As the "anchor" of the global rare earth permanent magnet supply chain, China's export data is not merely a reflection of trade flows but a barometer of great power competition. Looking back at 2022-2025, the fluctuations in total export volume and the shifts in regional destinations precisely mapped the international political landscape, evolving from "supply chain decoupling" to "export control countermeasures." Standing in the present of 2026, with the geopolitical landscape reshuffling once again, we are ushering in a new cycle of exports.

2022-2025 Export Data Review: From Sprint to Hard Landing

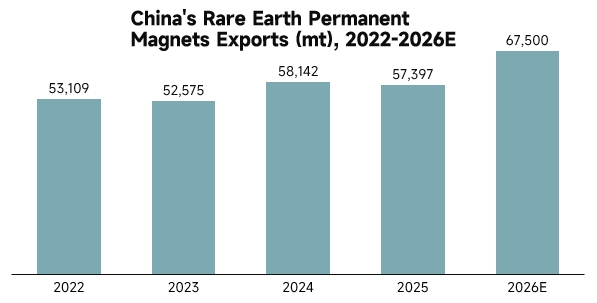

Over the past four years, China's total export volume of rare earth permanent magnets has shown a complex trend of "dipping, rising, and then hitting a policy ceiling."

In 2022, as the global supply chain was still in the post-pandemic recovery phase, total exports remained at a relatively high level of 53,109 tons. Entering 2023, influenced by the European and American "de-risking" strategies, total exports briefly fell to 52,575 tons, yet structural changes had already occurred: Europe, as the vanguard of alternative supply chains, saw imports surge to 26,995 tons, showing a strong willingness to stockpile; meanwhile, US imports remained at 7,308 tons, reflecting the rigid dependence of its high-end manufacturing on Chinese magnetic materials.

2024 was a key turning point. Driven by the integration effect of the China Rare Earth Group and the recovery of overseas demand, total annual exports climbed to a peak of 58,142 tons. Germany, with imports of 9,915 tons, became the core engine of the European market, and US imports also increased to 7,446 tons. However, this prosperity hit a sudden brake in 2025. Affected by China's April export controls on medium and heavy rare earths like Dysprosium and Terbium, total annual exports fell back to 57,397 tons. Notably, imports to the US market plummeted to 5,933 tons, a significant year-on-year contraction, directly reflecting the blocking effect of the export licensing system on trade flows.

The Decisive Role of China-US Relations: From Trade War to Licensing

In the grand narrative of China-US relations, rare earth permanent magnets have long transcended their commodity attributes to become core chips in the tech war and national security. Between 2022 and 2024, despite the US pushing its "Small Yard, High Fence" strategy to reduce reliance on China in sectors like EVs and wind power, the rigid demand for high-performance NdFeB in defense equipment like F-35 fighters and Virginia-class submarines kept US imports on the "lifeline" of 6,000-7,000 tons.

However, the policy shift in 2025 changed this balance. China's implementation of export controls was not a blanket ban but a precise "long-arm jurisdiction." For high-performance magnetic materials with dual civil-military use, the prolonged approval process directly led to a cliff-like drop in US imports. Data shows that the reduction in US imports in 2025 was not due to disappearing demand, but a supply mismatch caused by trade barriers. This "passive reduction due to rising compliance costs" has become the new normal in China-US rare earth trade.

Divergence in the European Market and Germany's "Lone Savior"

Unlike the drastic fluctuations in the US, the European market presents a contradictory unity. In 2023, the surge in overall European imports stemmed from its urgent need to establish an independent green energy supply chain after decoupling from Russian energy. But by 2025, affected by a dual squeeze of macroeconomic weakness and panic over export controls, overall European imports fell back to 20,565 tons.

Notably, the German market walked an independent path. In 2025, German imports bucked the trend, growing to 11,768 tons, accounting for over 57% of the European total. This reflects that as Europe's high-end manufacturing hub, Germany's automotive and precision instrument industries have a far higher dependence on Chinese high-performance magnetic materials than other European nations. Under the EU's slogan of "de-risking," German companies voted with real money, maintaining deep ties with the Chinese supply chain.

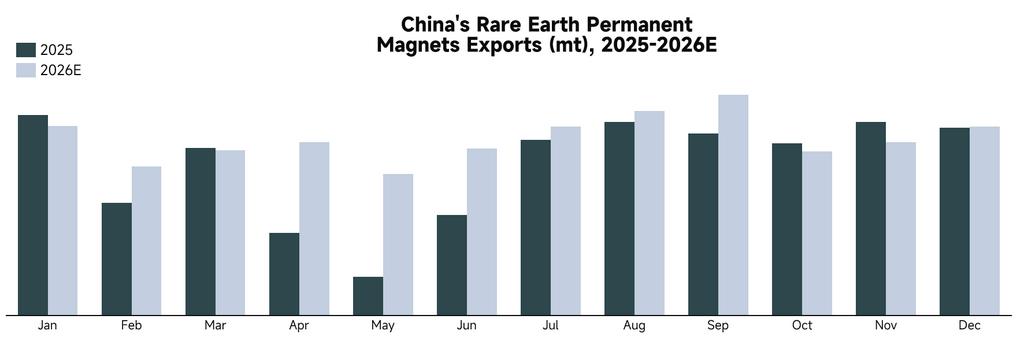

2026 Outlook: V-Shaped Rebound Amid Geopolitical De-escalation

Looking ahead to 2026, we project China's rare earth permanent magnet exports will break through 67,500 tons, ushering in a strong recovery. This forecast is based on three core judgments of the current international political landscape.

First is the tactical de-escalation of China-US relations. As the Trump administration gets bogged down in the US-Iran war, the US urgently needs to avoid direct conflict with China in the East Asian direction to concentrate strategic resources on the Middle East. Meanwhile, the market widely expects Trump to visit China in 2026, and the expectation of high-level interaction will greatly ease trade tensions. To gain China's support on regional security issues, the US side may show greater flexibility in approving rare earth export licenses, and pent-up US restocking demand will be released in a concentrated manner.

Second is the "rebalancing" of global supply chains. After the policy adjustment in 2025, overseas enterprises have largely adapted to China's new export control processes. The diminishing marginal impact of compliance costs is allowing trade flows to return to supply-demand fundamentals.

Finally, rigid demand growth. Whether it's the mass production expectations for humanoid robots or the recovery in global wind power installations, all provide a solid base for 2026 exports. In summary, driven by the dual engines of receding geopolitical risk aversion and recovering rigid demand, 2026 will be a year for China's rare earth permanent magnet exports to return to a fast lane of growth.