Around June 24, 2026, import and export data for products related to the cobalt and lithium battery industry chain for May were released. The data shows that spodumene imports in May continued to pull back from April, reaching 681,000 mt in physical content, down 10% MoM, equivalent to approximately 66,000 mt of lithium carbonate equivalent (LCE). On the lithium carbonate import side, China imported 37,555 mt of lithium carbonate in May, up 15% MoM and up 78% YoY. Cumulative imports of lithium carbonate from January to May reached 153,000 mt, up 53% YoY year-to-date... SMM has consolidated the import and export situation of battery materials, as follows:

Upstream

Lithium Concentrates

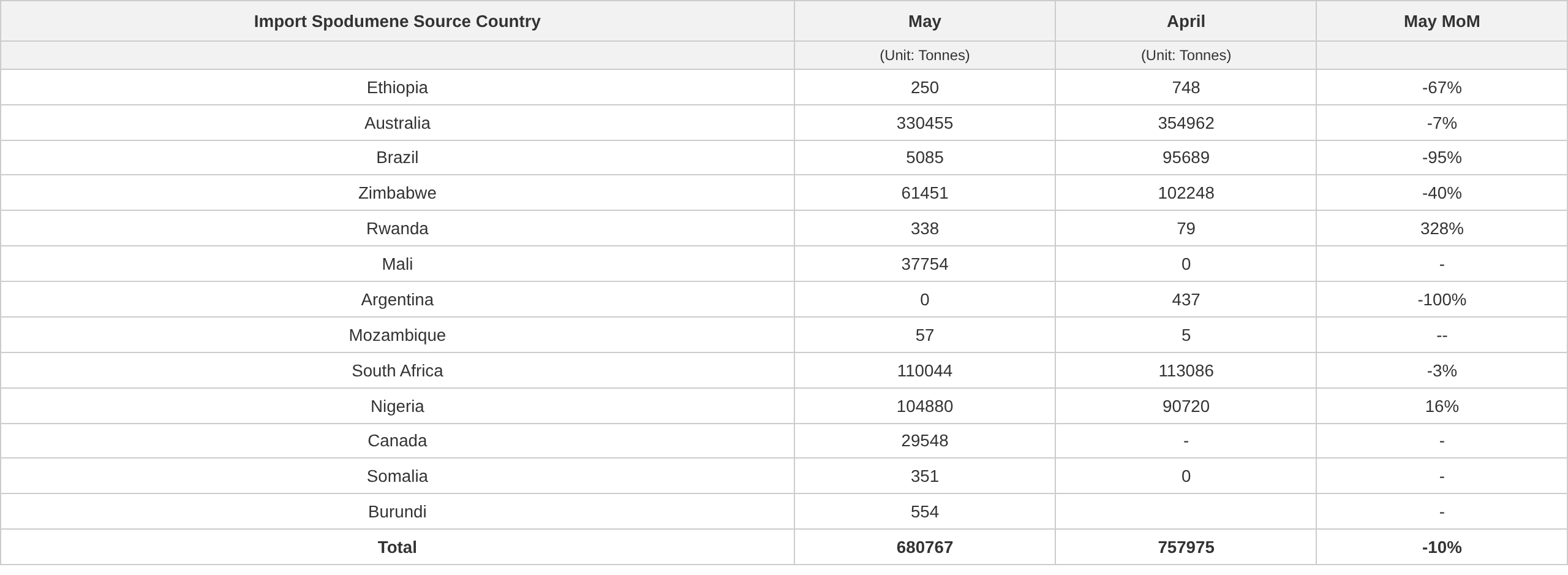

Customs data indicates that spodumene imports in May continued to pull back from April, reaching 681,000 mt in physical content. By source country, port arrivals of Australian ore returned to relatively normal levels, with arrivals exceeding 330,000 mt this month, down 6% MoM; shipments from Zimbabwe that were loaded earlier arrived at 63,800 mt this month, down 41% MoM; exports from South Africa and Nigeria from April to May were relatively stable, with port arrivals ranging from 90,000 to 110,000 mt per month. Arrivals from Mali were low this month, at only 38,000 mt, which increased MoM but have not returned to relatively high levels.

Additionally, after SMM screening, it can be seen that the incoming ore for the month was equivalent to 66,000 mt of LCE. Lithium concentrates accounted for 81% of the incoming ore, with the trend rising MoM compared to the previous month.

