SMM June 4 News:

Metals market:

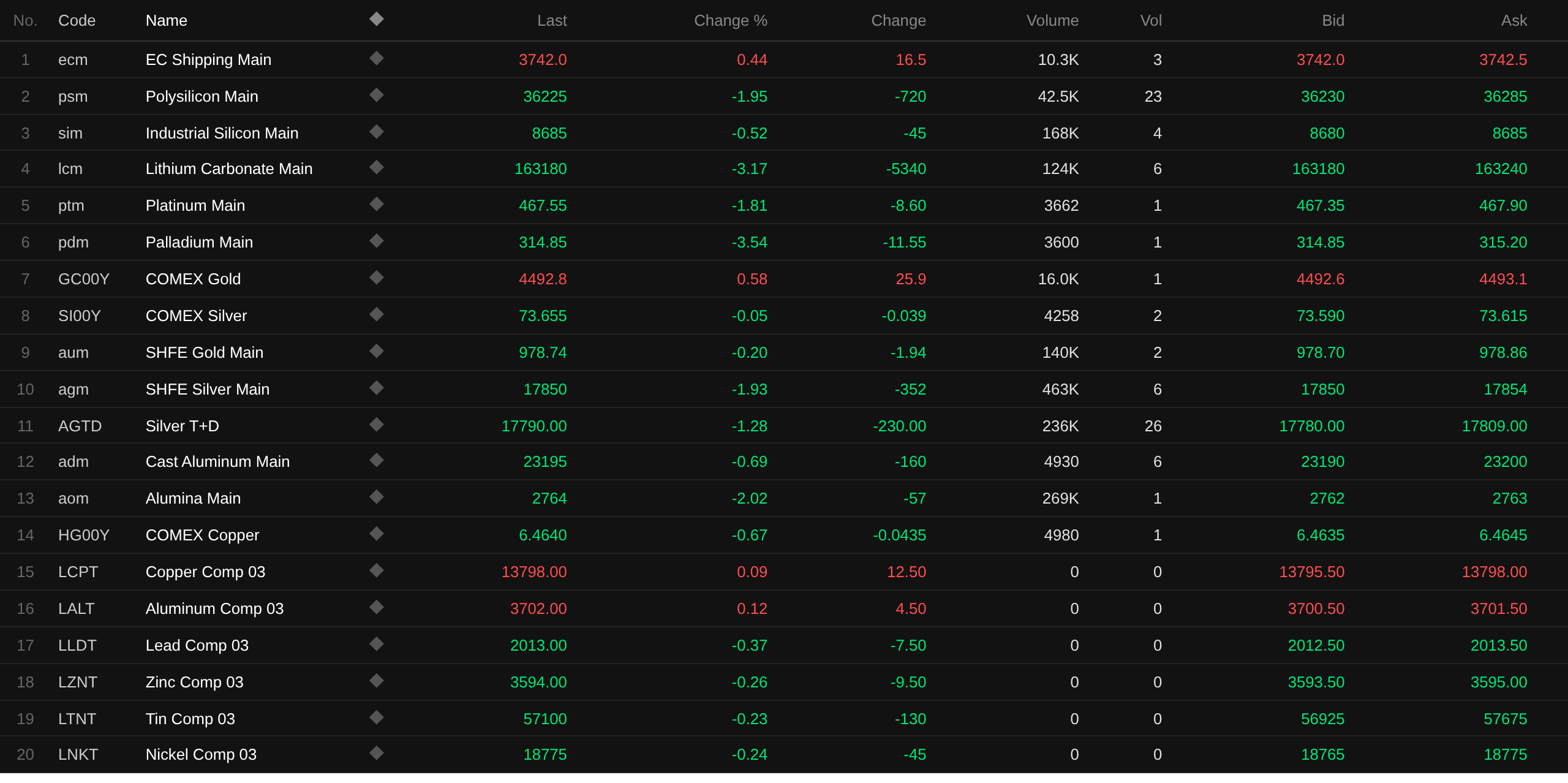

As of the midday close, domestic market base metals fell across the board. SHFE copper, SHFE aluminum, SHFE lead, and SHFE zinc all dropped over 1%. SHFE tin fell 0.86%. SHFE nickel fell 2.55%.

In addition, the most-traded casting aluminum futures fell 0.69%, and the most-traded alumina futures fell 2.02%. The most-traded lithium carbonate futures extended the decline from the previous three trading days, falling another 3.17%. The most-traded silicon metal futures fell 0.52%. The most-traded polysilicon futures fell 1.95%.

