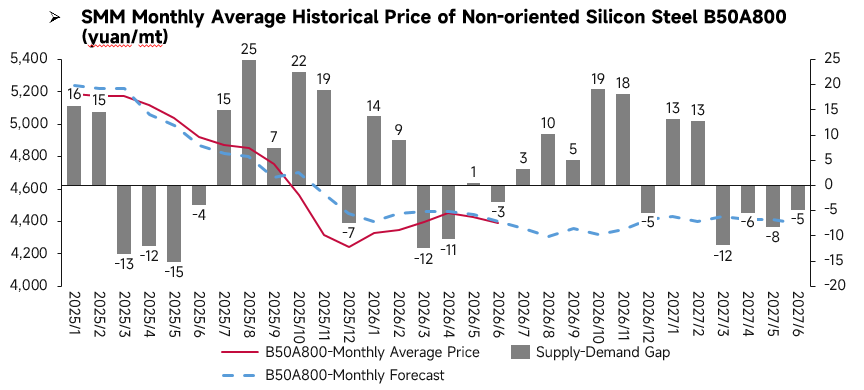

June Price Review:

The monthly average price of non-oriented silicon steel exhibited a bottoming-out decline in June. On the supply-demand front, the market shifted from a slight balance to a narrow undersupply, with fundamentals continuing to improve marginally. The oversupply that previously weighed on the market gradually eased, providing price support. Spot prices performed stronger than expected, edging down only slightly. As a transitional month shifting from off-season to peak season, the supply-demand pattern improved in June.

Fundamental Analysis:

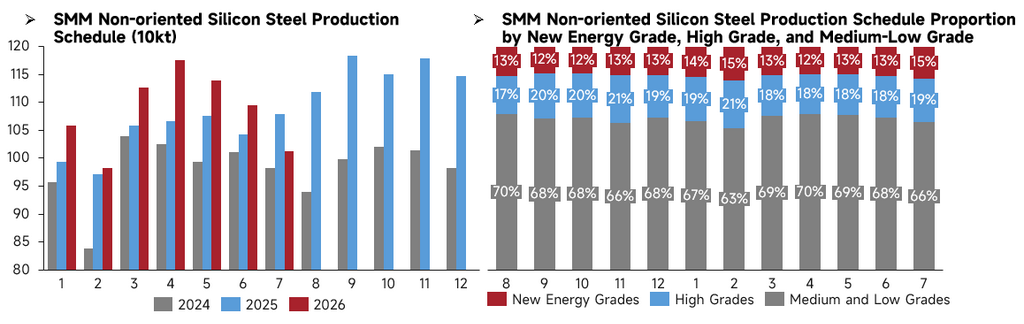

China's production schedule for non-oriented silicon steel continued to decline in July. Comparing with the same period in previous years, the scheduled production in July 2026 was lower than that of July 2025. Analyzing by grade, the proportion of NEV grades in the July production schedule rebounded to 15%, high grades accounted for 19%, while the proportion of low and mid-end grades pulled back to 66%. Steel mills continued to adjust their product mix, with the scheduled production of conventional low and mid-end grades shrinking accordingly. While total scheduled production continued to contract, supply-side pressure persisted. Maintaining original production levels for NEV and high-grade resources while significantly reducing low and mid-end grades optimized the supply structure to some extent, supporting market resilience.

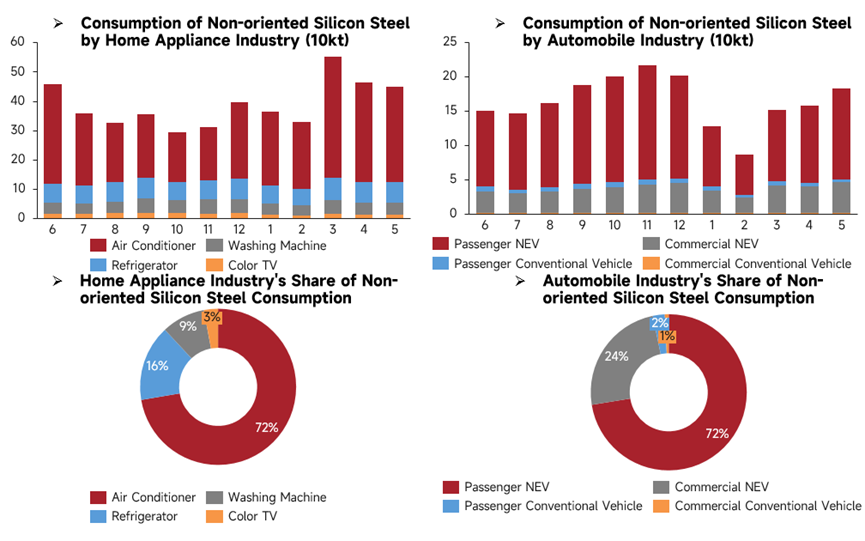

Downstream demand for non-oriented silicon steel showed structural divergence in May. In the home appliance sector, total silicon steel consumption pulled back MoM, with air conditioners remaining the core demand driver. Demand from the automotive sector was strong, with silicon steel consumption climbing to a high level for the period in May. Specifically, passenger NEVs provided the largest support for automotive silicon steel demand. Overall, traditional demand from home appliances weakened marginally, while NEV demand continued to strengthen. The demand center shifted toward the automotive sector, generating structural benefits for high-grade and NEV-grade non-oriented silicon steel.

July Price Outlook:

Supply side, China's planned production schedule for non-oriented silicon steel continued to decrease in July 2026, with reductions primarily focused on low and mid-end grades. On one hand, the off-season impact became more pronounced, downstream demand was soft, and purchasing interest declined, curbing production activity. On the other hand, industry leaders like Baowu and Shougang kept base prices unchanged in July, prioritizing price stability, but bearish sentiment persisted, making prices more likely to fall than rise. Most producers were loss-making and cut production autonomously. Demand side, in the home appliance sector, enterprises slowed their production pace, with orders falling MoM. The 618 shopping festival provided no significant order stimulus. Affected by low demand, high inventory, and high costs, some enterprises cut their production schedules ahead of schedule, and the implementation of new energy efficiency standards for some appliance products led to model upgrades that restricted production. In the automotive sector, automakers generally maintained normal production paces, with some increasing production schedules this month to meet mid-year targets. However, the sales promotions of the 618 festival and policies yielded limited boosting effects, and sales pressure persisted. Breaking it down, NEVs remained the main sales driver this month, orders for internal combustion engine vehicles showed no significant improvement, and exports were mainly directed to markets such as Russia, South America, and Southeast Asia, with the industry's full-year export volume expected to reach 12 million units. Cost side, with steel mill profits continuing to shrink and expectations of normalized local environmental protection-driven production restrictions, hot metal production is expected to continue to pull back. But as the off-season impact expands, the average hot-rolled coil price in July is expected to decline further MoM from June, though the extent of the decline will narrow. In summary, SMM expects that prices for low and mid-end non-oriented silicon steel will drift lower overall in July 2026, with some room for price reductions.

![[Al Yamamah Steel Advances Steel Billet Project]](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)

![[China Iron Ore Brief] China iron ore concentrates prices may remain in the doldrums next week](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)

![[SMM Hot-Rolled Coil Daily Trading Volume] Spot trading volume continues to consolidate near the bottom](https://imgqn.smm.cn/usercenter/zLhJl20251217171720.jpg)