Source: China Customs, compiled by SMM

On the spot quotation for spodumene concentrates (CIF China), according to SMM spot quotes, the spot quotation for spodumene concentrates (CIF China) in May showed a trend of rising first and then falling. As of May 29, the spot quotation for spodumene concentrates (CIF China) was around $2,571/mt, up $31/mt from $2,540/mt at month-end April, an increase of 1.22%.

> Click to view SMM's spot quotes for new energy products

In May, enterprises that purchase spodumene externally for lithium extraction still hovered near the break-even line. At the beginning of the month, lithium carbonate prices rebounded, but spodumene concentrates followed suit and at one point rose more than salt prices, leading to continued losses. In the first half of May, lithium carbonate prices further rose, and non-integrated enterprises might briefly achieve slim profits on the spot; after mid-month, ore prices fluctuated at highs while lithium carbonate pulled back, causing enterprises to fall back into losses, which lasted until month-end. Enterprises that purchase lepidolite externally for lithium extraction continued to see stable profits in May. Although lepidolite concentrate prices fluctuated at highs due to tight supply, their increase was smaller than the rise in lithium carbonate, leaving profit margins for the smelting end. May 12: Yichun Mining auctioned 5,700 mt of 2% lepidolite concentrate at a transaction price of 5,760 yuan/mt, reflecting the tight balance at the ore end.

As of June 24, spodumene concentrate (CIF China) spot prices remained at $2,291/mt.

Lithium Carbonate

According to customs data, China imported 37,555 mt of lithium carbonate in May, up 15% MoM and up 78% YoY. Of this, 24,522 mt came from Chile (65% of total imports), 11,422 mt from Argentina (30%), and 1,023 mt from Indonesia (3%). From January to May, China’s cumulative lithium carbonate imports reached 153,000 mt, up 53% YoY.

In May, China exported 201 mt of lithium carbonate, down 46% MoM and down 30% YoY. Cumulative exports from January to May totaled 2,087 mt, up 1% YoY.

China imported 12,107 mt of lithium sulfate in May, down 33% MoM but up 53% YoY. Cumulative imports from January to May reached 71,000 mt, up 105% YoY.

According to SMM spot price data, spot lithium carbonate prices in May also showed a pattern of rising first and then falling. As of May 29, spot lithium carbonate prices stood at 177,500 yuan/mt, up 500 yuan/mt from 177,000 yuan/mt on April 30, an increase of 0.28%.

》Click to view SMM New Energy product spot prices

Looking back at the May lithium carbonate market, according to SMM, spot lithium carbonate prices in China fluctuated upward with a notable rise in the price center, and the average monthly price rose 12% MoM. From the fundamental side, supply-side disruptions continued to fester, while on the demand side, production schedules for downstream cathode materials and battery cells remained at high levels. The June production schedule is expected to accelerate further, and the supply-demand time mismatch remains unresolved. Upstream lithium chemical plants maintained firm prices and held back from selling throughout the month. The downstream showed divergence: some enterprises restocked on dips, but most had limited acceptance of high prices and mainly made just-in-time procurement, leaving actual transactions relatively sluggish. In May, spot battery-grade lithium carbonate prices kept rising amid fluctuations, with a notable gain at month-end compared to the start of the month. The most-traded futures contract briefly broke through the 200,000 yuan/mt mark during the month.

As of June 24, spot battery-grade lithium carbonate prices were quoted at 154,000-161,000 yuan/mt, averaging 157,500 yuan/mt. According to SMM, entering June, the lithium carbonate market saw a clear tug-of-war between longs and shorts, with the price center shifting significantly lower than in May. On the supply side, disruptions such as declining exports from Chile and license renewals for mines in Jiangxi provided bottom support for lithium carbonate prices. However, pressure from high warrant levels and expectations of Zimbabwean ore arrivals capped the upside for prices. Downstream material plants maintain a dip-buying strategy amid falling lithium carbonate prices, with stronger willingness to restock when prices hit psychological levels but lacking momentum to chase rallies. Upstream lithium chemical plants, on the other hand, still hold sentiment to hold prices firm. Currently, the tug-of-war between longs and shorts intensifies. In the future, close attention should be paid to the warrant inflection point, the arrival pace of Zimbabwe lithium ore, and the extent to which downstream production schedules materialize. Spot lithium carbonate quotes are expected to remain in the doldrums in the near term.

