[SMM Analysis] Weak Downstream Consumption Increases Pressure on Ex-China Steel Trading

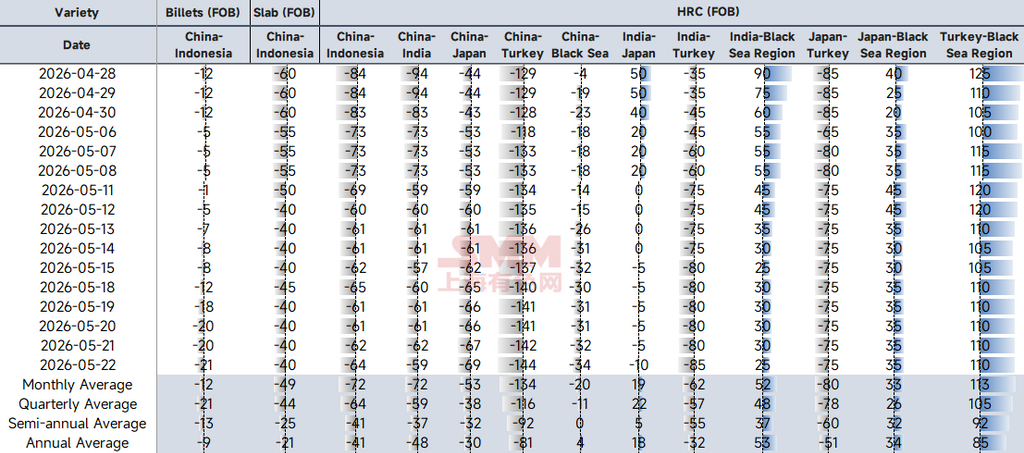

Price spread model, the price inversion of Chinese steel relative to overseas markets (India, Japan, Turkey, Black Sea) deepened further in late May. In particular, Chinese resources were cheaper compared to Indonesia, and the price spread was "narrowing at an accelerating pace." For pure ex-China inter-regional price spreads, India's decline was more pronounced compared to other regions, as weak domestic demand drove aggressive low-price bidding.

Segment-wise, steel procurement sentiment in Southeast Asia became more cautious last week, with coil prices weakening. In Vietnam, coated steel and steel pipe prices began to slow down after a prolonged rally, and buyers became increasingly cautious about restocking ahead of the rainy season. Meanwhile, due to weak demand and growing pressure from low-priced imports, Formosa Ha Tinh Steel, a subsidiary of Taiwan's China Steel Corporation, also cut its HRC quotations by $5-10/mt to $598-603/mt CIF Vietnam. Although some Vietnamese downstream steel mills continued to raise or maintain prices due to earlier increases in raw material costs and tight spot supply, some producers had begun to limit orders or delay quotations while waiting for a clearer market direction. Notably, Indonesian HRC quotations remained competitive with relatively active exports, with FOB prices at around $565/mt. According to SMM survey, recent transaction prices to Vietnam were around $585/mt CFR.

Turkey market: As the Middle East was set to enter a long holiday mid-week, most market participants had already exited early. According to SMM survey, no clear large-volume transactions were seen in the Turkish steel scrap market last week. Meanwhile, as domestic rebar demand remained sluggish, steel mills pushed their target purchase prices for European HMS 1&2 (80:20) scrap below $400/mt CFR to pass on the pressure. The recent euro depreciation and slight correction in ocean freight rates opened up some discount room for European sellers to a certain extent, but judging from actual market transactions, sellers still found it difficult to accept such low prices. At the same time, US exporters continued to hold prices firm at $420/mt CFR. In addition, mainstream quotations for Turkish domestic HRC remained at $660-675/mt EXW. Due to exchange rate fluctuations and high production costs, steel mills were striving to hold prices firm, but downstream buyers remained cautious in purchasing, with expected psychological prices 15-20 $/mt lower.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![[SMM Iron & Steel] US Iron & Steel Scrap Exports Fall 27.1% MoM in April 2026](https://imgqn.smm.cn/usercenter/Zznfn20251217171716.jpg)