Recently, affected by Indonesia's nickel ore quota and HPM benchmark price adjustments, the production cost of high-grade NPI has seen a rigid increase. Combined with supply-side increments falling short of expectations and continued inventory destocking, market prices have fluctuated upward. Meanwhile, weak buying interest from downstream steel mills and the sustained substitution advantage of steel scrap have limited the upside room for high-grade NPI prices, presenting an overall pattern of "support below, pressure above." The following is SMM's detailed analysis:

Cost Side: New HPM Policy + Tax Increase Significantly Strengthened Cost Support

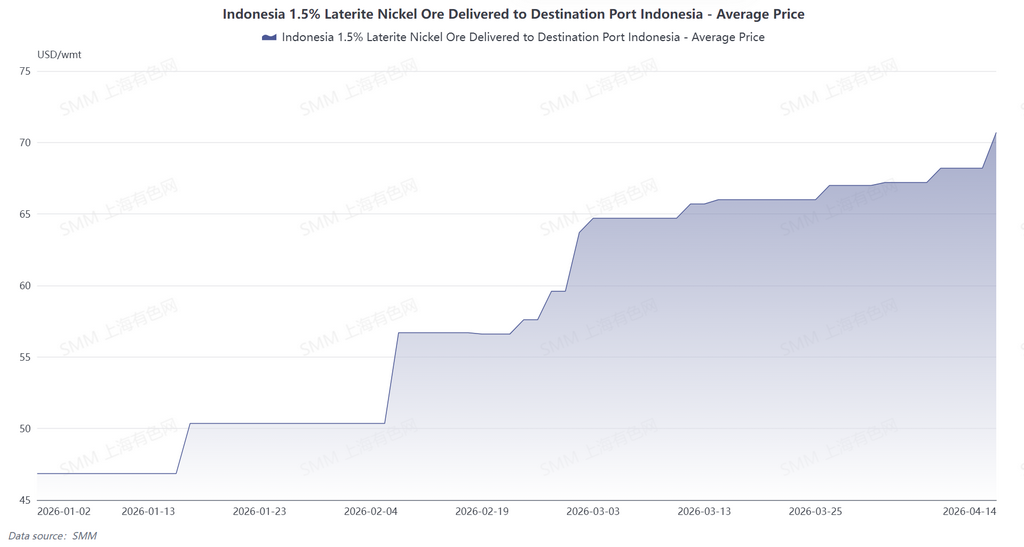

As Indonesia's new HPM benchmark price is about to take effect, according to SMM's calculations based on the benchmark price as of April 1, taking 1.5% grade nickel ore prices as an example: under the old formula, the HPM price for nickel ore was $26.66/wmt, while under the new formula, the HPM price for nickel ore was $57.13/wmt. Assuming the tax costs arising from the HPM price increase are fully passed through to downstream, the absolute price of nickel ore is expected to rise to approximately $72.47/wmt after the new policy is implemented. Based on this calculation, the adjustment will push the full cost of NPI up to $15,741.51/mt Ni, an increase of $570.48/mt Ni from the current level, representing a rise of approximately 3.76%, which is expected to provide further upward support for NPI prices.

Spot Quotations: Spot Quotations Rose, but Weak Downstream Buying Constrained the Increase