Lithium Hydroxide

According to customs data, in May 2026, China imported 3,932 mt of lithium hydroxide, down 41% MoM and up nearly fourfold YoY. Among them, imports from South Korea amounted to 2,029 mt, accounting for 51% of total imports; from Indonesia were 360 mt, marking a notable pullback; from Australia and Chile were 1,204 mt, making up 30%. In May, China exported 3,549 mt of lithium hydroxide, down 36% MoM and down 36% YoY, with 2,799 mt going to South Korea and 608 mt to Japan.

Battery Materials

LFP

In May 2026, China's LFP exports reached 7,625.4 mt, up 29.3% MoM from April and up 710.0% YoY from May last year, setting a new monthly high for the year. On the pricing front, total export value in May was $62.6062 million, with an average unit price of roughly $8,210/mt, equivalent to about 55,951 yuan/mt, up around 6.9% from the April average.

In terms of export destinations, there was a notable shift in May: exports to the US were the highest at 3,014.7 mt, leaping to first place; Thailand ranked second with 2,030.6 mt; exports to Malaysia totaled about 886 mt, ranking third; Japan and Vietnam recorded 620 mt and 420 mt, respectively. Compared with April, exports to Vietnam and Thailand increased significantly, while those to Poland and Canada declined. The overall export center shifted towards Southeast Asia and the US, which is closely related to the locations of battery cell manufacturers' clients.

Overall, overseas demand remains robust. China's total LFP exports kept increasing, achieving multiple-fold growth YoY. In the future, as overseas battery capacity gradually comes onstream, China's LFP exports are expected to stay high.

LiPF6

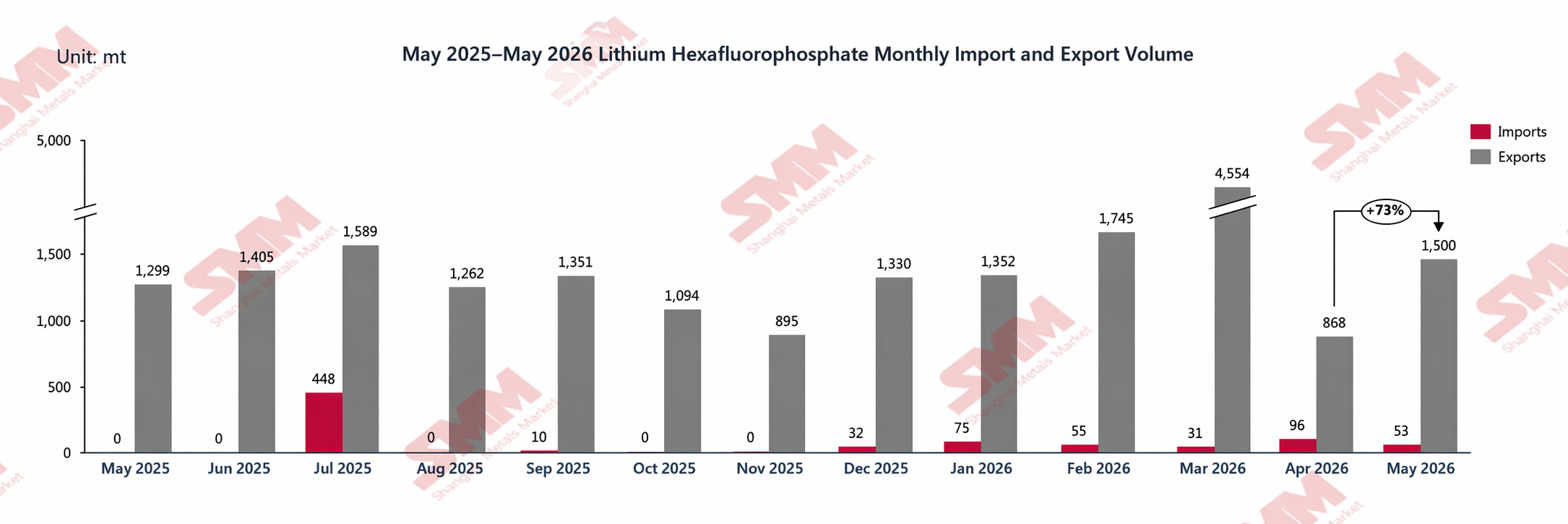

According to China customs data, in May 2026, China's cumulative exports of LiPF6 were approximately 1,500 mt, up about 72.8% MoM, while cumulative imports of LiPF6 were about 53.5 mt.

