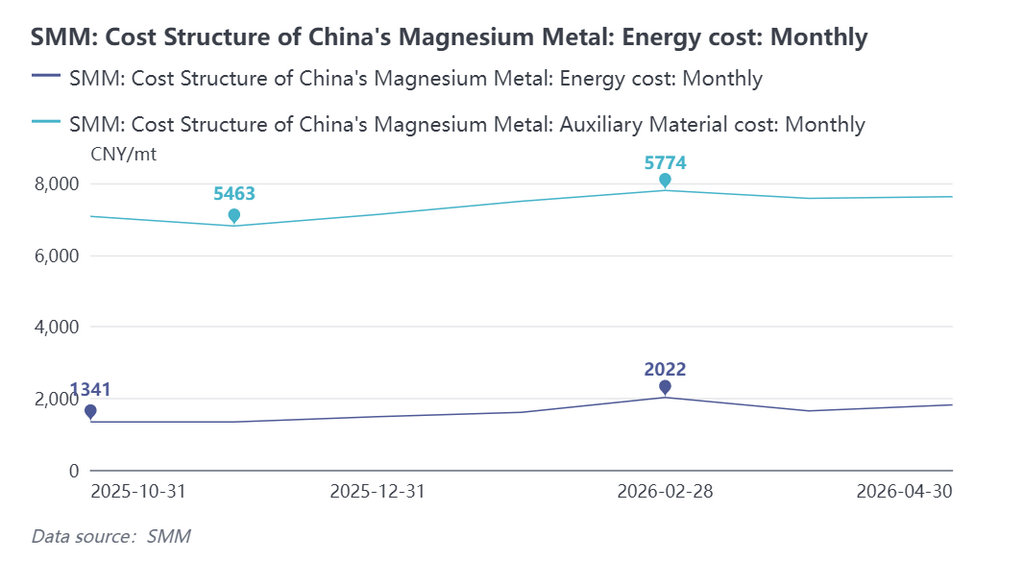

В настоящее время цены на коксовый газ демонстрировали колеблющуюся тенденцию с резкими скачками, что обусловлено главным образом балансом спроса и предложения на уголь, сезонным регулированием и корректировкой энергетической политики, при этом ценовые колебания значительно превысили показатели предыдущих лет. Основная причина заключалась в том, что отрасль полукокса не могла самостоятельно абсорбировать рост затрат на уголь, что приводило к серьёзному дисбалансу в передаче издержек. При росте цен на уголь полукоксовые предприятия могли переносить лишь незначительную часть затрат, тогда как основная их доля амортизировалась первичными магниеплавильными заводами, и эта тенденция продолжала усиливаться.

В последнее время рыночные цены на ферросилиций демонстрировали относительно умеренную динамику. С 2026 года основные цены на ферросилиций марки 75 оставались стабильными в диапазоне 5 700–6 100 юаней/т, а влияние ферросилиция на себестоимость магния значительно ослабло. В целом энергетические затраты заменили вспомогательные материалы в качестве ключевого фактора, определяющего ценовые тенденции на магний.

Устойчивые убытки в полукоксовой отрасли привели к значительному росту затрат на коксовый газ, которые приходилось амортизировать первичным магниеплавильным заводам. Эта цепочка передачи издержек заметно ослабила ценовые преимущества предприятий первичного магния, тесно связанных с полукоксовой отраслью.

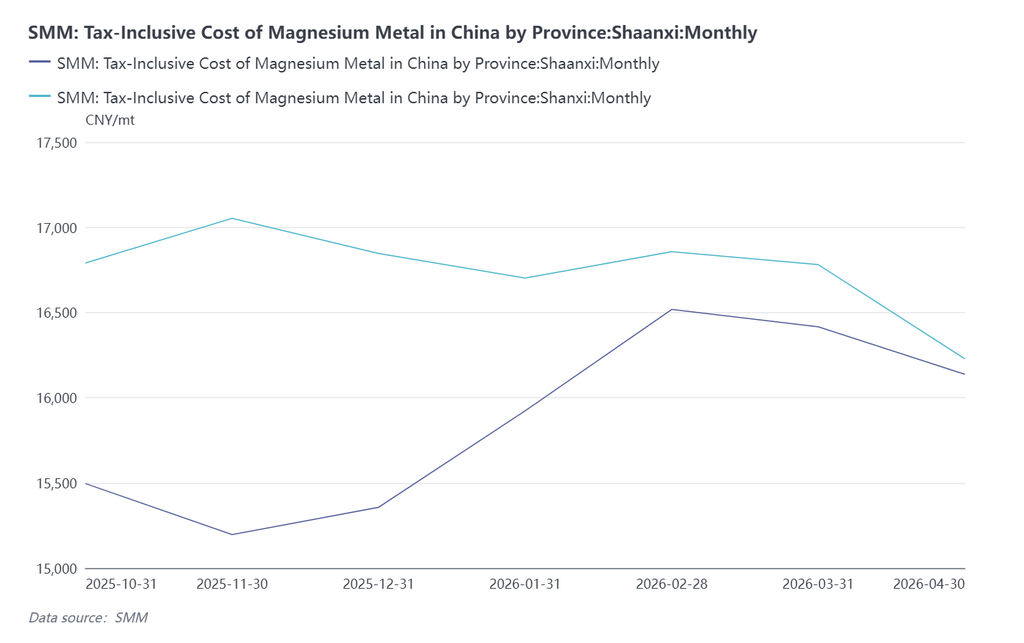

Согласно последним данным SMM по расчёту себестоимости за апрель 2026 года, региональная структура затрат на выплавку первичного магния в Китае претерпела существенную перестройку. Себестоимость выплавки первичного магния в провинции Шэньси, традиционно обладавшей преимуществами энергетической производственной цепочки, продолжала расти, тогда как затраты в провинции Шаньси оставались относительно стабильными. Ценовой спред между двумя регионами значительно сократился, а дифференцированные региональные преимущества по себестоимости на данном этапе нивелировались.

В целом затраты на уголь и коксовый газ стали ключевыми факторами, определяющими цены на первичный магний, рентабельность предприятий и динамику отрасли, а тенденция к росту ценового давления на первичные магниеплавильные заводы сохраняется.