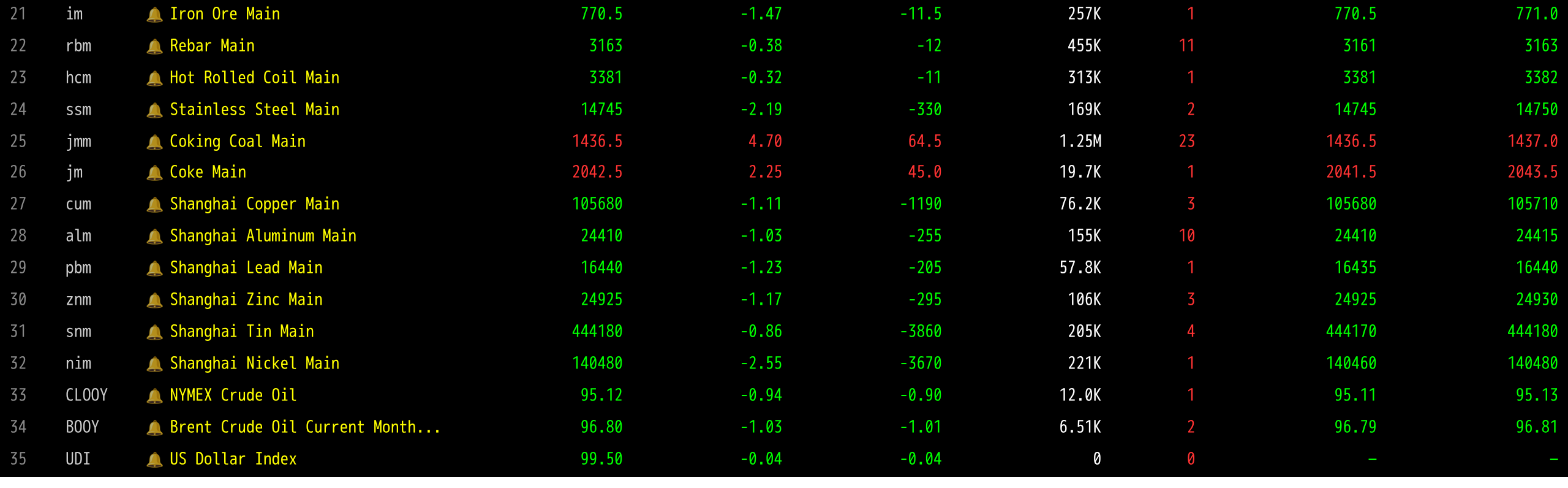

Ferrous metals mostly fell. Iron ore dropped 1.47%, rebar fell 0.38%, hot-rolled coil fell 0.32%, and stainless steel fell 2.19%. Coking coal and coke: the most-traded coking coal contract rose 4.7%, and the most-traded coke contract rose 2.25%.

Overseas market base metals: as of 11:45, LME metals generally fell. LME copper fell 0.09%, LME aluminum fell 0.12%, and LME lead fell 0.37%. LME zinc, LME tin, and LME nickel all fell within 0.3%.

Precious metals: as of 11:45, COMEX gold rose 0.58%, and COMEX silver fell 0.05%. Domestic market precious metals: the most-traded SHFE gold futures fell 0.2%, and the most-traded SHFE silver futures fell 1.93%.

In addition, as of the midday close, the most-traded platinum futures fell 1.81%, and the most-traded palladium futures fell 3.54%.

As of the midday close, the most-traded Europe containerized freight index contract rose 0.44% to 3,758 points.

As of 11:45 on June 4, midday futures quotes for selected contracts:

Spot and fundamentals

Aluminum:On June 4, SMM A00 aluminum (Foshan) was quoted at 24,130, down 190, at a discount of 190 to the current-month contract, narrowing by 60 (unit: yuan/mt). Futures stopped rising and turned lower today, while South China spot prices bucked the trend and stabilized with an upward bias...

Macro front

Domestic:

[MIIT: From January to April, China's above-scale electronic information manufacturing value-added output was up 14% YoY]From January to April, the value-added output of above-scale electronic information manufacturing was up 14% YoY, 8.4 and 1.4 percentage points higher than the growth rates of overall industry and high-tech manufacturing over the same period, respectively. In April, the value-added output of above-scale electronic information manufacturing was up 15.6% YoY. Among major products, mobile phone production reached 452 million units, up 0.3% YoY, of which smartphone production was 390 million units, up 6.5% YoY; micro-computer equipment production was 95.426 million units, down 10% YoY; integrated circuit production was 176.97 billion units, up 24.7% YoY. (MIIT Weibo)

[State Grid Corporation of China's Peak Power Load to Exceed 1.3 Billion kW This Summer, Up ~6% YoY] According to State Grid Corporation of China, this summer's maximum power load in its operating area was projected to exceed 1.3 billion kW, up approximately 6% YoY. To fully ensure safe power grid operation and reliable power supply, State Grid Corporation of China accelerated supply assurance capacity building, continued to improve market-based power trading, and promoted efficient utilization of clean energy. Currently, 168 key projects for peak summer power supply were under accelerated construction. (CCTV)

The PBOC announced that, based on the demand of primary dealers in open market operations, the volume of the 7-day reverse repo operation on June 4 was zero. 101.3 billion yuan in reverse repos matured today.