On the export front, in May 2026, China's LiPF6 exports were about 1,500 mt, up about 72.8% MoM from April and up about 15.5% YoY. Specifically, this month, LiPF6 was mainly exported to South Korea, Poland, Malaysia, Japan, and other countries. Exports to Poland were 451.88 mt, up about 33.89% MoM; exports to South Korea were 591.006 mt, up about 622.47% MoM; exports to Japan were 109.8 mt, down about 42.62% MoM; and exports to the US were 77.4 mt, down about 24.05% MoM. Overall, overseas procurement volume for LiPF6 recovered somewhat in May.

Artificial Graphite

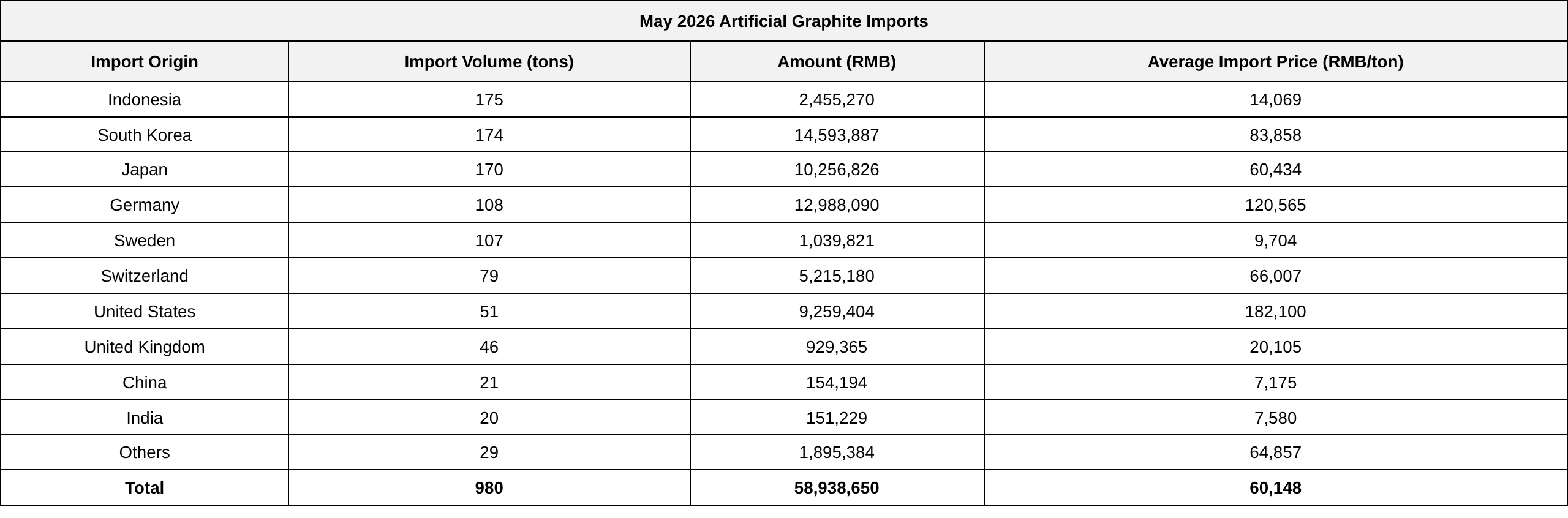

In May 2026, China's artificial graphite imports were 980 mt, up 29.5% MoM but down 21.8% YoY. In terms of the average import price, in May 2026, the average import price of China's artificial graphite stood at 60,148 yuan/mt, down 20.8% MoM but up 37.3% YoY.

In May 2026, China's artificial graphite exports were 50,038 mt, up 9.03% MoM but down 4% YoY. In terms of the average export price, in May 2026, the average export price of China's artificial graphite stood at 7,729 yuan/mt, down 16.12% MoM and down 12.91% YoY.

Looking at the overall export data, while total artificial graphite exports recorded MoM growth in May, the combined shipments of the top five exporting provinces in China registered a 19% MoM pullback. Performance by province diverged significantly, with two provinces seeing their exports down sharply 40% MoM, another province posting an MoM decline approaching 30%, and major production regions showing marked export weakness.

