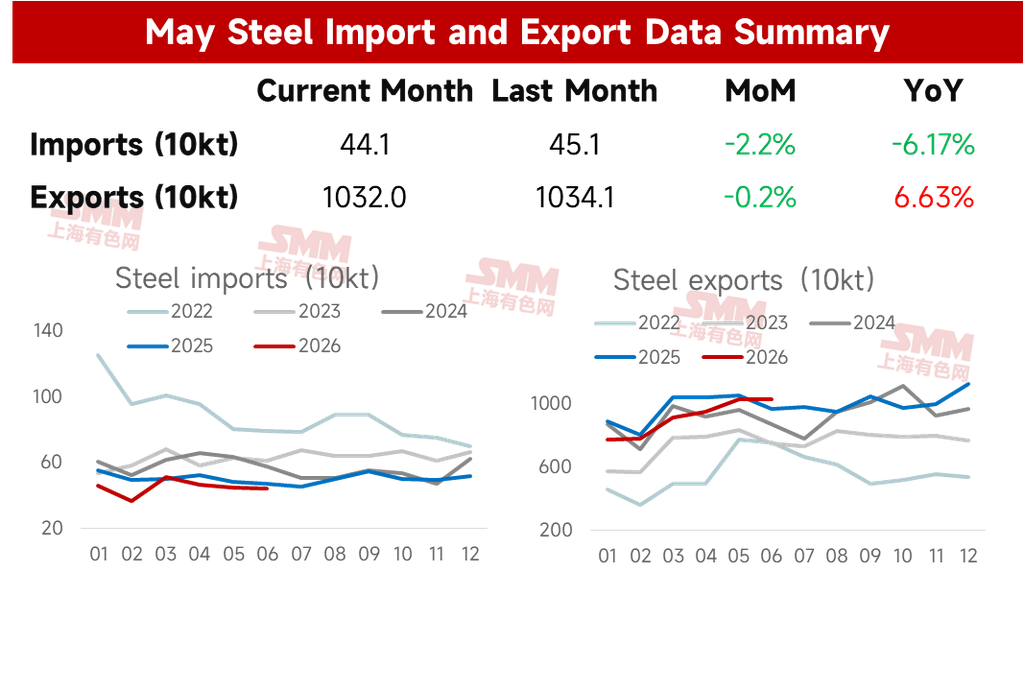

On July 14, data from the General Administration of Customs showed that China exported 10.32 million mt of steel in June 2026, down 21,000 mt MoM or 0.2% MoM. Cumulative exports from January to June reached 54.874 million mt, down 5.6% YoY.

In June 2026, China imported 441,000 mt of steel, down 10,000 mt MoM or 2.2% MoM. Cumulative imports from January to June were 2.696 million mt, down 11.3% YoY.

Table 1: Overview of Steel Imports and Exports, January-June

Source: SMM

- Steel Exports Remained High in June

According to SMM's June export production schedule survey, planned HRC export volume for the month stood at 1.05 million mt, slightly lower than actual exports in May, with a relatively limited decline. Meanwhile, SMM export order data showed that steel export orders remained high in mid-April, laying the foundation for high steel exports in May-June.

