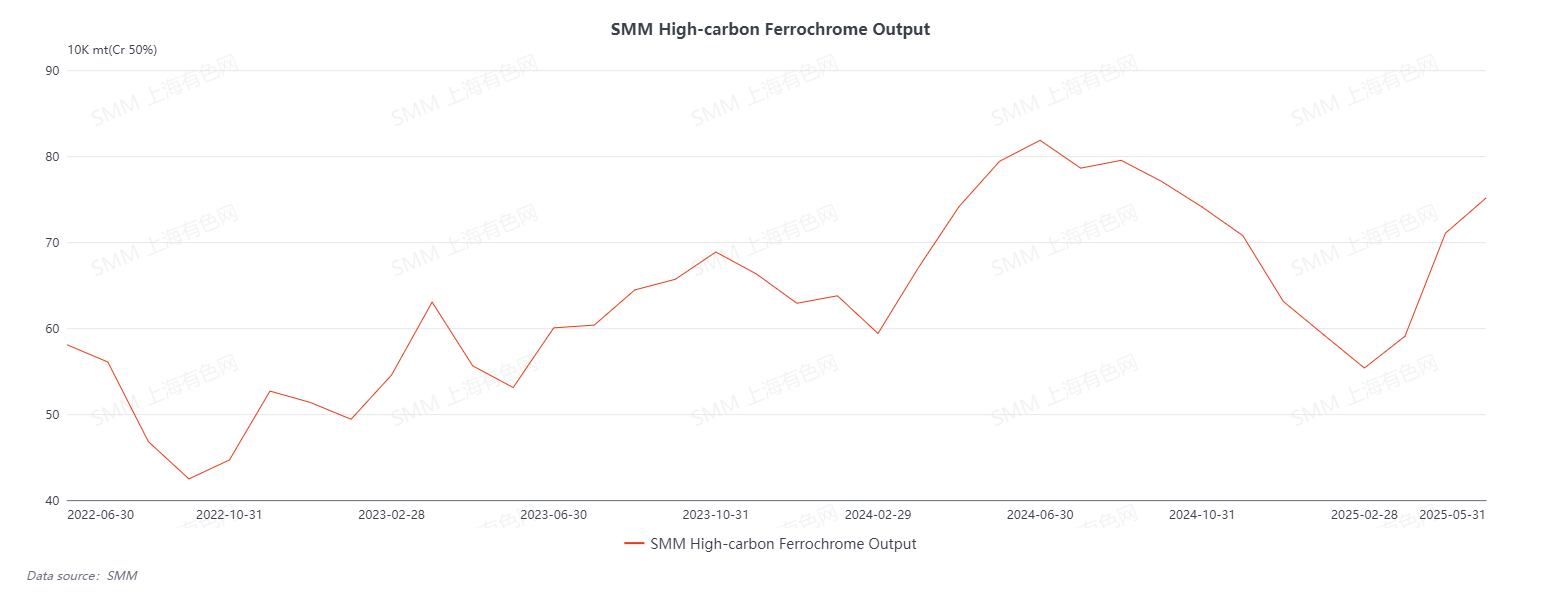

According to SMM data, high-carbon ferrochrome production in May 2025 increased further, rising 5.76% MoM but falling 5.38% YoY. Among them, Inner Mongolia accounted for 78.26% of the production, with a 1.27% MoM increase; the southern region, including Sichuan, Guizhou, and Guangxi, accounted for 17.14%, with a 24.69% MoM increase. In May, the tender prices for high-carbon ferrochrome purchases by mainstream stainless steel mills rose further by 500 yuan/mt (50% metal content), with Tsingshan Group's tender price reaching 8,095 yuan/mt (50% metal content). Influenced by this, the losses of ferrochrome producers eased somewhat, and production enthusiasm increased. Additionally, in April, the retail prices of ferrochrome fluctuated at highs, and the profits of ferrochrome producers were repaired to a certain extent, boosting market confidence and leading to more production resumptions. From the perspective of supply and demand, although downstream stainless steel production in May decreased slightly, it remained at a relatively high level overall. Coupled with significant destocking of ferrochrome, a raw material for steel mills, the demand for ferrochrome drove producers to resume and increase production. From the cost side, spot prices of chrome ore gradually declined during the month, and with two rounds of coke price reductions, the smelting cost of ferrochrome gradually decreased. Meanwhile, under the production resumption plan, the low-priced chrome ore futures purchased earlier in the year arrived at ports successively, and producers mostly completed raw material stocking to control production costs.

Looking ahead to June 2025, high-carbon ferrochrome production is expected to continue to rise slightly. Affected by power restrictions, some ferrochrome producers in northern Inner Mongolia halted production for maintenance in May, leading to abnormal production of ferrochrome. Production is expected to return to normal in June, resulting in a certain increase in ferrochrome output. Additionally, regions such as Sichuan and Chongqing officially entered the rainy season, and some ferrochrome producers have production resumption plans due to electricity price advantages, with operating rates expected to reach a relatively high level. Meanwhile, the decision by South African chrome companies to suspend ferrochrome smelting will significantly impact China's ferrochrome imports, and the reduced volume of imported ferrochrome will have a certain suppressive effect on the ferrochrome supply surplus. However, the June tender prices for high-carbon ferrochrome by mainstream stainless steel mills remained flat, coupled with the impact of downstream stainless steel production cut plans, the retail prices of ferrochrome continued to decline. The supply-demand imbalance in the downstream stainless steel market is evident, leading to cautious procurement of ferrochrome. Transactions in the chrome market have been sluggish recently, with producers mostly bearish on the market outlook and lacking enthusiasm, limiting the increase in ferrochrome output.

![[SMM Iron & Steel] Raipur Billet Prices Edge Higher](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)

![In the short term, ferrous metals will remain under pressure [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/YxksS20251217171748.jpg)

![Silicon Metal Futures Fluctuate within a Narrow Range, Spot Market Largely Stable [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/bkAyC20251217171720.jpg)