01Basic introduction of the company and its industry status

Profile

Fortescue Metals Group Ltd. FMG was founded in 2003 by Australian Andrew Forrest through the acquisition and renaming of ASX-listed Allied Mining & Processing. FMG is a global leader in the iron ore industry, boasting a unique corporate culture and technological innovation. It has developed world-class infrastructure and mining assets in the Pilbara region of Western Australia, a prime iron ore producing region. It is Australia's third-largest iron ore producer and the fourth-largest globally , after Rio Tinto and BHP Billiton . Compared to the diversified portfolios of Rio Tinto, BHP Billiton, and Vale, FMG focuses exclusively on iron ore .

Business

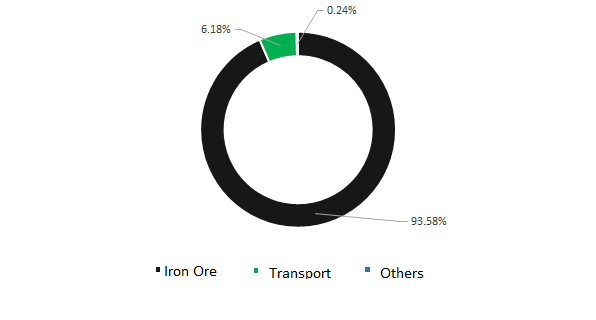

According to Fortescue Metals Group's financial reports, China accounts for 89.7% of Fortescue's overall revenue. Over 90% of its iron ore is shipped to China. In its early years, between 2004 and 2006, Fortescue Metals Group signed long-term supply agreements with numerous Chinese steelmakers, including Hebei Wenfeng Steel Co. , Ltd. , Jiangsu Fengli Group , and Jiangxi Pingxiang Steel Co., Ltd. These supply contracts earned Fortescue the trust of the capital market, leading to a surge in its stock price. Furthermore, through continuous financing through various channels, Fortescue Metals Group accumulated substantial funds for iron ore exploration and development. On May 15, 2008, Fortescue Metals Group dispatched its first commercial shipment of iron ore to Shanghai Baosteel's Majishan Port. The 2008 financial crisis plunged Fortescue Metals Group, which had previously heavily indebted, into a difficult situation, prompting the company to seek investor capital. Fortescue Metals Group set its sights on Hunan Valin Steel Group Co., Ltd. (hereinafter referred to as "Valin Group") in China. In 2009, Valin Group acquired a total of 535 million shares at an average price of AUD 2.38 per share through a private placement, acquiring a 17.34% stake and becoming the second largest shareholder of Fortescue. Valin Group invested in Fortescue during the depths of the financial crisis. As the world economy gradually stabilized, Fortescue's production and operations also steadily increased, and the financial crisis was resolved.

Main income components of Fortescue Group (US$ billion)

Data source : FMG financial report SMM

02 Iron ore production, shipments and main products

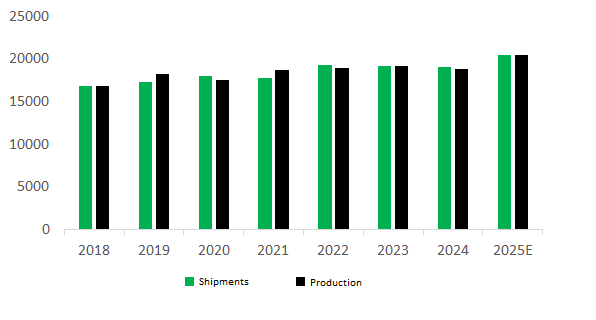

In 2004, Fortescue Metals Group (FMG) discovered iron ore reserves in the Cloudbreak mining area in Western Australia's Pilbara region. The company subsequently proposed a AUD 1.85 billion investment plan, projecting an annual production of 45 million tons of iron ore. Construction began at Port Hedland in February 2006, followed by full-scale development of the port, railway, and mine. In just two years, Fortescue Metals Group completed the railway infrastructure, opened the Fortescue Herb Elliott Port, and commenced mining at its first mine, Cloudbreak. On May 15, 2008, Fortescue Metals Group shipped its first iron ore cargo to Shanghai Baosteel's Maggie Hill Port. Production and shipments have been on the rise in recent years, with a target shipment of 195-205 million tons for fiscal year 2026.