Flake Graphite

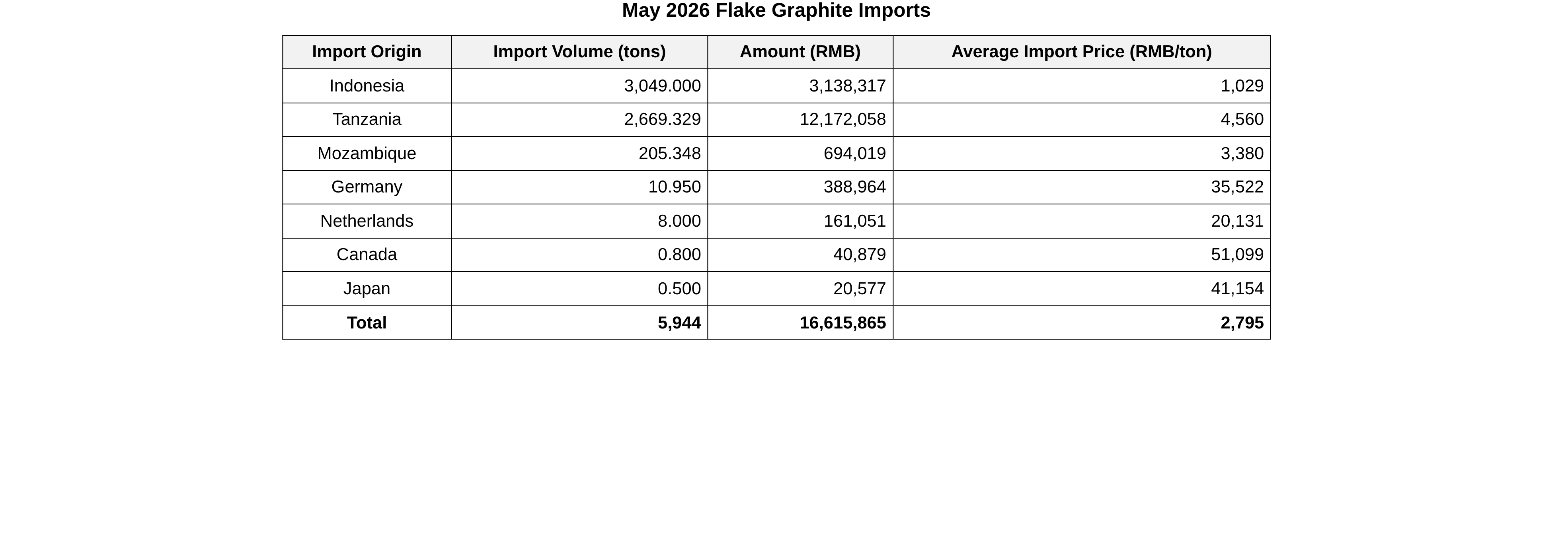

In May 2026, China's flake graphite imports were 5,944 mt, up 87% MoM and up 22% YoY.

Data source: China Customs, SMM

In May 2026, China's flake graphite exports were 7,641 mt, up 87% MoM but down 12% YoY.

The significant 87% MoM rise in flake graphite exports in this period was mainly driven by the low base effect stemming from the delayed delivery of export orders in April. Affected by earlier logistics delays, production schedule postponements, and other factors, export shipments in April were at a relatively low level, and previously backlogged export orders were concentrated for customs declaration and shipment in May, driving a sharp MoM increase in export volumes this month.

