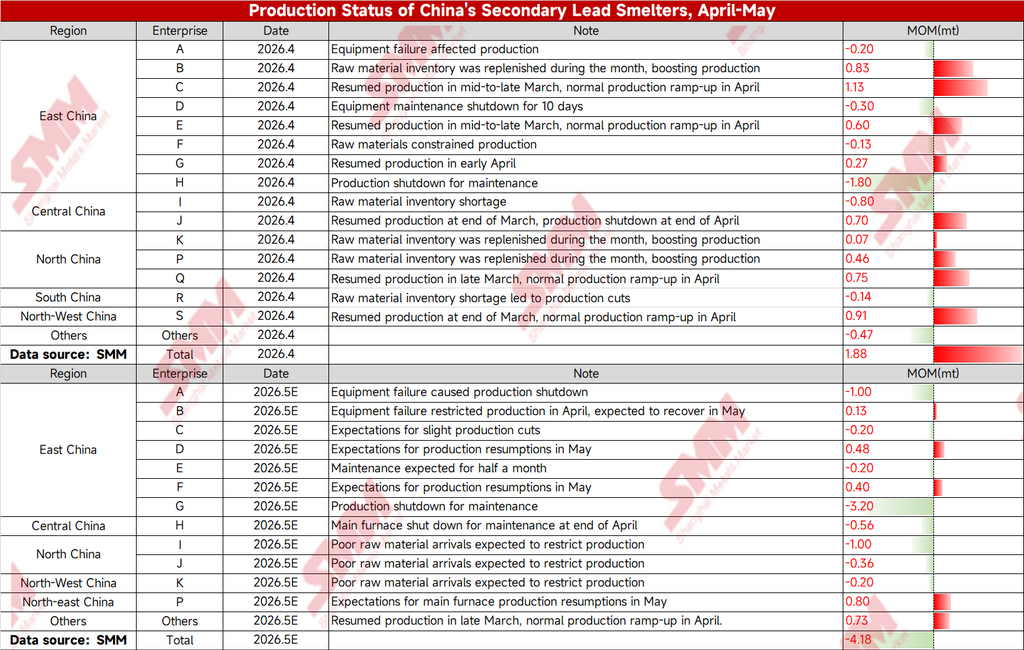

An SMM survey showed that in April, refined lead supply from secondary lead enterprises edged up by 18,800 mt MoM, mainly driven by production resumptions at previously idled enterprises and output increases from raw material restocking. However, entering May, the supply side quickly shifted to contraction, with the combined MoM impact on refined lead reaching -41,800 mt, far exceeding the prior increase.

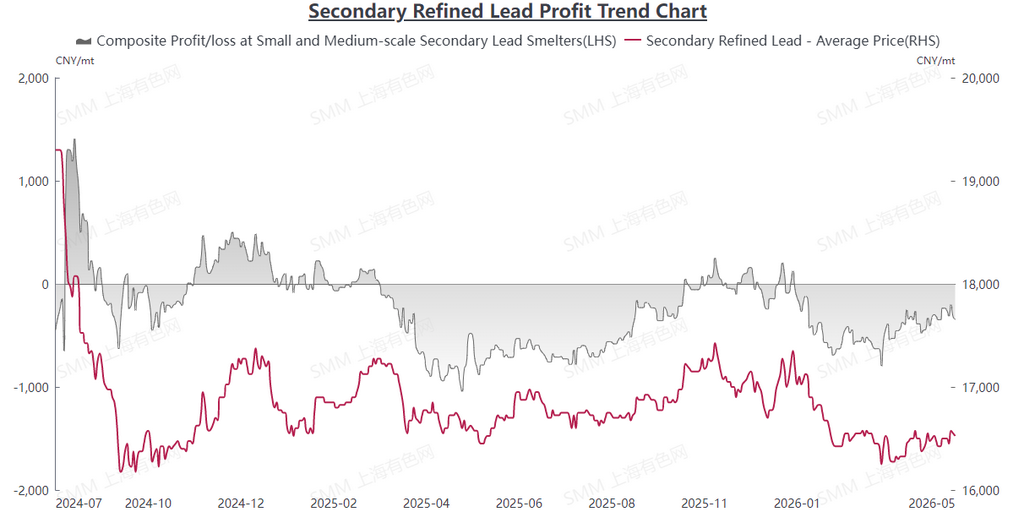

The core driver was sustained pressure on smelter profits: tight scrap battery supply, procurement costs that stayed high, compounded by weak demand during the downstream battery off-season, continuously squeezed smelting margins, and enterprises' willingness to passively cut production rose significantly.

Multiple smelters in east China, central China, and north China suspended production due to equipment maintenance, insufficient raw materials, or losses, while some enterprises' production resumption plans were also delayed as raw material arrivals fell short of expectations. In the short term, cost pressure and raw material bottlenecks are expected to continue constraining secondary lead supply release. Smelter production cuts may persist, and industry profit recovery still awaits improvement on both the raw material and demand sides.

![Lead Prices Fell in Both Overnight and Prompt Markets, Support for Ex-China Lead Prices Remains [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/xVUpr20251217171722.jpg)

![As the Holiday Factor Subsided, Downstream Enterprises Resumed Purchasing Lead Ingots as Needed [SMM Lead Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/xVgcv20251217171721.jpg)