Iron ore production and shipments over the years

Data source : FMG financial report SMM

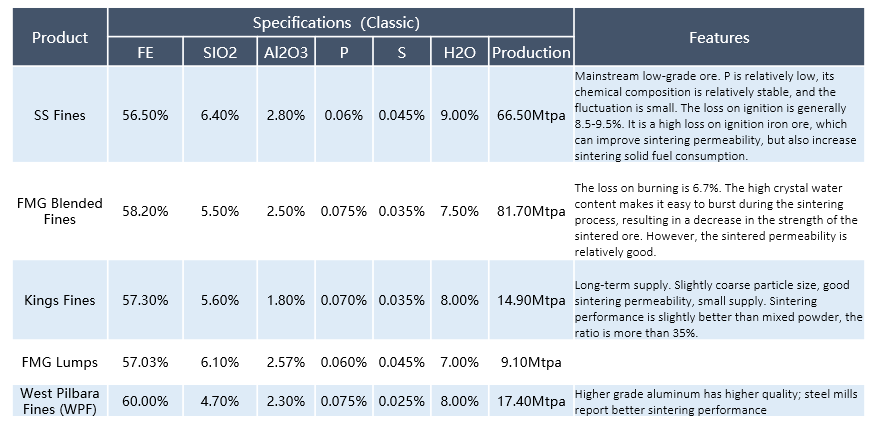

Products

03 Situation of the Group’s Mines

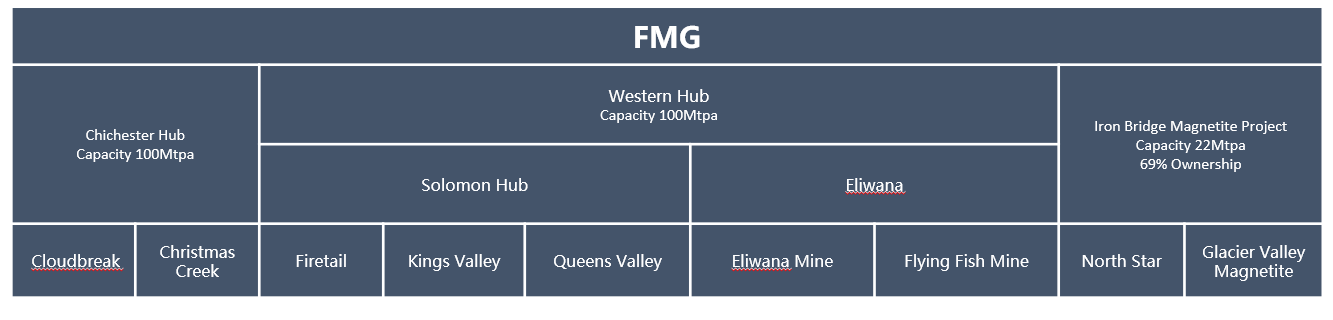

1. Chichester Hub, including the Cloudbreak and Christmas Creek mines and three ore processing facilities (OPFs), with an annual production capacity of 100 million tonnes.

2. The Western Hub, comprising two mines, Solomon and Eliwana, is located near the Hamersley Ranges, 60 kilometers north of Tom Price and 120 kilometers west of the Chichester Hub. The Solomon mine began operations in 2012, while the Eliwana mine (140 kilometers west of the Solomon mine) began production in December 2020. With its innovative low-profile Ore Handling Facility (OPF) and dual stackers and reclaimers, the Eliwana mine has a direct loading capacity of up to 9,000 tons per hour. The Western Hub has an annual production capacity of 100 million tons.

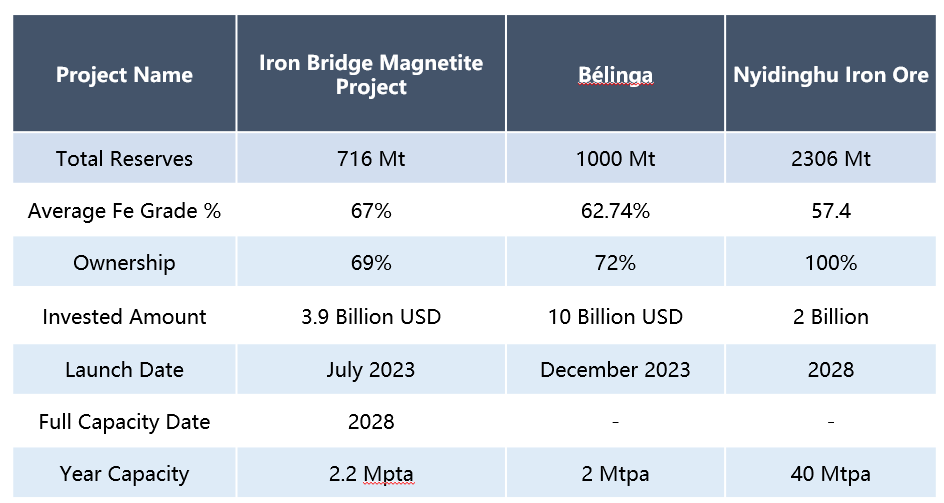

3. Iron Bridge Magnetite Project: The Iron Bridge Project, located 145 kilometers south of Port Hedland, integrates the world-class North Star and Glacier Valley magnetite ore bodies. It is an unincorporated joint venture between FMG Magnetite Pty Ltd (69%) and Formosa Steel IB Pty Ltd (31%). Each party is responsible for its equity share of total capital expenditure. The project was approved in September 2020, with a commercial assessment completed in May 2021. The first shipment of approximately 200,000 tons will be in September 2023, with production expected to reach 13 million tons/year in 2024 and 22 million tons/year in 2028.

04Future Expansion Project

new project is to achieve further expansion on the basis of stable production

FMG's recent production increase plans include the Iron Bridge Magnetite Project, the Galen Belinga Iron Ore Project and the Nitinghu Project.

Currently, the Tieqiao project has been put into production since May 2023. The first batch of shipments will be about 200,000 tons in September 2023. The production volume in 2024 will be 13 million tons and the shipment volume will be 12 million tons. It is expected to reach a production capacity of 22 million tons/year in 2028.

The Belinga Iron Ore Project, located in Gabon , is Fortescue Metals Group's first iron ore project outside of Australia, acquired through its joint venture subsidiary. Its goal is to achieve stable production while also pursuing further expansion. On December 4, 2023, the first shipment of iron ore from the Belinga Iron Ore Project was successfully loaded and shipped. Currently, the Belinga mine is still in the early stages of trial operations and has not yet officially commenced full-scale production. Fortescue Metals Group is conducting extensive drilling activities to gradually unlock the Belinga project's production potential.

Nyidinghu , being developed by Chichester Metals, a subsidiary of Fortescue Metals, covers approximately 92,301 hectares and is valued at approximately US$2 billion (A$3.1 billion). The mine is planned to produce approximately 40 million tonnes of iron ore annually over 26 years, with first ore expected in 2028.

05 Green Transformation Plan

Fortescue Metals Group plans to invest $6.2 billion by 2030 to achieve green transformation and carbon neutrality across all iron ore operations

Key investment and construction projects include:

1. The Green Metals Project , located at the Christmas Creek Mine, is a collaboration with China Baowu Steel Group to advance hydrogen-based direct reduced iron (DRI) technology. With a total investment of US$50 million, the plant will have an annual production capacity of over 1,500 tonnes of green metal , with first production expected in the fourth quarter of 2025.

2. Electric Iron Ore Train (Infinity Train) : In partnership with Williams Advanced Engineering (WAE), the company is developing the world's first zero-emission electric iron ore train, called the Infinity Train, which uses downhill gravity energy recovery to recharge its batteries. The train is expected to be operational by 2026. This train is self-sufficient in its electricity cycle, requiring no external charger.

3. The Pilbara Energy Connect project integrates the Pilbara region's fixed energy needs into an efficient network. The project includes the construction of 100 MW and 190 MW solar farms at North Star and Cloudbreak, respectively, along with 500 km of transmission lines and associated substations. The North Star solar farm is expected to be completed in 2024, while the Cloudbreak solar farm is expected to be completed in the second half of 2026.

![In the short term, ferrous metals will remain under pressure [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/YxksS20251217171748.jpg)

![Silicon Metal Futures Fluctuate within a Narrow Range, Spot Market Largely Stable [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/bkAyC20251217171720.jpg)