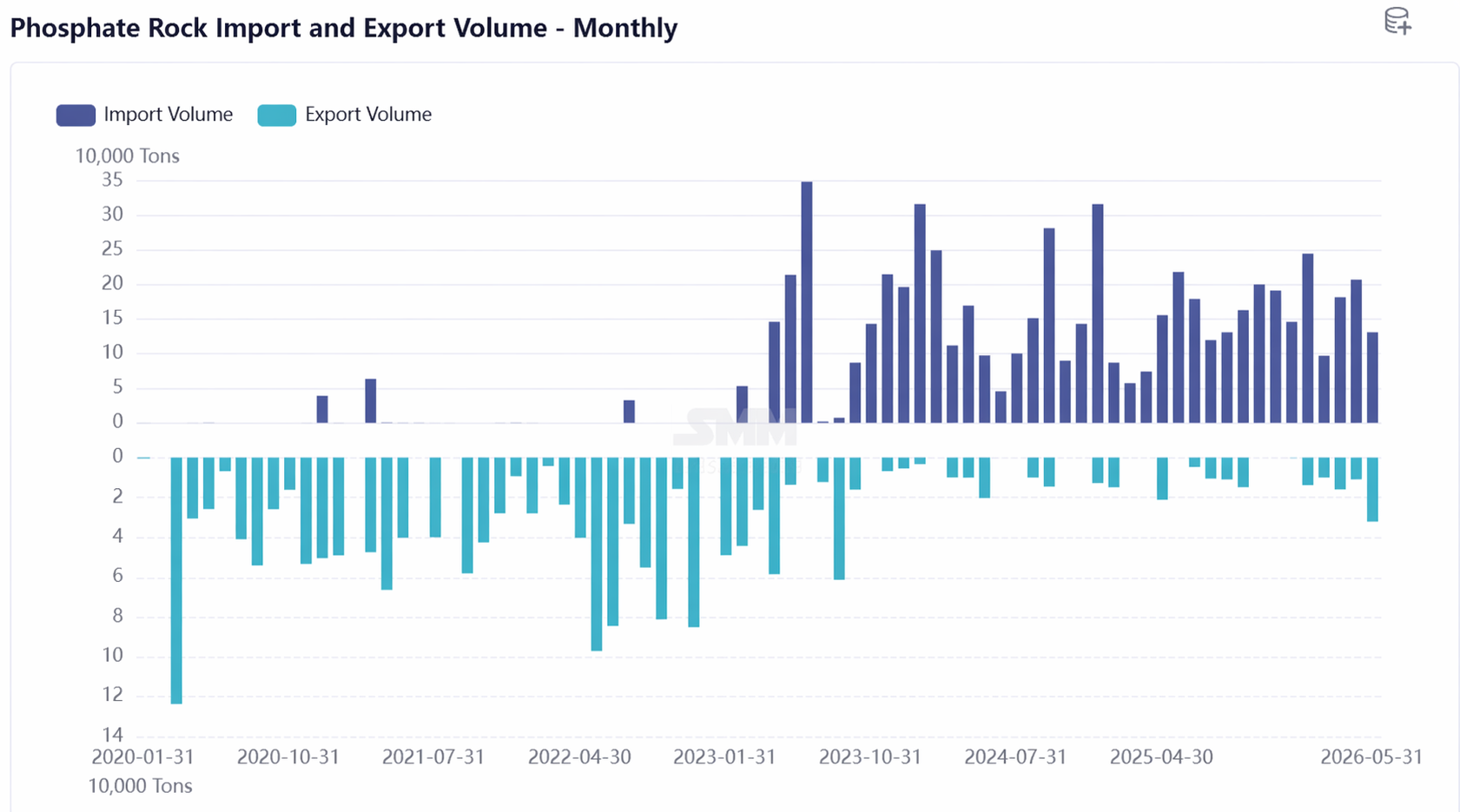

Phosphate Ore

In May 2026, China's phosphate ore imports stood at 131,000 mt, down 36.4% MoM, with an average price of $93/mt, down slightly 2.6% MoM. Import sources were highly concentrated in Egypt (128 kt, accounting for 97.7%), while shipments from Peru and Jordan were interrupted. Exports stood at 32 kt, up 189.6% MoM, with Hubei resuming exports of 21 kt. The Egyptian government halted new export contracts in mid-May, intensifying supply uncertainty going forward, which may further pressure import costs. The provincial mix shifted dramatically as Hubei imports fell to zero and Guangxi reclaimed the top spot.

Characteristics of China’s phosphate ore import market in May:

First, total volume pulled back significantly, with imports down more than one-third MoM; second, sources were highly concentrated, with Egypt alone accounting for as much as 97.7%, while shipments from Peru and Jordan were interrupted; third, the provincial mix shifted dramatically, as Hubei imports fell to zero and Guangxi reclaimed the top spot. The Egyptian government announced in mid-May that it would stop signing new phosphate ore export contracts. The uncertainty surrounding Egyptian cargo supply will rise markedly in the coming months, potentially pushing import costs higher and exacerbating tight supply. At the same time, the recovery in exports from Hubei and Guizhou reflects a rebalancing of the regional supply-demand pattern for domestic phosphate ore.

Cobalt

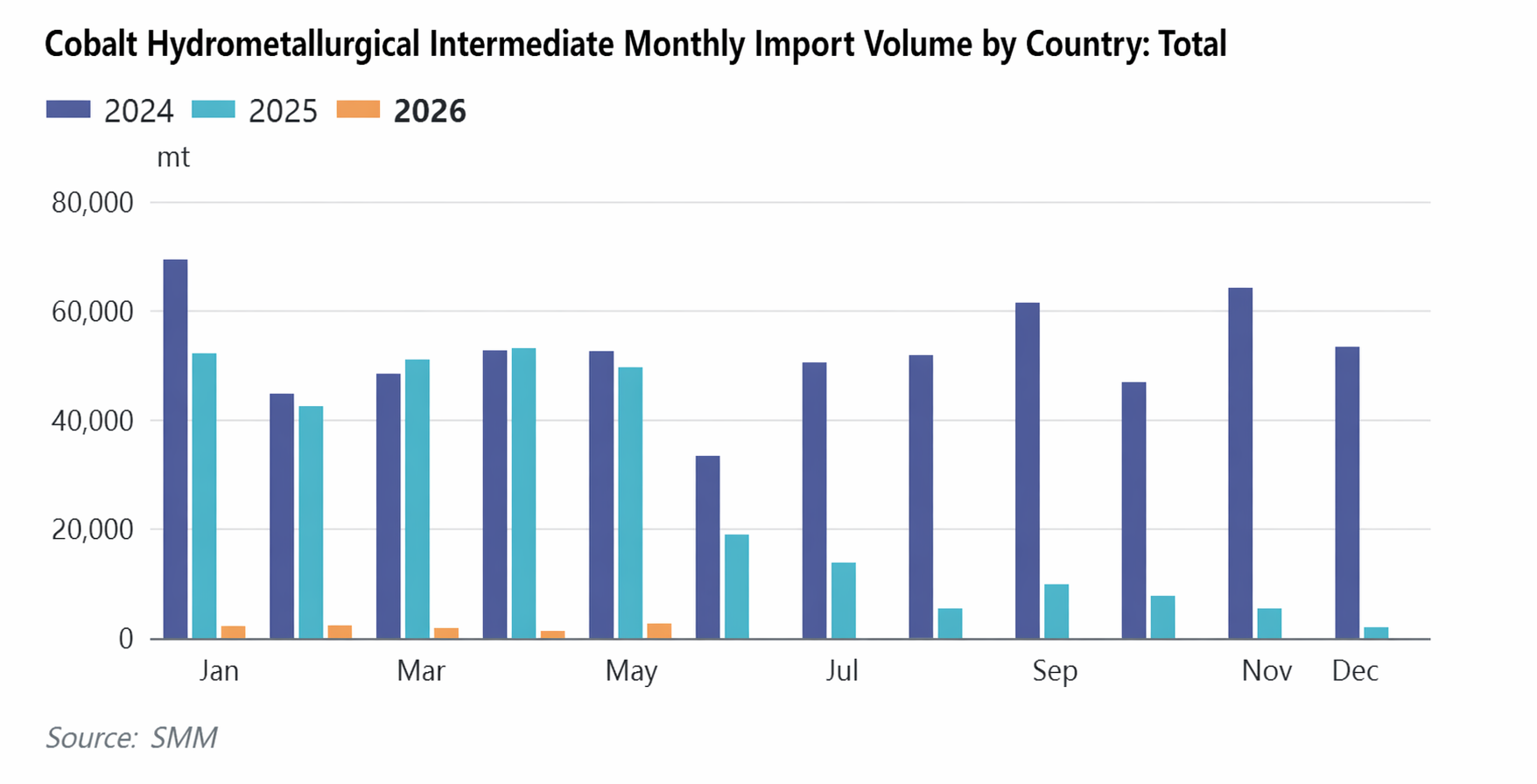

Cobalt Hydrometallurgy Intermediate Products

In May 2026, China’s imports of cobalt hydrometallurgy intermediate products were approximately 2,584 mt in physical content, up 107% MoM and down 95% YoY. Imports from the DRC were approximately 2,066 mt in physical content, up 119% MoM and down 96% YoY. The average import price of cobalt hydrometallurgy intermediate products in China in May 2026 was $16,607/mt in physical content, down 3.37% MoM. Reports indicate that some Chinese-invested miners have gradually increased chartered shipments since May, with several leading miners progressively resuming shipments from June onward. Port arrivals of intermediate products are expected to slowly pick up in the coming months and are likely to achieve bulk arrival volumes after August.