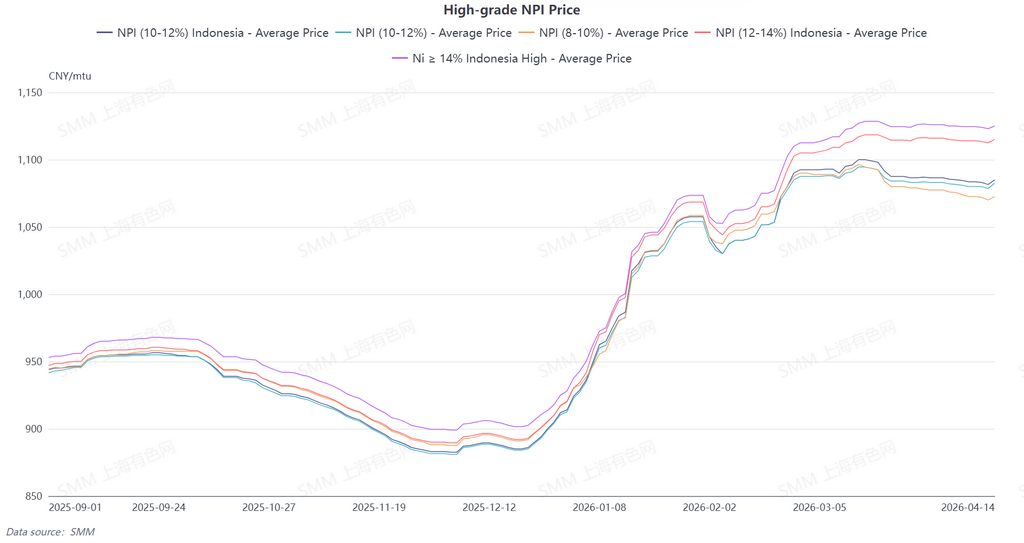

Driven by rising costs, higher nickel ore prices, and nickel futures gains, NPI producers' willingness to hold prices firm strengthened notably, and the market quotation center shifted upward again.

After the sharp rally in nickel prices, NPI traders' purchase quotations were concentrated at 1,080–1,090 yuan/nickel unit, up from the previous period but with limited gains. The main reason was that although the futures-spot arbitrage window opened and traders showed greater enthusiasm in inquiring, downstream stainless steel mills' buying interest remained persistently weak, and traders were generally concerned about difficulties in spot shipments after arbitrage. Although arbitrage opportunities exist on the futures side, actual shipments to steel mills require discounts for quick transactions, making the arbitrage appeal insufficient and providing limited actual support for spot prices.

From the steel mill perspective, most steel mills' purchase target prices remained flat, with quotations still running below 1,080 yuan/nickel unit.

Supply and demand: Supply growth falls short of expectations, inventory drawdown confirms tight pattern

On the supply side, affected by maintenance-related production cuts at some NPI projects and Indonesia's nickel ore mining quota controls, NPI supply growth has fallen short of expectations. On the demand side, steel mill planned production remains elevated, rigid demand for raw material procurement is not weak, and although it is difficult to find fixed-price deals in the market, a large volume of transactions are being concluded at average prices.

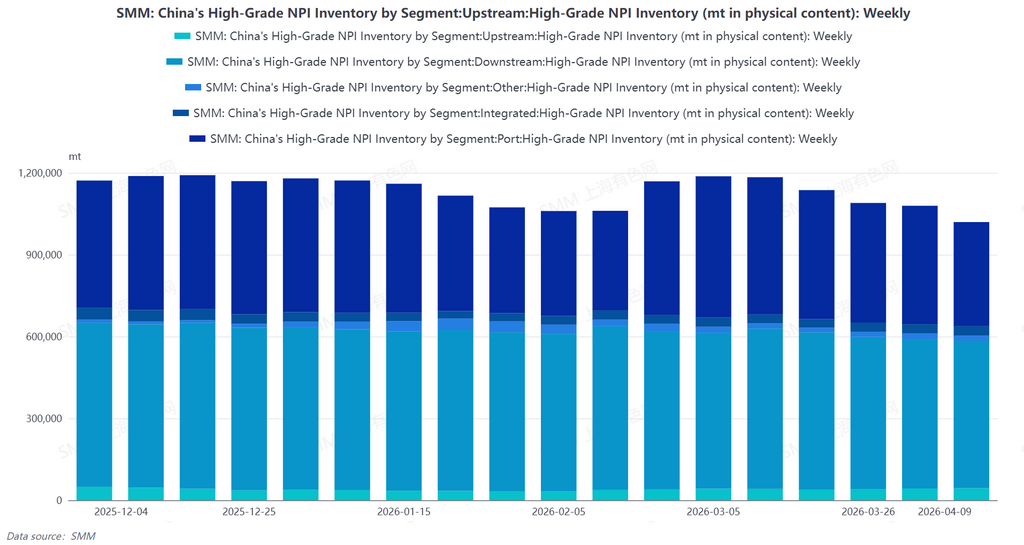

Inventory data further confirms the tight supply-demand situation: the latest weekly high-grade NPI inventory data shows that China's port NPI inventory drew down by 52,600 mt last week, with cumulative overall inventory declining by 59,700 mt. The current supply-demand pattern is tight, and the market is particularly short of high nickel unit spot cargoes.