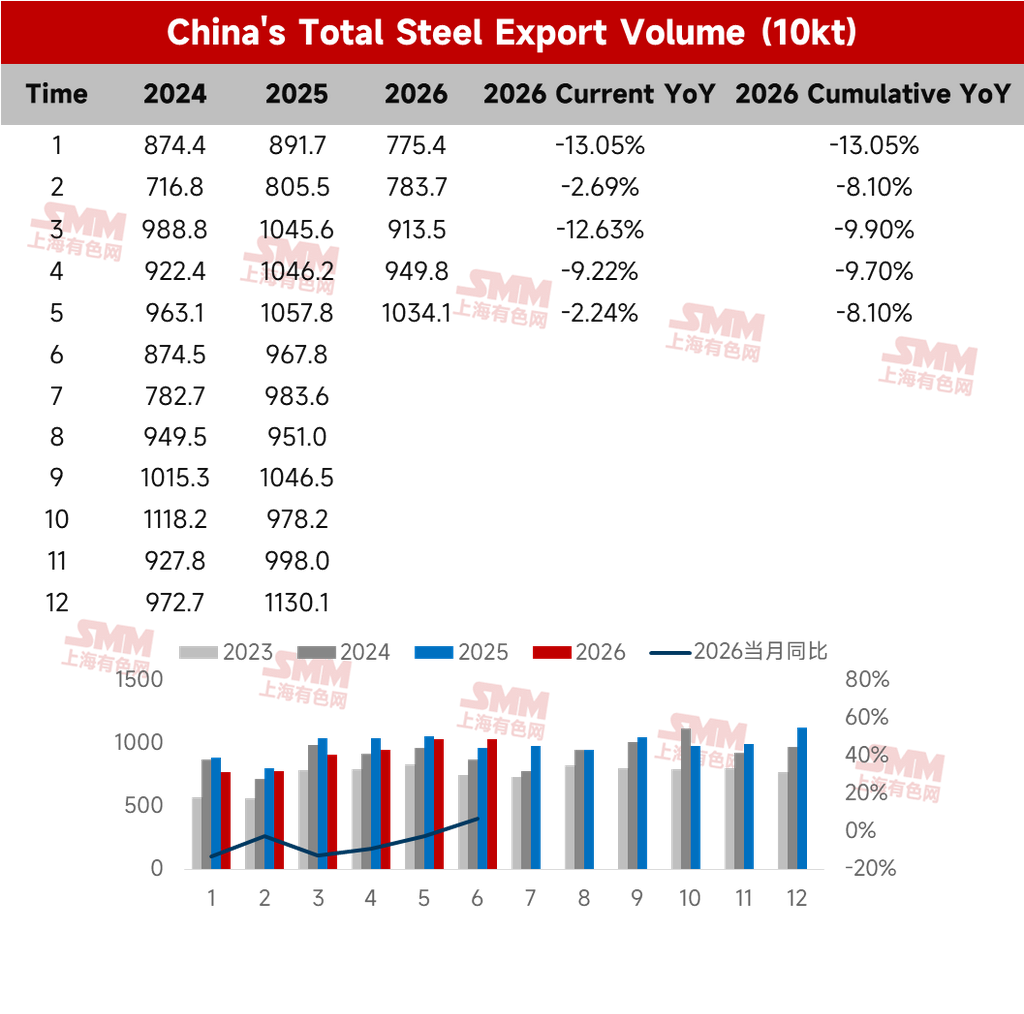

Table 2: China’s Total Steel Exports

Source: SMM

- Steel Imports Stayed Low in June

On the import side, steel imports in June were 441,000 mt, down MoM. January-June cumulative imports were 2.696 million mt, down 11.3% YoY. Net steel exports reached 52.178 million mt.

- Short-Term Steel Export Outlook

1. Global Manufacturing Declined MoM; Domestic New Export Orders Recovered Marginally

According to J.P. Morgan global PMI data, the global manufacturing PMI stood at 52.2 in June 2026, still in expansion territory but with momentum slowing for a second consecutive month, mainly due to earlier stockpiling to avoid Middle East shipping risks, while preventive stockpiling demand waned in June. In addition, end-use consumer goods demand in Europe and the US was weak, global export orders fell below the 50 mark, and the ASEAN composite PMI dropped 1 point MoM, with regional sentiment cooling significantly. China's manufacturing new export orders index at 50.1% in June, up 1.5 percentage points MoM, pointed to a marginal recovery in external demand.

2. Supply Outside China Rose MoM; Overall Supply Pressure Intensified

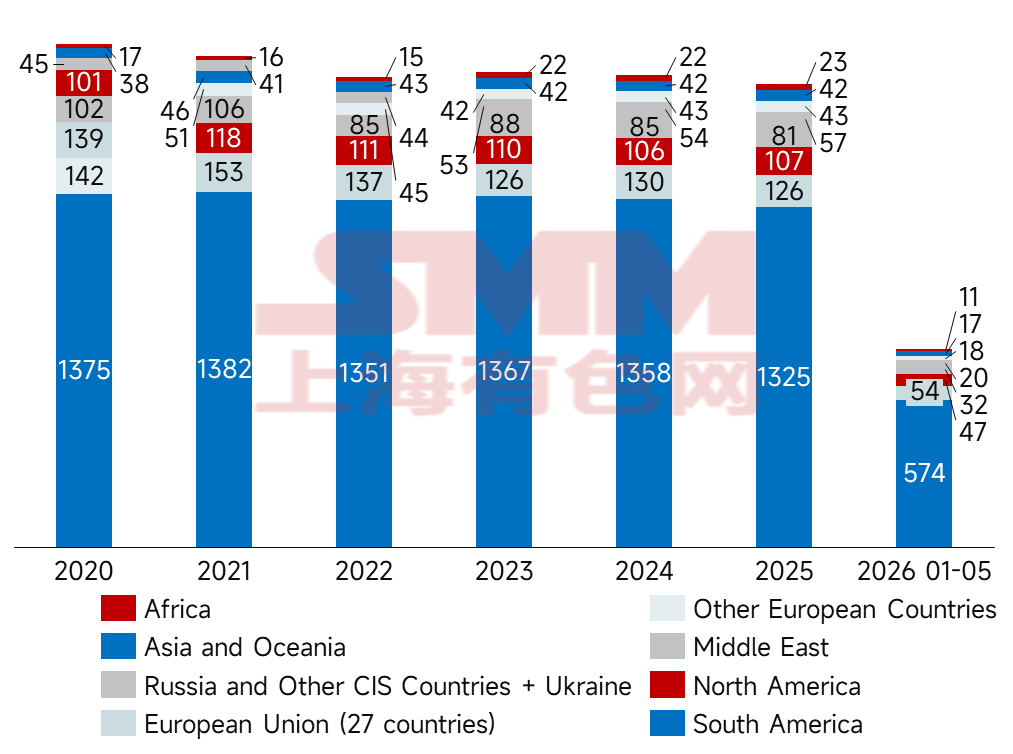

Global crude steel production fell 0.3% YoY to 157.9 million mt in May 2026. In China, against a severe backdrop of finished steel destocking falling short of expectations and losses, steel mills proactively brought forward maintenance plans to defensively control output. Excluding China, production in the rest of the world rose 28.8% YoY. The Asian market was unusually resilient, with India's crude steel production recording 14.1 million mt. Meanwhile, Vietnam's production surged 27.2% YoY, driven not by a stress response to trade barriers but by downstream manufacturing entering a concentrated stockpiling phase, coupled with genuine demand from infrastructure projects rushing to meet deadlines ahead of the monsoon season. In contrast, production in the Middle East plunged 19.4% YoY in May, with previous war damage from geopolitical conflicts and wartime energy controls remaining an invisible and heavy ceiling suppressing production resumptions in the region. Production regions in Europe and the US (the US up 9.2% YoY, Germany up 7.3% YoY) maintained relatively active operating rates, supported by new-type data center infrastructure and anticipatory moves to preempt regional trade barriers such as the EU's Carbon Border Adjustment Mechanism (CBAM). It is reported that the Middle East recently started offering billet exports and concluded deals. Meanwhile, increased production in India, Vietnam and others also put some pressure on domestic exports.

Figure 1: Global Crude Steel Production by Region

Source: SMM

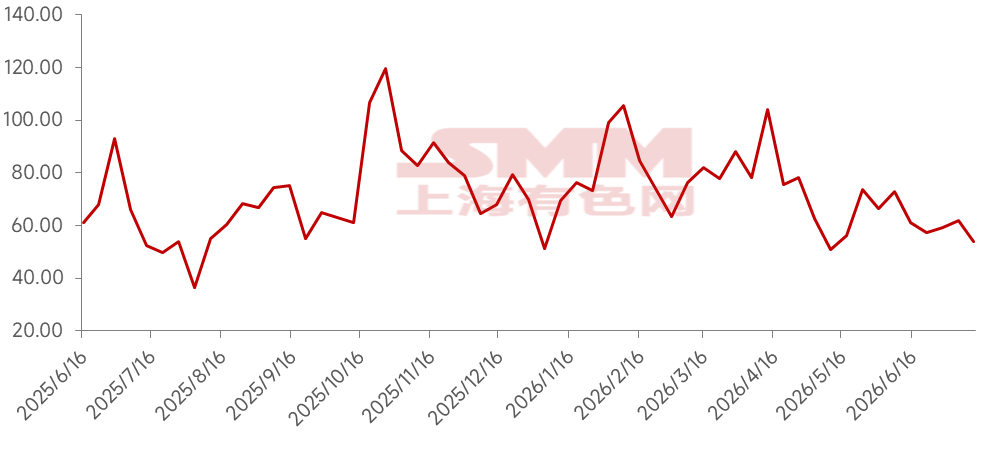

3. Price Advantage Narrowed Significantly; Pressure on Export Orders Intensified

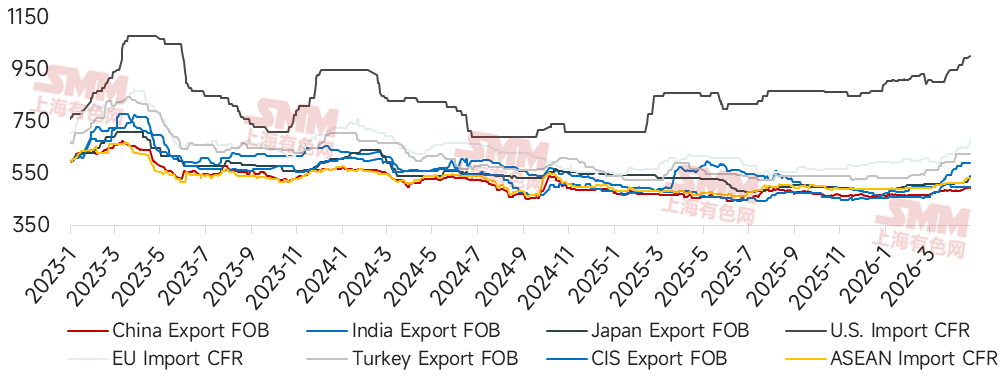

As of July 16, 2026, HRC export quotations (FOB) for India, Turkey, and the CIS were $510/mt, $408/mt, and $530/mt, respectively, while China's HRC export quotation (FOB) was $493/mt. Currently, China's HRC export quotations are $17/mt, $115/mt, and $37/mt lower than those countries. China's steel export price advantage narrowed significantly MoM from June. The overseas market remained in the off-season, and low-price export promotion remained the main channel for them to relieve domestic pressure. In China, prices remained relatively firm supported by costs. The price spread between Chinese and overseas markets narrowed markedly, intensifying pressure on export orders.

Figure 2: HRC Quotations in Major Global Markets

Source: SMM

4. Export Orders Remained at Low Levels in May-June; A Sudden Increase Is Difficult

According to SMM's latest steel mill export order schedule, planned HRC exports for this month totaled 1.059 million mt, up 5.2% MoM from actual exports last month. SMM's steel export order data showed that due to the ongoing overseas off-season and consecutive overseas price declines, steel export orders in May-June declined significantly MoM from the previous period.

Figure 3: SMM Steel Export Order Volumes

Source: SMM

5. Anti-Dumping Cases with Impact Increased in June

New anti-dumping related cases in China increased in June, involving products such as steel pipes, coated sheets, cold-rolled, stainless steel, hot-rolled, and medium-thickness plates. Details of the cases and their impact volumes are shown in the table below.

Table 3: New Anti-Dumping Cases in June

Source: SMM

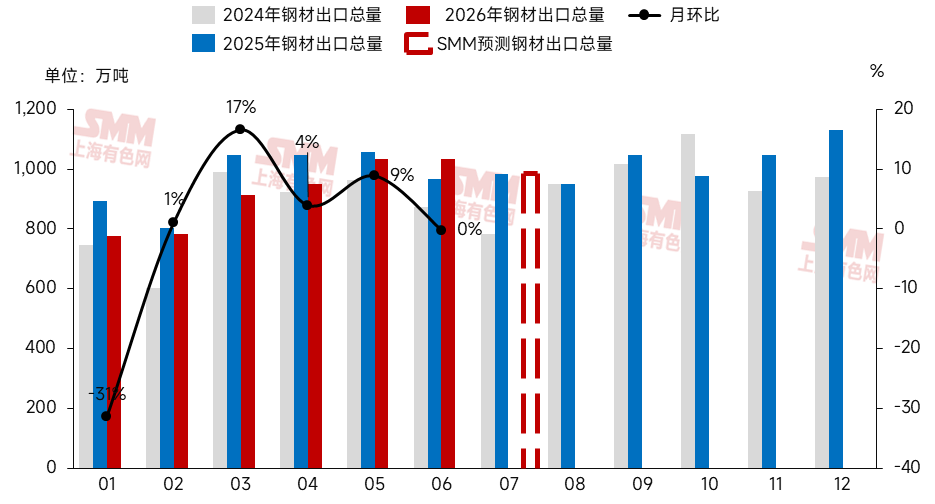

Overall, against the backdrop of the overseas off-season coupled with a narrowing price advantage, the weakness in earlier export orders may gradually be reflected in export data. SMM expects that actual steel exports in July will face some downward pressure. However, as overseas prices continue to pull back and hit bottom, some new procurement demand may be released.

Figure 4: Steel Exports and Forecast, 2024-2026

Source: SMM

Source Declaration: All data other than publicly available information is processed by SMM based on public information, market communication, and SMM's internal database models, and is for reference only and does not constitute any decision-making advice.

Note: This article is original content of this official account. If you need to reprint, whitelist, or cooperate, please contact us. Without permission, no one may reprint, modify, use, sell, transfer, display, translate, compile, disseminate, or otherwise disclose the above content to any third party or permit any third party to use it. Otherwise, Shanghai Metals Market (SMM) will pursue legal liability for infringement, including but not limited to claiming contractual breach of contract liability, disgorgement of unjust enrichment, and compensation for direct and indirect economic losses. Scan to Get Free Information

![[Indian billet cargo vessel partially sinks in Strait of Hormuz, UAE supply faces disruption]](https://imgqn.smm.cn/usercenter/FFFrV20251217171719.jpg)