По данным агентства Синьхуа, по мере эскалации конфликта между США и Ираном Корпус стражей исламской революции Ирана объявил о закрытии Ормузского пролива вечером 28 февраля. Многие владельцы танкеров и трейдеры приостановили перевозки через пролив. Это первый случай за последние годы, когда основной глобальный канал транспортировки энергоносителей и химикатов столкнулся с фактической приостановкой работы. Будучи «горлом» для мировой торговли серой, этот сбой непосредственно перекроет экспортные каналы серы на Ближнем Востоке и создаст цепную реакцию, повлиявшую на производство МНП в Индонезии и на индустрию фосфатных удобрений в Китае, которые в значительной степени зависят от ближневосточных источников.

I. Ормузский пролив: «Канал жизненной важности» для экспорта серы с Ближнего Востока перекрыт, пропускная способность альтернативных маршрутов ограничена

Ормузский пролив является абсолютно основным путем для мировой торговли серой, и его закрытие окажет «магнитудное» воздействие на экспорт серы с Ближнего Востока.

1. Мировая торговля серой в значительной степени зависит от этого пути

В мировой морской торговле серой 50% грузов (около 20 млн тонн в год) поступает из региона Персидского залива на Ближнем Востоке и должно пройти через Ормузский пролив для достижения мировых рынков. К основным экспортирующим странам относятся Саудовская Аравия, ОАЭ, Катар, Кувейт и Иран.

2. Блокированы все основные экспортные порты

Основные порты экспорта серы на Ближнем Востоке — Рувайс в ОАЭ, Джубайль и Рас-эль-Хайр в Саудовской Аравии, Рас-Лаффан в Катаре, Эль-Зур и Шуайба в Кувейте и Бандар-Имам-Хомейни в Иране — все должны транспортировать свою серу через Персидский залив, а затем через Ормузский пролив в Индийский океан. Закрытие пролива означает, что сера из этих портов не может быть погружена и экспортирована.

3. Пропускная способность альтернативных маршрутов крайне ограничена

Хотя существуют варианты обхода Ормузского пролива, их сложно использовать в больших масштабах:

Порт Фуджейра, ОАЭ: расположен за пределами пролива в Оманском заливе, но далеко от основных производственных районов в Персидском заливе, с высокими затратами на наземные перевозки и ограниченной пропускной способностью, а также сложностями в приоритизации навалочной серы во время кризисов.

Порты Красного моря Саудовской Аравии: серу можно перевозить по суше в порт Янбу, но дальняя наземная транспортировка сталкивается с серьезными экономическими и операционными проблемами.

II. Индонезийский MHP: сера из Ближнего Востока как основной источник вспомогательных материалов, нарушение логистики напрямую увеличит производственные затраты

Как ключевой производственный центр для глобальных материалов нового энергетического никеля-кобальта (MHP), индонезийские проекты HPAL сильно зависят от серы из Ближнего Востока. Это нарушение напрямую повлияет на производственные затраты и стабильность поставок MHP.

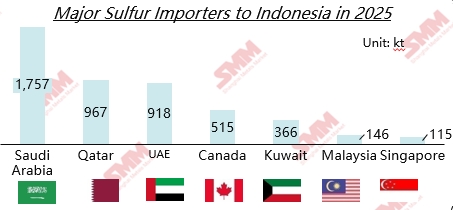

1. Высокая концентрация импорта серы в Индонезии

Согласно данным таможни Индонезии, более 75% импорта серы в Индонезию в 2025 году пришлось на Ближний Восток. Эта высококонцентрированная структура поставок означает, что после закрытия Ормузского пролива основной источник сырья для индонезийских проектов MHP будет точно перекрыт.

2. Жесткий спрос на производство MHP

На основе средних показателей отрасли, для производства 1 тонны MHP требуется около 11,7 тонн серы. Несмотря на недавние оползни в индонезийском промышленном парке, которые нарушили некоторые проекты, приведя к работе на низкой нагрузке и неопределенности спроса со стороны потребителей, другие существующие и новые проекты MHP все еще имеют значительный жесткий спрос на серу.

