten market is expected to follow a mild and orderly upward trajectory thereafter.

Recommended Reading: