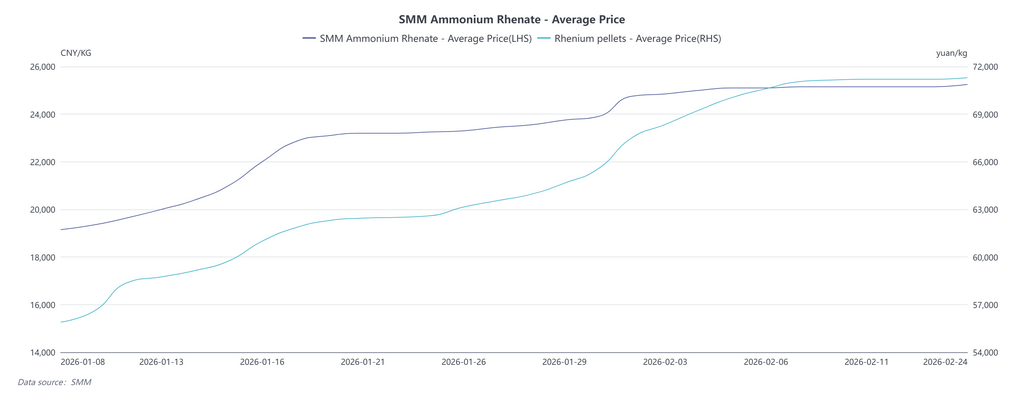

Following the Spring Festival holiday, SMM research indicates that some raw material manufacturers have quoted prices in the range of 27,000-28,000, with a reluctance to sell. Meanwhile, metal-side manufacturers intend to adjust prices but have shown low willingness to purchase raw materials at high prices, due to the impact of downstream market sentiment.

The downstream metal market has seen active inquiries but sluggish actual transactions. Major metal manufacturers have refrained from adjusting prices temporarily after the holiday, partly because some manufacturers have not yet resumed operations. Additionally, amid relatively high raw material prices, some manufacturers have increased their proportion of scrap procurement. Although downstream buyers are willing to enter the market, they remain on the sidelines waiting for price declines and have not yet made actual purchases.

In terms of market sentiment, a strong wait-and-see attitude prevails, and some metal manufacturers are caught in a dilemma. On one hand, these manufacturers are reluctant to sell and have no intention of large-volume shipments, leading to their willingness to raise prices. However, they face multiple concerns: excessive price hikes would trigger a corresponding increase in ammonium rhenate raw material prices, pushing up their subsequent procurement costs; maintaining current prices, on the other hand, would squeeze profit margins due to rising raw material costs. On the other hand, the current rhenium price environment has already resulted in a downstream market characterized by active inquiries but weak transactions, and excessive price increases would likely further dampen downstream procurement willingness. This dilemma in price adjustment decisions has further underpinned the overall stability of the current rhenium market.

![[SMM Analysis] Indonesian Nickel Ore Drives Futures Higher, Stainless Steel Inventory Continues Mild Destocking](https://imgqn.smm.cn/usercenter/TdoSs20251217171724.jpeg)