SMM April 22:

Metals market:

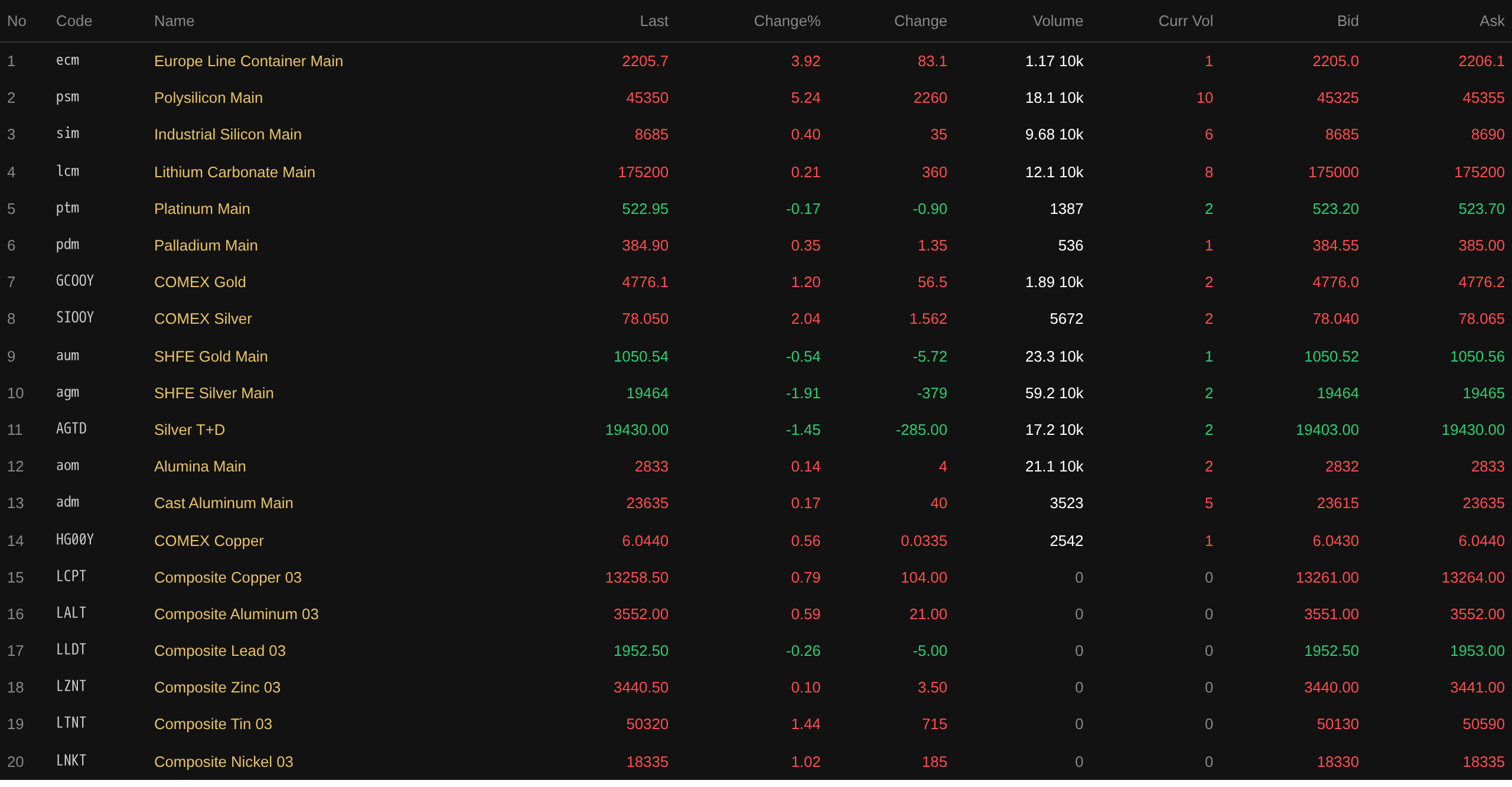

As of the midday close, domestic market base metals mostly rose. SHFE copper was up 0.12%. SHFE aluminum was up 0.26%. SHFE lead was down 0.59%, and SHFE zinc was up 0.23%. SHFE tin was down 0.58%, and SHFE nickel was up 0.79%.

In addition, the most-traded foundry aluminum futures were up 0.17%, and the most-traded alumina contract was up 0.14%. The most-traded lithium carbonate contract was up 0.21%. The most-traded silicon metal contract was up 0.4%. The most-traded polysilicon futures were up 5.24%.

Ferrous metals mostly rose. Iron ore was up 0.64%, rebar and hot-rolled coil were both up less than 0.5%, and stainless steel was down 0.1%. Coking coal and coke: the most-traded coking coal contract was up 1.31%, and the most-traded coke contract was up 1.12%.

Overseas market base metals, as of 11:48, LME metals were nearly all up. LME copper was up 0.79%. LME aluminum was up 0.59%, LME lead was down 0.26%, and LME zinc was up 0.1%. LME tin was up 1.44%. LME nickel was up 1.02%.

Precious metals, as of 11:48, COMEX gold was up 1.2%, and COMEX silver was up 2.04%. Domestic market precious metals: the most-traded SHFE gold contract was down 0.54%, and the most-traded SHFE silver contract was down 1.91%.

In addition, as of the midday close, the most-traded platinum futures were down 0.17%, and the most-traded palladium futures were up 0.35%.

As of the midday close, the most-traded Europe containerized freight index contract was up 3.92%, at 2,205.7 points.

As of 11:48 on April 22, midday futures quotes for selected contracts:

Spot cargo and fundamentals

Zinc:In the Tianjin market, #0 zinc ingot was mainly traded at 23,980-24,120 yuan/mt, Zijin brand at 24,060-24,140 yuan/mt, and #1 zinc ingot at around 23,980-24,060 yuan/mt. Zijin was quoted at a discount of 30-40 yuan/mt against the 2605 contract. Huzinc was quoted at 25,170 yuan/mt. #0 zinc ingot was quoted at a discount of 50-120 yuan/mt against the 2605 contract. Tianjin was quoted at a discount of around 50 yuan/mt against Shanghai.

Macro front

China:

[Ministry of Emergency Management: China's total work safety accidents dropped significantly in Q1]April 22 - According to the Ministry of Emergency Management, China's total work safety accidents dropped significantly in Q1, with the safety situation in most regions and industry sectors improving notably. Shen Zhanli, Director of the Press and Publicity Department of the Ministry of Emergency Management, said that a total of 3,258 work safety accidents of various types occurred nationwide in Q1, down 26.7% YoY. No extraordinarily serious accidents occurred, but major accidents and significant near-miss incidents were frequent in some regions and industry sectors. Illegal production activities in sectors such as mining, chemicals, fire safety, and fireworks showed signs of resurgence. The pressure to prevent and curb major and extraordinarily serious accidents further increased, and the work safety situation remained challenging. Natural disaster side, China's Q1 was dominated by low-temperature freezing rain and snow, snowstorms, wind and hail, and earthquakes, with droughts, floods, forest fires, and geological disasters also occurring to varying degrees. (Xinhua News Agency) (Jin10 Data)

[China Motorcycle Chamber of Commerce: Motorcycle Exports Reached 4.6268 Million Units in Q1]Based on customs data analysis, from January to March 2026, China's motorcycle exports totaled 4.6268 million units, up 13.49% compared to the same period last year, with an export value of $3.014 billion, up 16.93% compared to the same period last year. Latin America was the largest export destination, with exports of 1.4812 million units, down 8.47% YoY, and an export value of $963 million, down 0.99% YoY. Africa saw the largest growth, with exports of 1.753 million units, up 44.95% YoY, and an export value of $949 million, up 48.01% YoY. (Jin10 Data APP)