Market outlook: Prices to test higher in the short term, but upside is constrained

In the short term, cost support and tight supply and demand will drive NPI prices to rebound and rise, and the price center for high-grade NPI is expected to continue shifting upward this month.

However, upward price movement still faces three layers of pressure:

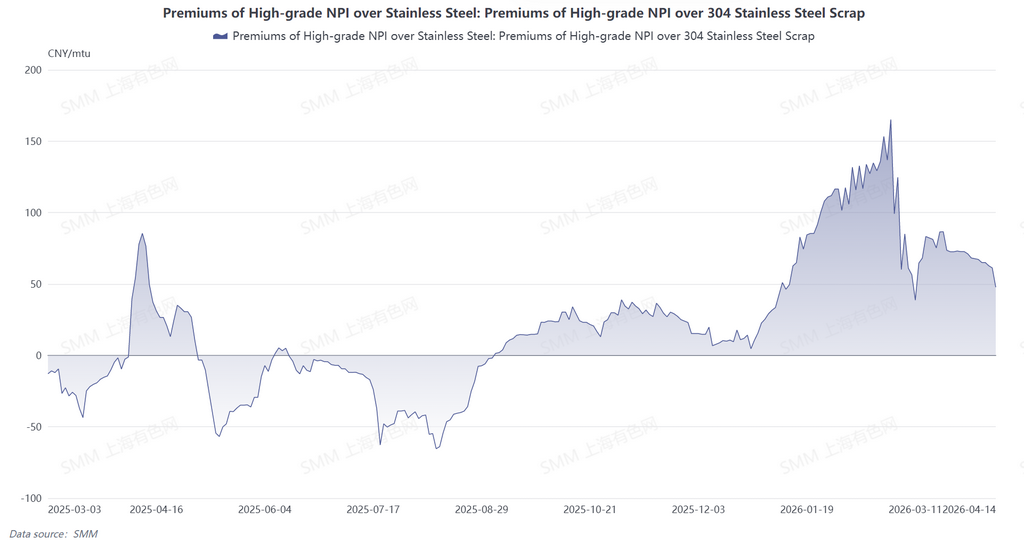

First, steel scrap substitution is capping prices. Steel scrap prices currently maintain a significant cost advantage. Following the release of the reverse-invoicing whitelist, combined with considerable economic advantages, the share of steel scrap usage at steel mills has continued to rise, keeping steel mills' psychological price level below 1,080 yuan/nickel unit, unadjusted in line with rising NPI costs.

Second, end-use demand pressure. Although stainless steel futures have also been lifted, and steel mill profits have improved somewhat, end-user procurement remains cautious throughout, and stainless steel spot prices are running steadily, making it difficult to form end-use demand support for NPI.

Third, concerns over arbitrage-driven selling. With the arbitrage window open and traders actively purchasing, the market simultaneously faces concerns over arbitrage-driven selling pressure. Wild swings in nickel prices may make it difficult to sustain upward momentum.

In summary, the tug-of-war between upstream and downstream in the current NPI market continues, and expectations of losses at NPI producers are becoming prominent. Although the cost support brought by the new HPM policy is strong, the drag from end-user demand and steel scrap substitution cannot be ignored. In the short term, high-grade NPI prices are expected to rise gradually amid the tug-of-war between upstream and downstream.

![[SMM Stainless Steel Flash] Major China CR Stainless Producer Sees Profit Drop in 2025, Sets Higher 2026 Targets](https://imgqn.smm.cn/usercenter/VstiG20251217171732.jpeg)

![[SMM Stainless Steel Flash] Major Indonesian Stainless Mill Suspends Offers After New HPM Formula Revision](https://imgqn.smm.cn/usercenter/PuSOO20251217171732.jpeg)