US dollar:

As of 11:45, the US dollar index fell 0.04% to 99.5. According to the CME "FedWatch": the probability of the US Fed keeping rates unchanged through June was 98.4%, with a 1.6% probability of a cumulative 25 bps interest rate cut. The probability of the US Fed keeping rates unchanged through July was 90.2%, with an 8.4% probability of a cumulative 25 bps rate hike and a 1.4% probability of a cumulative 25 bps interest rate cut.

US Fed's Logan stated that US Fed officials may need to raise interest rates later this year to bring inflation down to the 2% target. She noted that the US labour market was "broadly in balance," investment in artificial intelligence was booming, and financial conditions remained "accommodative." However, she added that the current inflation trajectory did not appear to be pulling back toward the US Fed's 2% target. "These conditions suggest that current monetary policy is not restraining the economy," "I am increasingly concerned that achieving a full restoration of price stability, while appropriately balancing both sides of the US Fed's dual mandate, may require raising interest rates later this year."

The US Fed Beige Book noted that overall, prices rose at a moderate to strong pace, with most districts reporting inflation rates higher than in the previous report. Districts cited energy costs related to the Middle East conflict as a primary driver of inflationary pressures, with impacts extending to shipping, packaging, groceries, and fertilizers. Non-labour costs continued to rise faster than selling prices, raising broader concerns about margin compression. The ability to pass on higher costs varied across industries, particularly among consumer-facing companies. Some regions noted that enterprises across multiple areas had adopted strategies to cope with inflation, including supply chain optimization, product adjustments, reducing supply, and temporarily absorbing higher costs to maintain client demand. (Jin10 Data APP)

Data:

Data to be released today included US May Challenger enterprise layoffs, US initial jobless claims for the week ending May 30, US May Global Supply Chain Pressure Index, Eurozone April retail sales MoM, Switzerland May CPI MoM, and Switzerland May seasonally adjusted unemployment rate.

In addition, at 2:00 the US Fed released the Beige Book on economic conditions, and 2026 FOMC voter and Dallas Fed President Logan delivered a speech. At 15:00, the Ministry of Commerce held the first regular press conference of June, and China's refined oil products entered a new round of price adjustment window. ECB President Lagarde delivered a speech, 2027 FOMC voter and Richmond Fed President Barkin participated in a fireside chat, and Bank of England Governor Bailey spoke at the Investment Association conference.

Crude oil:

As of 11:45, oil prices in both markets declined, with WTI down 0.94% and Brent down 1.03%. According to CCTV News, on local time June 3, US President Trump stated that negotiations with Iran were progressing very well and a new round of talks could be held this weekend. Once an agreement is signed, the Strait of Hormuz will immediately reopen. (Jin10 Data APP) Expectations of an end to Middle East conflicts put oil prices under pressure.

Investinglive analyst Eamonn Sheridan stated that reports indicated Israel and Lebanon had reached a ceasefire framework agreement under US guidance, with both sides set to resume full talks during the week of June 22, contingent on Hezbollah's complete withdrawal from southern Lebanon. The geopolitical risk premium in the oil market will digest this headline and largely treat it as a priced-in factor. (Jin10 Data APP)

The US-Iran conflict is pushing the global oil market toward a tipping point. US crude oil and petroleum product inventory has fallen to its lowest level in over two decades, while US crude oil exports hit a record high in May, rapidly depleting domestic reserves. Analysts warned that if the Strait of Hormuz remains closed, oil prices could surge significantly within weeks. According to data released by the US Energy Information Administration (EIA) on Wednesday, for the week ending May 29, total US crude oil and petroleum product inventory decreased by 10.6 million barrels from the previous week to 1.57 billion barrels, the lowest level since 2004. Commercial crude oil inventory (excluding the Strategic Petroleum Reserve) fell by 8 million barrels in a single week to 433.7 million barrels, marking the sixth consecutive weekly decline, far exceeding analysts' prior expectations of 3.3 million barrels. (Wall Street Journal)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

![BC Copper Retreated After Rapid Rise with Sharp Decline, Geopolitical and Data Under Pressure Narrowing Inversion [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/KytYP20251217171712.jpg)

![Bulls Took Profits and Exited, SHFE Zinc Declined [SMM SHFE Zinc Brief Review]](https://imgqn.smm.cn/usercenter/EviJV20251217171754.jpg)

![Declining Copper Prices Stimulated Consumption, Converging Price Spread Between Futures Contracts Supported Narrowing of Shanghai Spot Copper Discounts [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/pJSbE20251217171713.jpeg)