[PV Patent Pool Expert Advisory Committee Inauguration Ceremony and PV Patent Pool Co-building Seminar Held in Beijing]On April 21, the PV Patent Pool Expert Advisory Committee Inauguration Ceremony and PV Patent Pool Co-building Seminar was held in Beijing. The establishment of the Expert Advisory Committee aimed to provide regulatory supervision and guidance over the construction and operation of China's PV patent pool, promoting its lawful, compliant, and healthy development. After prior solicitation, selection, and review, the first batch of 14 experts were selected, covering fields including intellectual property management, PV technology R&D, legal litigation, and antitrust research. At the event, representatives from enterprises including TrinaSolar Co., Ltd., JA Solar Technology Co., Ltd., and Jinko Solar Holdings Co., Ltd. jointly launched the PV patent pool in the TOPCon battery technology field. (National Industrial Information Security Development Research Center)

[PBOC Net Injected 5.5 Billion Yuan via Reverse Repo Operations]The PBOC conducted 6 billion yuan of 7-day reverse repo operations today. As 500 million yuan of 7-day reverse repos matured today, a net injection of 5.5 billion yuan was achieved. (Jin10 Data APP)

US dollar side:

As of 11:48, the US dollar index was up 0.01% at 98.4. Fed Chairman nominee Kevin Warsh rebutted Democrats' concerns that he would become the President's "puppet," repeatedly emphasizing that he would be an independent decision-maker if his nomination was confirmed by the Senate. Warsh stated at the Senate Banking Committee hearing on Tuesday that a series of reforms should be made to how the US Fed makes decisions, including establishing a new inflation response framework and improving communication with the public. But he provided few details and dodged questions about the near-term path of short-term interest rates. (Wallstreetcn)

According to CME "FedWatch": the probability of the US Fed raising interest rates by 25 basis points in April was 0%, and the probability of keeping rates unchanged was 100%. The probability of a cumulative 25-basis-point interest rate cut by the US Fed through June was 1.7%, and the probability of keeping rates unchanged was 98.3%. (Jin10 Data)

A CITIC Securities research report stated that Warsh's testimony demonstrated the highly difficult balancing act he faces. On one hand, he needs to "please" Trump to a certain extent, thus acknowledging Trump's right to voice opinions on interest rates; on the other hand, he needs to earn the trust of the market and the US Fed internally, thus emphasizing the mission of price stability and the independence of the US Fed. Although Warsh's performance was unsatisfactory when facing questions from Democratic senators, this has a relatively small impact on whether Warsh can succeed Powell. Whether Warsh can successfully pass the Senate Banking Committee vote depends on whether he can secure the support of Republican Senator Tillis. We believe Trump will most likely TACO and withdraw the investigation into Powell to help Warsh pass the Senate vote. Warsh emphasized during the Q&A session that he would not become Trump's "puppet," and the market leaned toward hawkish trading. Warsh's ideas on reforming the US Fed deserve more market attention, especially his proposal that the US Fed needs a new inflation framework and his criticism of the US Fed's current approach to forward guidance. Warsh emphasized that the US Fed should shrink its balance sheet, with interest rates as the primary policy tool. However, we still believe Warsh's plan to shrink the balance sheet requires lengthy preparation, and the pace of implementation will be gradual.

A CICC research report stated that Fed Chairman nominee Kevin Warsh attended the Senate Banking Committee hearing, revealing his core policy stance of a dual-track approach of "balance sheet reduction and interest rate cuts": at the balance sheet level, he explicitly opposed normalizing quantitative easing (QE), advocating for a gradual and orderly reduction of the US Fed's balance sheet size, exiting quasi-fiscal functions, and returning it to its monetary policy mandate; at the interest rate level, although he made no explicit commitment, his statements already showed an inclination toward cutting interest rates. In our view, Warsh's policy stance is not only an adjustment to the monetary transmission mechanism but also an extension of the "America First" strategy into the monetary domain amid the wave of deglobalization — shifting from a "global central bank" that endlessly supplies liquidity to the world, toward a new approach that firmly controls the monetary spigot, focuses on domestic productivity, and emphasizes monetary sovereignty. We believe this shift means the narrative of persistently excessive US dollar liquidity will face correction, and assets that purely rely on liquidity-driven gains and benefit from "US dollar over-issuance" may come under pressure. (Jin10 Data)