3. Усиление механизма передачи затрат

Прямое влияние на затраты: По оценкам SMM, к январю 2026 года сера составляла 41% затрат на производство MHP. Если цены на серу продолжат расти из-за нарушений поставок, стоимость серы в MHP также возрастет, сжимая маржу прибыли проектов.

Растущие закупочные затраты: Индонезийским покупателям придется конкурировать с мировыми покупателями за ограниченные поставки, не связанные с Ближним Востоком. Кроме того, рост страховых премий и увеличение стоимости фрахта из-за обходных маршрутов еще больше повысят стоимость доставки.

III. Расширение ценового воздействия: ускоренное истощение запасов серы в Китае еще больше повысит цены

Как крупнейший в мире импортер серы, Китай имеет структурную зависимость от источников Ближнего Востока. Это нарушение напрямую повлияет на внутреннее предложение серы и производство фосфатных удобрений, что еще больше повысит цены на серу.

1. Чрезвычайно высокая зависимость от импорта

Внешняя зависимость Китая от серы долгое время оставалась на уровне 50-53%. Таможенные данные показывают, что в 2025 году Ближний Восток составил 56,2% импорта серы в Китай, что означает, что более половины логистики импортной серы будет затронуто.

2. Жесткий спрос на подготовку удобрений к весне

В настоящее время это критический период для подготовки удобрений к весне, когда существует жесткий спрос на серу для производства фосфатных удобрений. Предприятия по производству диаммонийфосфата поддерживают высокие уровни работы, с выпуском потребностей в пополнении запасов, и аукционы обычно заканчиваются премиальными ценами, что указывает на сильное намерение трейдеров удерживать цены.

3. Ускоренное истощение запасов, ограниченные альтернативные поставки

Финансовые данные iFinD показывают, что по состоянию на 28 февраля, общий портовый запас серы в Китае составлял 1,7398 миллиона тонн. При среднем ежемесячном потреблении 1,4-1,5 миллиона тонн во время весеннего пахотного сезона, текущие запасы могут поддерживать работу только на 1,2-1,5 месяца. С учетом заводских запасов и товаров в пути, время поддержки увеличивается до 1,5-2 месяцев. Если блокада пролива продолжится, запасы будут быстро истощаться в пиковый период весеннего пахотного сезона в марте-апреле. Хотя Китай может искать альтернативные источники в Северной Америке, Черном море и Центральной Азии, большие расстояния перевозки, высокие транспортные расходы и ограничения контрактов ограничат скорость пополнения запасов.

IV. Предупреждения о рисках для нижнего звена

1. Материалы для аккумуляторов электромобилей:Как основной исходный материал для предшественников катодов, увеличение стоимости MHP будет передаваться по цепочке отрасли к материалам катода и элементам батарей, в конечном итоге влияя на затраты на производство электромобилей.

2. Фосфатные удобрения: 56% импорта серы в Китай сталкиваются с риском перебоев в поставках. Внутренние портовые запасы будут быстро истощаться в пиковый период подготовки к весеннему сельскохозяйственному сезону, ожидается, что цены на серу превысят предыдущие максимумы и передадутся ценам на фосфатные удобрения, в конечном итоге повышая затраты на сельскохозяйственное производство.

3. Продолжительность является ключевой переменной:

Если остановка будет краткосрочной (1-2 месяца): влияние будет сосредоточено главным образом на колебаниях цен, с которыми предприятия могут справиться путем корректировки запасов и замены сырья.

Если остановка производства длительная (более 3 месяцев): это приведет к непрерывному расширению дефицита предложения. Некоторые предприятия, зависящие от долгосрочных соглашений с Ближним Востоком, могут столкнуться с нехваткой сырья, снижением загрузки мощностей или даже остановкой производства. Глобальные цепочки поставок серы и смежные отрасли пройдут через глубокую реструктуризацию.

![[SMM Обзор рынка никеля за полдень] 23 июня цены на никель резко упали, индекс доллара США пробил отметку 100.](https://imgqn.smm.cn/usercenter/sKmGT20251217171733.jpg)