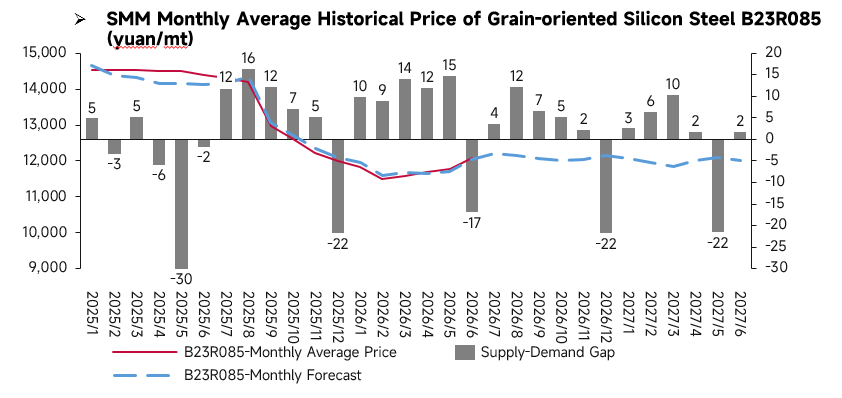

June Price Review:

In June, the monthly average price of GO silicon steel continued its previous rebound trend, with the price center continuing to rise. Despite relatively high supply pressure, the earlier trend of price bottom repair persisted, and the monthly average spot price steadily rose, reflecting that the market held good expectations for a market recovery. However, the oversupply pattern capped the upside room, and the price uptrend was relatively mild without any sharp surge.

Fundamental Analysis:

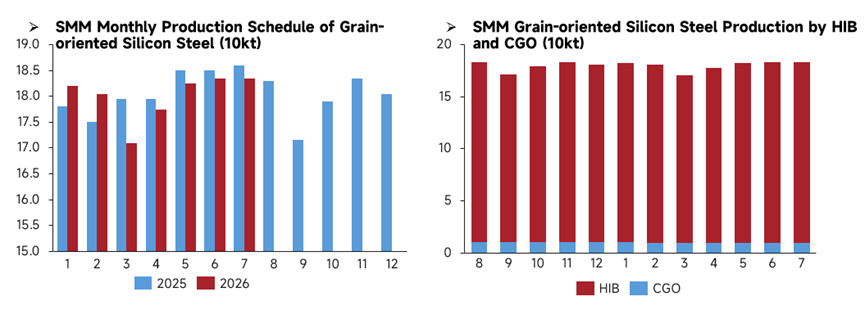

In July, GO silicon steel production is expected to stay high. In terms of production by variety, HIB and CGO output will remain stable, with high-grade HIB still accounting for the vast majority of production, while CGO output will hold steady within a narrow range, and the product mix will not undergo significant adjustments. Compared with historical production schedules, the July 2026 production schedule will continue the high-level range, with overall supply releases stable, and total GO silicon steel supply will remain relatively ample. Sustained high output has also become one of the core factors capping the upside room for GO silicon steel prices this round and keeping the supply-demand balance loose.

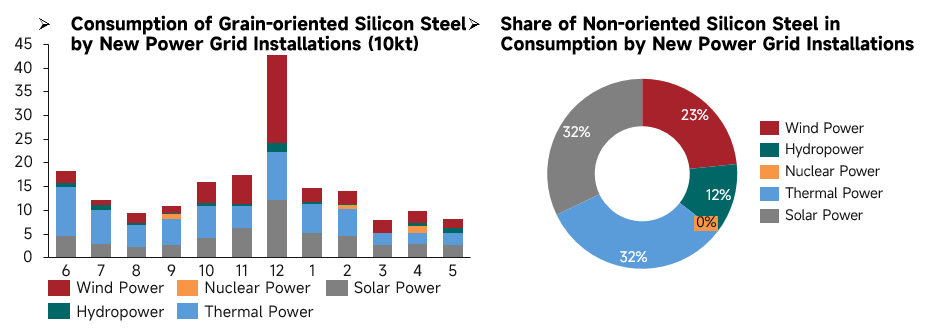

In May, GO silicon steel consumption driven by new grid installations was at a relatively low level for the year. In terms of structure, thermal power and solar power remained the main consumption sources, with wind and hydropower demand providing supplementation, and nuclear power’s share staying low. Compared with the consumption structure of non-oriented silicon steel, thermal power and solar together accounted for 60%, making the demand structure characteristics on the power supply side clear. In May, the pace of new terminal installations slowed down, transformer enterprise order growth was limited, and direct demand for GO silicon steel was released slowly, coupled with sustained high production at steel mills earlier, supply-side pressure was hard to digest, which weighed on silicon steel prices, making it difficult to rely on grid installations for strong demand boost in the short term.

July Price Outlook:

Looking ahead to July 2026, on the supply side, China's GO silicon steel supply is expected to be basically stable. Mainstream steel mills’ production lines will operate stably with no concentrated maintenance plans, and the overall production load will remain stable. Meanwhile, mainstream steel mills such as Baowu will raise the base price of grain-oriented products by 300 yuan/mt in their July pricing policies. Coupled with production profits maintaining a reasonable range, overall production enthusiasm will be good, and high-grade resources will be steadily released. Demand side, favorable market support continues, with overall demand performing robustly. China’s “15th Five-Year Plan” UHV projects continue to start construction in a concentrated manner, with the construction pace steadily advancing. Demand for transformers supporting new energy grid connections is robust. At the same time, energy efficiency upgrades for home appliances and NEVs are gradually being implemented, keeping demand for high-efficiency motor retrofits high. Moreover, overseas power grid upgrade projects are advancing, and procurement demand for high-grade GO silicon steel remains stable. However, India’s launch of anti-dumping against China’s GO silicon steel may cause some resources to flow back into the domestic market, weighing on price increases. Cost side, with expectations of further shrinking steel mill profits and normalizing production restrictions driven by local environmental protection, hot metal output is expected to continue to decline. However, the off-season impact on the market is expanding, and the average HRC price in July is expected to decline further MoM from June, with the decline narrowing. Overall, SMM expects that GO silicon steel prices will present a consolidation pattern in July 2026.

![[Al Yamamah Steel Advances Steel Billet Project]](https://imgqn.smm.cn/usercenter/UqlZJ20251217171717.jpg)