Other currencies:

Japan's March imports and exports continued to grow, but the trade outlook for the coming months remains clouded by the Middle East war. Yasuhisa Irie, an economist at Mizuho Securities, said that in the short term, Japan's total import value is likely to remain roughly flat, as supply constraints suppressed imports and high energy prices eroded consumer confidence, thereby limiting demand. Takeshi Minami, an economist at Norinchukin Research Institute, expected the consequences of energy shortages to become more apparent starting in April. Minami said: "Although the Japanese government has begun to release crude oil reserves and claims to have secured alternative procurement routes that do not rely on the Strait of Hormuz, a prolonged blockade could lead to significant economic contraction in emerging markets with smaller oil reserves." He added that this situation is expected to harm the Japanese economy in multiple ways, including a slowdown in economic activity and intensified inflationary pressures. (Jin10 Data)

Data:

The preliminary eurozone consumer confidence index for April, the UK March CPI monthly rate, and the UK March retail price index monthly rate will be released today. In addition, US Fed Governor Waller will deliver a speech at the Brookings Institution.

Crude oil:

As of 11:48, oil prices in both markets edged down, with WTI falling 0.22% and Brent falling 0.07%. Oil prices moved sideways as the market weighed the prospects of US-Iran peace negotiations.

Data released by the American Petroleum Institute (API) showed that US crude oil inventory declined. For the week ending April 17, API crude oil inventory was -4.47 million barrels (expectations: -1.8 million barrels, previous: 6.101 million barrels). For the same week, API gasoline inventory was -5.165 million barrels (expectations: -1.333 million barrels, previous: 626,000 barrels). (Jin10 Data)

Mitsubishi UFJ analyst Lloyd Chan said in a research note that the US-Iran conflict appeared to have shifted into a prolonged stalemate rather than a swift resolution. The senior currency analyst said the US appeared to be using a blockade of Iranian ports to pressure Tehran into a peace deal, or risk further military escalation. Chan said: "For markets, this environment means continued disruption to energy shipments through the Strait of Hormuz." The analyst added that pressure points were more evident in oil-sensitive currencies, including the Philippine peso and the Thai baht. (Jin10 Data)

A research report from CITIC Securities noted that the recurring tensions in the Strait of Hormuz indicated that the impact of this round of events on the oil shipping market was still unfolding according to a three-phase logic. After a brief reopening on April 17, Iran reimposed the blockade on April 18, indicating that the situation had not yet stabilized. Regardless of how the U.S.-Iran standoff develops going forward, the market is still in the process of the Hormuz blockade shock gradually transmitting to oil shipping fundamentals. Oil shipping freight rates evolved in three stages: rates rose during the conflict period, vessel redeployment lengthened shipping distances and pushed up the freight rate center, and after the reopening, a rush to secure oil may drive freight rates higher for over two months. Currently, the third stage — the inevitable global scramble for crude oil following the reopening of the Strait of Hormuz — will inevitably transmit to the oil tanker shipping market. (Jin10 Data)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

![Inventory Hit a New Annual Low as Suppliers Actively Held Prices Firm, Overall Trading Atmosphere Better Than Yesterday [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/FERSF20251217171712.jpg)

![Extension of Ceasefire Deadline Flattened Macro Sentiment, Tin Prices Continued Volatile Pattern [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/GgYmu20251217171750.jpg)

![Cross-Regional Arbitrage Window Continued to Widen, Tight Cargoes with Invoices Dated This Month Expected to Support Spot Premiums [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/vcsIC20251217171710.jpg)