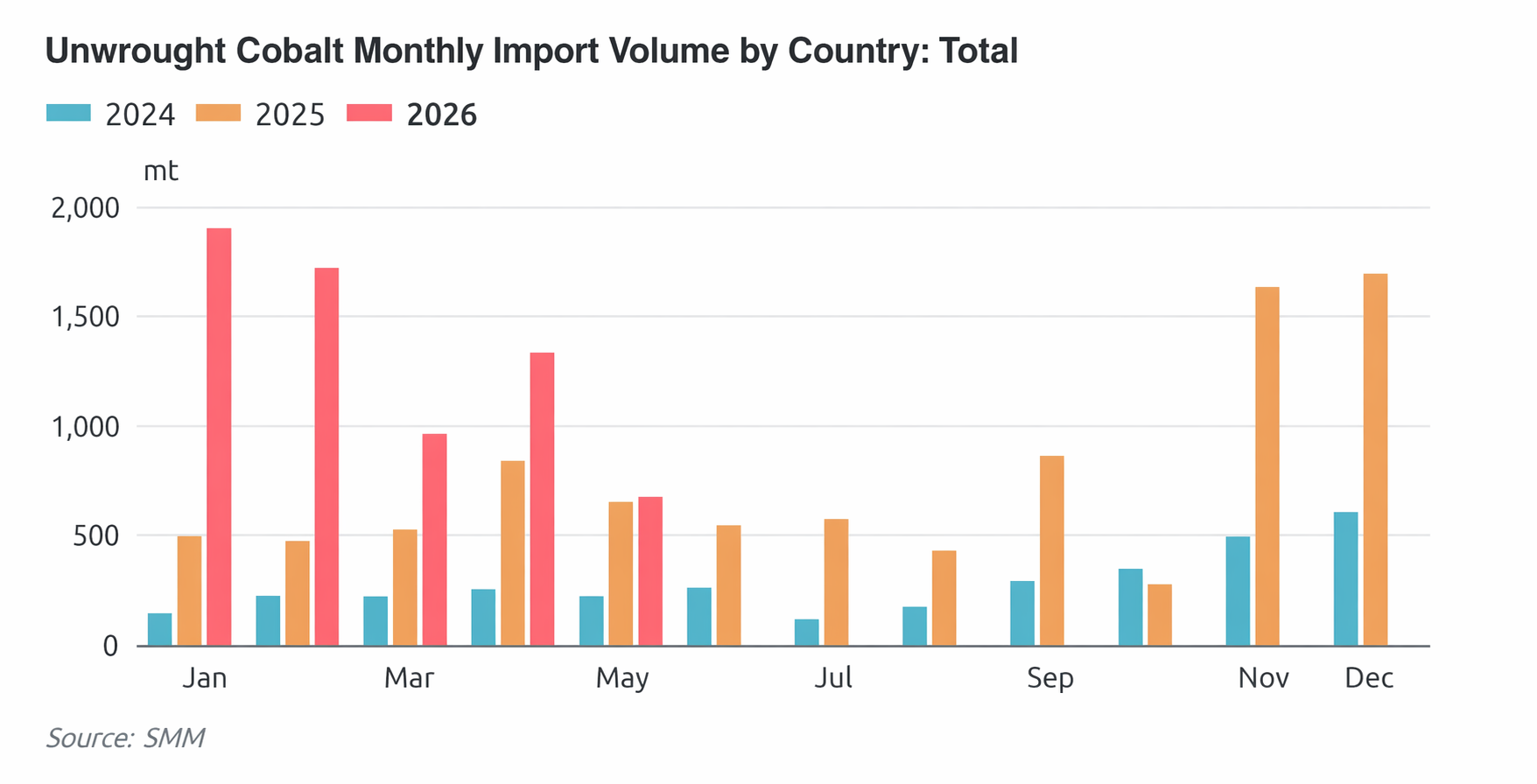

Unwrought Cobalt

In May 2026, China’s imports of unwrought cobalt were approximately 673 mt, down 50% MoM and up 3% YoY. In May, the top three sources by refined cobalt import volume were Indonesia (211 mt), Madagascar (93 mt), and Canada (85 mt). The sharp MoM decline in imports was mainly due to the depletion of low-priced cobalt raw materials previously accumulated outside China, while newly imported cobalt plates and cobalt briquettes were priced higher than other domestic cobalt raw materials, reducing smelters’ willingness to purchase for dissolution. The average import price of unwrought cobalt in China in May 2026 was $54,557/mt, up 3.48% MoM. Cumulative imports in January-May 2026 totaled 6,589 mt, up 120% YoY.

Exports, in May 2026 China's unwrought cobalt exports were approximately 370 mt, up 70% MoM and down 88% YoY. By destination, exports to the Netherlands surged to 205 mt in May, up 791% MoM. Average export price, the average export price of China's unwrought cobalt in May 2026 was $53,403/mt, down 2.17% MoM. Cumulative exports in January-May 2026 totaled 2,161 mt, down 79% YoY.